You might also like

- Eturns: After Studying This Chapter, You Will Be Able ToDocument70 pagesEturns: After Studying This Chapter, You Will Be Able ToChandan ganapathi HcNo ratings yet

- ELP Indirect Tax Newsletter November 2022Document6 pagesELP Indirect Tax Newsletter November 2022ELP LawNo ratings yet

- Document 1Document2 pagesDocument 1gstceraslmNo ratings yet

- Refunds: After Studying This Chapter, You Will Be Able ToDocument41 pagesRefunds: After Studying This Chapter, You Will Be Able ToSONICK THUKKANI100% (1)

- Faqs Track Refund Status Tracking Refund StatusDocument7 pagesFaqs Track Refund Status Tracking Refund StatussitNo ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- Assessment and Audit Under GST-DGTPS-New Delhi-19!12!2023-FinalDocument118 pagesAssessment and Audit Under GST-DGTPS-New Delhi-19!12!2023-Finalsanjaypunjabi78No ratings yet

- GST LatestAmendments Issues 01072023Document85 pagesGST LatestAmendments Issues 01072023Selvakumar MuthurajNo ratings yet

- RefundsDocument8 pagesRefundsswati dubeyNo ratings yet

- GST Notices and CompliancesDocument7 pagesGST Notices and CompliancesSubhash VishwakarmaNo ratings yet

- GST Refund changesDocument2 pagesGST Refund changesRicha SachdevaNo ratings yet

- Highlights - 49th GST Council Meeting PDFDocument3 pagesHighlights - 49th GST Council Meeting PDFcarupesh16No ratings yet

- Refund in GSTDocument6 pagesRefund in GSTNilesh SoniNo ratings yet

- Instructions For Form 1120-REIT: U.S. Income Tax Return For Real Estate Investment TrustsDocument12 pagesInstructions For Form 1120-REIT: U.S. Income Tax Return For Real Estate Investment TrustsIRSNo ratings yet

- Do You Know GST - July 2022Document17 pagesDo You Know GST - July 2022CA Ranjan MehtaNo ratings yet

- 'RFD 06Document3 pages'RFD 06ahmgstserviceNo ratings yet

- Presentation Union Budget 2022Document227 pagesPresentation Union Budget 2022nilanjan_kar_2No ratings yet

- Cajournal March2023 15Document9 pagesCajournal March2023 15S M SHEKARNo ratings yet

- GST Registration PPT Ver6 28042017Document46 pagesGST Registration PPT Ver6 28042017Sonal AggarwalNo ratings yet

- Hindustan Unilever GST ReturnsDocument136 pagesHindustan Unilever GST Returnsyoyorikee0% (1)

- Refunds: After Studying This Chapter, You Will Be Able ToDocument59 pagesRefunds: After Studying This Chapter, You Will Be Able Toarohi guptaNo ratings yet

- Refunds: After Studying This Chapter, You Will Be Able ToDocument62 pagesRefunds: After Studying This Chapter, You Will Be Able ToAdventure TimeNo ratings yet

- DCapsule 46 - 27 July 2023Document20 pagesDCapsule 46 - 27 July 2023naveen.mNo ratings yet

- Notice - 18 JanDocument24 pagesNotice - 18 JancgstportalNo ratings yet

- 74824bos60500 cp15Document90 pages74824bos60500 cp15soni12c2004No ratings yet

- Notice 18 JanDocument24 pagesNotice 18 JancgstportalNo ratings yet

- GST Circulars Issued On 6th July - A SummaryDocument8 pagesGST Circulars Issued On 6th July - A SummaryVijaya ChandNo ratings yet

- 6.2 RefundDocument35 pages6.2 Refundvenkatesh grietNo ratings yet

- Refund FaqDocument3 pagesRefund FaqMy GST RefundNo ratings yet

- Ack FGVPK3894L 2022-23 255674620290722Document1 pageAck FGVPK3894L 2022-23 255674620290722dharmesh1986No ratings yet

- Class PaperDocument1 pageClass PaperPrashant GargNo ratings yet

- PDF 979942370250722Document1 pagePDF 979942370250722MANNA PERSONNELNo ratings yet

