You might also like

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Luzon Dev Bank V KrishnaDocument3 pagesLuzon Dev Bank V KrishnaDino Bernard LapitanNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Zacarias Vs Heirs of Revilla G.R. 190901Document10 pagesZacarias Vs Heirs of Revilla G.R. 190901Dino Bernard LapitanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Philippine National Construction Corporation V Pabion 320 Scra 188Document1 pagePhilippine National Construction Corporation V Pabion 320 Scra 188Dino Bernard Lapitan100% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Pacific Consultants V Schonfeld GR 166920Document14 pagesPacific Consultants V Schonfeld GR 166920Dino Bernard LapitanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Gamboa V Teves G.R. 176579Document2 pagesGamboa V Teves G.R. 176579Dino Bernard LapitanNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- People of The Philippins Vs Hernandez G.R. 141221Document33 pagesPeople of The Philippins Vs Hernandez G.R. 141221Dino Bernard LapitanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Bangis V Adolfo G.R. 190875Document8 pagesBangis V Adolfo G.R. 190875Dino Bernard LapitanNo ratings yet

- Consuelo Metal Corp Vs PLanters Development Bank G.R. 152580Document5 pagesConsuelo Metal Corp Vs PLanters Development Bank G.R. 152580Dino Bernard LapitanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Atlantic Erectors V Herbal Cove G.R. 149568Document7 pagesAtlantic Erectors V Herbal Cove G.R. 149568Dino Bernard LapitanNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Seri V Orlane S.A. G.R. 188996Document10 pagesSeri V Orlane S.A. G.R. 188996Dino Bernard LapitanNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Simny Guy V Gilbert Guy G.R. 189486Document9 pagesSimny Guy V Gilbert Guy G.R. 189486Dino Bernard LapitanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Philippine Long Distance Telephone Co V Pingol G.R. 182622Document4 pagesPhilippine Long Distance Telephone Co V Pingol G.R. 182622Dino Bernard LapitanNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- G.R. 173297 Stronghold Insurance V CuencaDocument2 pagesG.R. 173297 Stronghold Insurance V CuencaDino Bernard LapitanNo ratings yet

- Tuna Processing V Philippine Kingford Inc G.R. 185582Document8 pagesTuna Processing V Philippine Kingford Inc G.R. 185582Dino Bernard LapitanNo ratings yet

- Nestor Ching V Subic Bay Golf and Country Club G.R. 174353Document8 pagesNestor Ching V Subic Bay Golf and Country Club G.R. 174353Dino Bernard LapitanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Violeta Tutud BAnate V Philippine Countryside Rural BankDocument7 pagesVioleta Tutud BAnate V Philippine Countryside Rural BankDino Bernard LapitanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- RN Symaco Trading Corporation V Luisito Santos G.R. 142474Document8 pagesRN Symaco Trading Corporation V Luisito Santos G.R. 142474Dino Bernard LapitanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Nemesio Garcia Vs Nicolas Jomouad G.R. 133969Document2 pagesNemesio Garcia Vs Nicolas Jomouad G.R. 133969Dino Bernard LapitanNo ratings yet

- Sunset View Condominium Corporation Petitioner vs. The Hon. Jose C. Campos, Jr. of The Court of First Instance L-52361Document2 pagesSunset View Condominium Corporation Petitioner vs. The Hon. Jose C. Campos, Jr. of The Court of First Instance L-52361Dino Bernard LapitanNo ratings yet

- Lim Tay vs. Court of Appeals G.R. 126891Document2 pagesLim Tay vs. Court of Appeals G.R. 126891Dino Bernard LapitanNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Sps Ajero Vs Court of Appeals G.R. 106720Document4 pagesSps Ajero Vs Court of Appeals G.R. 106720Dino Bernard LapitanNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- A.2.5. Letter of Confirmation of The EngagementDocument3 pagesA.2.5. Letter of Confirmation of The EngagementRodeth CeaNo ratings yet

- General Equilibrium Modelling The State of The ArtDocument7 pagesGeneral Equilibrium Modelling The State of The ArtGodwinUddinNo ratings yet

- Objective of EPSDocument9 pagesObjective of EPSSuryansh GuptaNo ratings yet

- RFQ - M40 Milton Tactical Boots PDFDocument19 pagesRFQ - M40 Milton Tactical Boots PDFSkhumbuzo Macinga0% (1)

