You might also like

- CFP Investment Planning Study Notes SampleDocument28 pagesCFP Investment Planning Study Notes SampleMeenakshi67% (3)

- UniglobeDocument2 pagesUniglobeGurdev SinghNo ratings yet

- Lic Receipt PDFDocument1 pageLic Receipt PDFrohitjain444No ratings yet

- Case Study For CFPDocument1 pageCase Study For CFPsinghanshu21100% (2)

- CasesDocument43 pagesCasesapi-3814557No ratings yet

- Sample Paper for Exam 4: Tax Planning & Estate Planning (AY2015-16Document9 pagesSample Paper for Exam 4: Tax Planning & Estate Planning (AY2015-16SODDEYNo ratings yet

- CFP Introduction To Financial Planning Study Notes SampleDocument42 pagesCFP Introduction To Financial Planning Study Notes SampleMeenakshi67% (3)

- CFP Retirement Planning Study Notes SampleDocument35 pagesCFP Retirement Planning Study Notes SampleMeenakshi100% (1)

- Investment Analysis and Portfolio Management Practice Book SampleDocument21 pagesInvestment Analysis and Portfolio Management Practice Book SampleMeenakshi86% (7)

- CFP Introduction To Financial Planning Study Notes SampleDocument42 pagesCFP Introduction To Financial Planning Study Notes SampleMeenakshi67% (3)

- Key Principle and Characteristics of Micro FinanceDocument18 pagesKey Principle and Characteristics of Micro Financedeepakbrt85% (40)

- Intro Practice Book Sample FPDocument35 pagesIntro Practice Book Sample FPnaresh2011No ratings yet

- Advance Financial Planning Study Notes Part 1Document63 pagesAdvance Financial Planning Study Notes Part 1MeenakshiNo ratings yet

- Advance Financial Planning Practice Book Part 2 Case Studies 2Document27 pagesAdvance Financial Planning Practice Book Part 2 Case Studies 2Meenakshi77% (13)

- CFP Tax Stduy Note SampleDocument51 pagesCFP Tax Stduy Note SampleMeenakshiNo ratings yet

- Advance Financial Planning Study Notes Part 2Document63 pagesAdvance Financial Planning Study Notes Part 2Meenakshi0% (1)

- CFP Investment Planning Practice Book SampleDocument51 pagesCFP Investment Planning Practice Book SampleMeenakshi100% (1)

- NCFMNISM Online Question Bank AvailableDocument2 pagesNCFMNISM Online Question Bank AvailableMeenakshi100% (2)

- Money & MoreDocument31 pagesMoney & MoreMaulik ShahNo ratings yet

- Limited Preview of CFP Study Material of IMS ProschoolDocument96 pagesLimited Preview of CFP Study Material of IMS ProschoolSai Krishna DhulipallaNo ratings yet

- Gurpreet Case Study - Only AnswersDocument12 pagesGurpreet Case Study - Only Answerspooja katariya0% (1)

- Exam4 PastCaseStudy 2010Document46 pagesExam4 PastCaseStudy 2010Namrata PrajapatiNo ratings yet

- Sahanubhuti Case Study 2017 Que & SolDocument13 pagesSahanubhuti Case Study 2017 Que & SolIBBF FitnessNo ratings yet

- Risk Analysis & Insurance Planning (RAIP)Document19 pagesRisk Analysis & Insurance Planning (RAIP)Harichandra PatilNo ratings yet

- WN - 2Document6 pagesWN - 2bhaw_shNo ratings yet

- Ashwini Agarwal Age34 - Case - A - MasterDocument61 pagesAshwini Agarwal Age34 - Case - A - MasterAmit GuptaNo ratings yet

- Maricris G. Alagar BA-101 Finance IIDocument5 pagesMaricris G. Alagar BA-101 Finance IIMharykhriz AlagarNo ratings yet

- Ref Date 1/4/17 Sahanubhuti SP-2 Pattern Question Bank (15 Questions: 2 HRS)Document4 pagesRef Date 1/4/17 Sahanubhuti SP-2 Pattern Question Bank (15 Questions: 2 HRS)preeti chhatwalNo ratings yet

- Capital Market Dealer Module Practice Book SampleDocument36 pagesCapital Market Dealer Module Practice Book SampleMeenakshi86% (7)

- CFP RaipDocument3 pagesCFP RaipsinhapushpanjaliNo ratings yet

- NISM CPFA Mock Test at WWW - MODELEXAM.INDocument2 pagesNISM CPFA Mock Test at WWW - MODELEXAM.INSRINIVASANNo ratings yet

- Sanjay Case Study 2017 QsDocument3 pagesSanjay Case Study 2017 QsIBBF FitnessNo ratings yet

- Sample Papre For Investment PlanningDocument5 pagesSample Papre For Investment Planningapi-3706352No ratings yet