- ITR Filing Acknowledgement for AY 2022-23Document1 pageITR Filing Acknowledgement for AY 2022-23Prashant GargNo ratings yet

- Capital Reduction Losses Allowed or DisallowedDocument5 pagesCapital Reduction Losses Allowed or DisallowedJUNA SURESHNo ratings yet

- RR No. 12-13Document2 pagesRR No. 12-13shlm bNo ratings yet

- Atul Saini 22Document1 pageAtul Saini 22Fascino WhiteNo ratings yet

- Ramanjeet Itr 22-23Document1 pageRamanjeet Itr 22-23MK ASSOCIATESNo ratings yet

- RSM India Union Budget 2021 HighlightsDocument132 pagesRSM India Union Budget 2021 HighlightsSunil KumarNo ratings yet

- EY Changes To Indonesian Rules DGT Regulation No 25 PJ 2018 PDFDocument6 pagesEY Changes To Indonesian Rules DGT Regulation No 25 PJ 2018 PDFSyahrul IchwanNo ratings yet

- Parachutepayments ExamplesDocument8 pagesParachutepayments ExamplesaxispointdbNo ratings yet

- A Brief Introduction To CGST, Sgst/Utgst, Igst & Compensation Cess Act (S)Document38 pagesA Brief Introduction To CGST, Sgst/Utgst, Igst & Compensation Cess Act (S)JkNo ratings yet

- TDS Rates 2021 - 22Document7 pagesTDS Rates 2021 - 22Shantanu BhadkamkarNo ratings yet

- Net Business IncomeDocument21 pagesNet Business IncomedonawajNo ratings yet

- ITR Acknowledgement for AY 2022-23Document1 pageITR Acknowledgement for AY 2022-23QunalNo ratings yet

- RefundDocument6 pagesRefundManish K JadhavNo ratings yet

- Audit Offence Penalty-ApurvaDocument35 pagesAudit Offence Penalty-ApurvaApurva DharNo ratings yet

- ITRVDocument1 pageITRVPeppyPlants plantsNo ratings yet

- Ack Bqgpa0377p 2022-23 794790900120722Document1 pageAck Bqgpa0377p 2022-23 794790900120722inspiremetonewworldNo ratings yet

- GSTV70P4 November 27 December 3 (PG 144) SamplechapterDocument2 pagesGSTV70P4 November 27 December 3 (PG 144) SamplechapterSatyakanth SunkaraNo ratings yet

- PDF 235571600140623Document1 pagePDF 235571600140623Hema TNo ratings yet

- Ack Aadhn6348f 2022-23 220799250290722Document1 pageAck Aadhn6348f 2022-23 220799250290722Akansha JainNo ratings yet

- GST Annual Return and AuditDocument10 pagesGST Annual Return and AuditRachit ChhedaNo ratings yet

- ITR Acknowledgement for AY 2022-23Document1 pageITR Acknowledgement for AY 2022-23Sam SargeNo ratings yet

- Instructions For Form 990-C: Internal Revenue ServiceDocument12 pagesInstructions For Form 990-C: Internal Revenue ServiceIRSNo ratings yet

- PDF 176612130280722Document1 pagePDF 176612130280722Sudhangshu SarkarNo ratings yet

- Indian Income Tax Return Acknowledgement 2022-23: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2022-23: Assessment YearYash ChauhanNo ratings yet

- Minimum Alternate Tax: Prepared by - Dhaval Girishkumar TrivediDocument21 pagesMinimum Alternate Tax: Prepared by - Dhaval Girishkumar TrivediSmit NareshNo ratings yet

- Ack Cdhpa3843f 2022-23 220950670290722Document1 pageAck Cdhpa3843f 2022-23 220950670290722rtaxhelp helpNo ratings yet

- TDS 21-22Document25 pagesTDS 21-22dinesh kasnNo ratings yet

- Credit Annual STMTDocument9 pagesCredit Annual STMTKunalKumarNo ratings yet

- Tattvam Advisors GSTR 9 and 9CDocument63 pagesTattvam Advisors GSTR 9 and 9CKunalKumarNo ratings yet