- Quit Your JobDocument30 pagesQuit Your JobNoah Navarro100% (2)

- Wellspring Capital LawsuitDocument32 pagesWellspring Capital LawsuitWIS Digital News StaffNo ratings yet

- Audit IndipendenceDocument45 pagesAudit IndipendencegeopourNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Pristine Financial Modeling BrochureDocument4 pagesPristine Financial Modeling BrochureSamarth MarwahaNo ratings yet

- Manchester United PLC 20f 20141027Document706 pagesManchester United PLC 20f 20141027Hassan ShahidNo ratings yet

- Internship Report-FinalDocument48 pagesInternship Report-FinalShamim BaadshahNo ratings yet

- The WatchdogDocument3 pagesThe WatchdogNikunjGuptaNo ratings yet

- Apuntes ContabilidadDocument206 pagesApuntes ContabilidadclaudiazdeandresNo ratings yet

- 56 - 2001 WinterDocument61 pages56 - 2001 Winterc_mc2100% (1)

- Company Law-2 Project Topics, 2019Document8 pagesCompany Law-2 Project Topics, 2019Amitesh TejaswiNo ratings yet

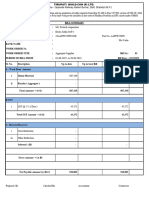

- InvoiceDocument1 pageInvoiceRPGERNo ratings yet

- Bunker HedgingDocument30 pagesBunker Hedgingukhalanthar100% (6)

- Cryptocurrency and Its Impact On Indian EconomyDocument6 pagesCryptocurrency and Its Impact On Indian EconomyShriya VaidyaNo ratings yet

- Marketing Plan WIDocument33 pagesMarketing Plan WIAlliah Mari Pelitro BairaNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- SBR NoteDocument27 pagesSBR Notejeewen thienNo ratings yet

- A Study On The Financial Awareness Among Women Entrepreneurs in Kottayam DistrictDocument6 pagesA Study On The Financial Awareness Among Women Entrepreneurs in Kottayam Districtprashanthi ENo ratings yet

- CORPORATE GOVERNANCE AND ENRON CASE FinalDocument14 pagesCORPORATE GOVERNANCE AND ENRON CASE FinalAllyah Paula PostorNo ratings yet

- ProjectDocument24 pagesProjectYemesirach MengistuNo ratings yet

- ADB Private Sector Financing For RMIT InternationalDocument17 pagesADB Private Sector Financing For RMIT Internationalapi-26045136No ratings yet

- Pakistan Strategy 2022Document148 pagesPakistan Strategy 2022Sulman Bin KhurshidNo ratings yet

- Trutech Stone Crusher KubariDocument7 pagesTrutech Stone Crusher Kubarigolu23_1988No ratings yet

- 3.5 Decision Making To Improve Financial PerformanceDocument2 pages3.5 Decision Making To Improve Financial Performancex SwxyxM xNo ratings yet

- Rules of Debit & CreditDocument16 pagesRules of Debit & CreditVidhya UnniNo ratings yet

- Your Work Your Life - Free Yourself FirstDocument262 pagesYour Work Your Life - Free Yourself FirstRicardo Zimmermann100% (1)

- 2nd Addison v. Felix Chang v. GenatoDocument54 pages2nd Addison v. Felix Chang v. GenatoCzara DyNo ratings yet

- Accenture Basel III HandbookDocument64 pagesAccenture Basel III HandbookSara Humayun100% (2)

- The Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyFrom EverandThe Panama Papers: Breaking the Story of How the Rich and Powerful Hide Their MoneyRating: 4 out of 5 stars4/5 (52)

- Taxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingFrom EverandTaxes for Small Businesses 2023: Beginners Guide to Understanding LLC, Sole Proprietorship and Startup Taxes. Cutting Edge Strategies Explained to Lower Your Taxes Legally for Business, InvestingRating: 5 out of 5 stars5/5 (3)

- Tax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProFrom EverandTax Strategies: The Essential Guide to All Things Taxes, Learn the Secrets and Expert Tips to Understanding and Filing Your Taxes Like a ProRating: 4.5 out of 5 stars4.5/5 (43)