- Bachelor in Retail Management (BRM)Document1 pageBachelor in Retail Management (BRM)KunalKumarNo ratings yet

- NEW-AGE LAMINATES FROM GREENLAMDocument64 pagesNEW-AGE LAMINATES FROM GREENLAMKunalKumarNo ratings yet

- Applicability of ESIC On CompaniesDocument5 pagesApplicability of ESIC On CompaniesKunalKumarNo ratings yet

- Joint Development Agreements GST Implications: CA Ashish KR Bansal M:9336100380 Ashishbansal@gcac - inDocument21 pagesJoint Development Agreements GST Implications: CA Ashish KR Bansal M:9336100380 Ashishbansal@gcac - inKunalKumarNo ratings yet

- Jharkhandselfsupportingco Operativesocietiesact 1996Document42 pagesJharkhandselfsupportingco Operativesocietiesact 1996KunalKumarNo ratings yet

- Circular 1 2023Document1 pageCircular 1 2023KunalKumarNo ratings yet

- Liability of JDA entered prior to GST when SA is entered post GSTDocument3 pagesLiability of JDA entered prior to GST when SA is entered post GSTKunalKumarNo ratings yet

- Fair Usage PolicyDocument1 pageFair Usage Policykodi.sudarNo ratings yet

- GST JugDocument14 pagesGST JugKunalKumarNo ratings yet

- E Flier Credit Notes in GSTDocument2 pagesE Flier Credit Notes in GSTSneha AgarwalNo ratings yet

- GSTR Form Sub Column Form GSTR 1: 7 B2C (Interstate, Invoice Upto 2.5 Lakh & Intrastate (All) ) A Intrastate AllDocument8 pagesGSTR Form Sub Column Form GSTR 1: 7 B2C (Interstate, Invoice Upto 2.5 Lakh & Intrastate (All) ) A Intrastate AllKunalKumarNo ratings yet

- 2f86d64GST Issues in Place of Supply and IGST 050818Document57 pages2f86d64GST Issues in Place of Supply and IGST 050818KunalKumarNo ratings yet

- SavingAccountCharges PDFDocument1 pageSavingAccountCharges PDFKunalKumarNo ratings yet

- GST Imp DefinitionsDocument14 pagesGST Imp DefinitionsKunalKumarNo ratings yet

- Akers Study GuideDocument44 pagesAkers Study GuideAravind SastryNo ratings yet

- Collated Suggestions Submitted On Draft RulesDocument26 pagesCollated Suggestions Submitted On Draft RulesKunalKumarNo ratings yet

- Final Collated Suggestions For Printing - WatermarkDocument85 pagesFinal Collated Suggestions For Printing - WatermarkKunalKumarNo ratings yet

- Analysis Definitions CGSTSGSTDocument20 pagesAnalysis Definitions CGSTSGSTKunalKumarNo ratings yet

- Report On GST RegistrationDocument52 pagesReport On GST RegistrationLillyLalithaNo ratings yet

- Sector GSTDocument105 pagesSector GSTKunalKumarNo ratings yet

- Services Booklet 03july2017Document30 pagesServices Booklet 03july2017Vaishnavi JayakumarNo ratings yet

- Lifting of Corporate Veil - Indian ScenarioDocument10 pagesLifting of Corporate Veil - Indian ScenarioKunalKumarNo ratings yet

- Transitional Provision Act Rules LM 17052017Document30 pagesTransitional Provision Act Rules LM 17052017KunalKumarNo ratings yet

- Interpretation of StatutesDocument1 pageInterpretation of StatutesKunalKumarNo ratings yet

- GST Ebook sk-1Document89 pagesGST Ebook sk-1KunalKumarNo ratings yet

- Limitation Act 2963 36 of 1963 With Exhaustive CDocument2 pagesLimitation Act 2963 36 of 1963 With Exhaustive CKunalKumarNo ratings yet

- Director Report PVT LTD FinalDocument22 pagesDirector Report PVT LTD FinalKunalKumarNo ratings yet

- InvoiceDocument1 pageInvoicemrrohitmehta8No ratings yet

- Patrakar SadanDocument4 pagesPatrakar SadanRKM RKMNo ratings yet

- Invoice - HitDocument1 pageInvoice - HitAnkit MaheshwariNo ratings yet

- Self Test 4. Financial Planning Time: 1 Hour) (Marks: 20 Q. 1. (A) Choose The Correct Alternative From Those Given Below Each Question: 4Document3 pagesSelf Test 4. Financial Planning Time: 1 Hour) (Marks: 20 Q. 1. (A) Choose The Correct Alternative From Those Given Below Each Question: 4UmarNo ratings yet

- Kadakia PlasticsDocument1 pageKadakia PlasticsRajiv DubeyNo ratings yet

- TAX INVOICE FOR DALMIA CEMENTDocument2 pagesTAX INVOICE FOR DALMIA CEMENTRaja HussainNo ratings yet

- Honours SyllabusDocument48 pagesHonours Syllabusleo aminNo ratings yet

- Print - MALDA TOWN (MLDT) - RAIPUR JN (R) - 6224111704Document1 pagePrint - MALDA TOWN (MLDT) - RAIPUR JN (R) - 6224111704sourajya BanikNo ratings yet

- Consolidated InvoiceDocument4 pagesConsolidated InvoiceNarendra NarshimamoorthyNo ratings yet

- UntitledDocument11 pagesUntitleddeepika devsaniNo ratings yet

- Manual - PPT On EInvoice SystemDocument52 pagesManual - PPT On EInvoice SystemDadang Tirtha100% (1)

- 9517309706Document2 pages9517309706Doita Dutta ChoudhuryNo ratings yet

- Goods and Service Tax Act, 2017Document4 pagesGoods and Service Tax Act, 2017shivani yadavNo ratings yet

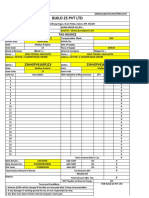

- Build 25 PVT LTD: Tax InvoiceDocument2 pagesBuild 25 PVT LTD: Tax InvoiceM O7No ratings yet

- TNPSC SURESH IAS ACADEMY July Current Affairs (E)Document60 pagesTNPSC SURESH IAS ACADEMY July Current Affairs (E)Siva Raman KNo ratings yet

- HON - Price Reckoner-May - 2023Document108 pagesHON - Price Reckoner-May - 2023Er Sundeep RachakondaNo ratings yet

- LIC policy renewal receiptDocument1 pageLIC policy renewal receiptCHAKRADHAR REDDYNo ratings yet

- Expense Reimbursement FormDocument3 pagesExpense Reimbursement Formг๏ђเt кย๓คг ๒คﻮђєlNo ratings yet

- CA Rajat Jain: Career ObjectiveDocument3 pagesCA Rajat Jain: Career ObjectiveThe Cultural CommitteeNo ratings yet

- Accura Diagnostics AMC Proposal All DocumentDocument6 pagesAccura Diagnostics AMC Proposal All DocumentMahadeva SwamyNo ratings yet

- GSTR1 Excel Workbook Template V1.5Document65 pagesGSTR1 Excel Workbook Template V1.5OM PRAKASH ROYNo ratings yet

- Acronyms Important Abbreviations in Banking: AffairsDocument10 pagesAcronyms Important Abbreviations in Banking: AffairsAbhijeet PatilNo ratings yet

- Sri Sai Food CourtDocument1 pageSri Sai Food CourtpvrdeveltestNo ratings yet

- Verma EnterprisesDocument2 pagesVerma EnterpriseskapilazarchitectsNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)RMNo ratings yet

- Law of TaxationDocument13 pagesLaw of TaxationAar ManojNo ratings yet

- Fiber Monthly Statement: This Month's SummaryDocument4 pagesFiber Monthly Statement: This Month's Summaryspartan sportNo ratings yet

- Toaz - Info Invoice Amazonpdf PRDocument1 pageToaz - Info Invoice Amazonpdf PRwakaNo ratings yet

- Budget SpeechDocument28 pagesBudget SpeechExpress Web0% (1)

- Invoice 20022024142838Document2 pagesInvoice 20022024142838s.madhuniNo ratings yet