- IMS Proschool CFA EbookDocument356 pagesIMS Proschool CFA EbookAjay Yadav0% (1)

- 2020 CFP Exam Candidate Prep Toolkit Nov 2020Document28 pages2020 CFP Exam Candidate Prep Toolkit Nov 2020Calvin YeohNo ratings yet

- Nism Series X A Investment Adviser Level 1 Exam WorkbookDocument12 pagesNism Series X A Investment Adviser Level 1 Exam WorkbookGautam KhannaNo ratings yet

- Manual Financial Calculator FC-200V - 100V - EngDocument149 pagesManual Financial Calculator FC-200V - 100V - Engm2biz05No ratings yet

- Welcome to Pass4Sure Mock TestDocument28 pagesWelcome to Pass4Sure Mock TestManan SharmaNo ratings yet

- Review Extra CreditDocument8 pagesReview Extra CreditMichelle de GuzmanNo ratings yet

- Prashant FinalReportDocument29 pagesPrashant FinalReportadhia_saurabh100% (1)

- Portfolio Management Extra Practice QuestionsDocument17 pagesPortfolio Management Extra Practice QuestionsVANDANA GOYALNo ratings yet

- Exam5 CaseStudy 2009Document248 pagesExam5 CaseStudy 2009Swetal ParmarNo ratings yet

- Section 80 Deduction Table and Limits for FY 2018-19Document45 pagesSection 80 Deduction Table and Limits for FY 2018-19Shobhit KumarNo ratings yet

- Tax Estate CFP Mock TestDocument22 pagesTax Estate CFP Mock Testbitterhoney4871100% (1)

- Nism X B Caselet 7Document8 pagesNism X B Caselet 7Finware 1No ratings yet

- Spiral 2 - FPSB CasesDocument66 pagesSpiral 2 - FPSB CasesAditya LohiaNo ratings yet

- Personal Wealth Management Plan for Ms. Sahanubhuti VanaspatiDocument9 pagesPersonal Wealth Management Plan for Ms. Sahanubhuti VanaspatiAditya GulatiNo ratings yet

- CFP Sample Paper Tax PlanningDocument4 pagesCFP Sample Paper Tax PlanningamishasoniNo ratings yet

- Ashwin Case Study 2017 Que & SolDocument14 pagesAshwin Case Study 2017 Que & SolIBBF FitnessNo ratings yet

- CFP - Module 1 - IIFP - StudentsDocument269 pagesCFP - Module 1 - IIFP - StudentsmodisahebNo ratings yet

- Derivative Market Dealer Module Practice Book SampleDocument35 pagesDerivative Market Dealer Module Practice Book SampleMeenakshi0% (1)

- Fast Track CFP Exam 5 (Final Exam) Preparation Training Workshop1Document2 pagesFast Track CFP Exam 5 (Final Exam) Preparation Training Workshop1keyur1975No ratings yet

- Course Outline Advanced Corporate Finance 2019Document8 pagesCourse Outline Advanced Corporate Finance 2019Ali Shaharyar ShigriNo ratings yet

- Compound Interest Explained: Calculating Future and Present Value of AnnuitiesDocument30 pagesCompound Interest Explained: Calculating Future and Present Value of AnnuitiesAshia12No ratings yet

- 9 CFP Exam5-Afp-2008 Case Studies PDFDocument130 pages9 CFP Exam5-Afp-2008 Case Studies PDFankur892No ratings yet

- Chapter Five Investment PolicyDocument14 pagesChapter Five Investment PolicyfergiemcNo ratings yet

- Retirement Workbook 3.2Document31 pagesRetirement Workbook 3.2Tejas Shah83% (6)

- CFA - Alternative Investment Question Book NoteDocument12 pagesCFA - Alternative Investment Question Book NoteJingdan ZhangNo ratings yet

- Demo - Nism 5 A - Mutual Fund ModuleDocument7 pagesDemo - Nism 5 A - Mutual Fund ModuleDiwakarNo ratings yet

- Advanced Financial Planning Case Studies ForDocument19 pagesAdvanced Financial Planning Case Studies ForPrashant UjjawalNo ratings yet

- Investment Planning (Finally Done)Document146 pagesInvestment Planning (Finally Done)api-3814557100% (2)

- FPSBI/M-VI/01-01/10/SP-21: 1 FPSB India / PublicDocument11 pagesFPSBI/M-VI/01-01/10/SP-21: 1 FPSB India / Publicbhaw_shNo ratings yet

- CFP Introduction To Financial Planning Practice Book SampleDocument35 pagesCFP Introduction To Financial Planning Practice Book SampleMeenakshi100% (1)

- CFP Retirerment Planning Practice Book SampleDocument43 pagesCFP Retirerment Planning Practice Book SampleMeenakshi100% (4)

- 31st - Vi TrimesterDocument38 pages31st - Vi TrimesterPrasanth SurendharNo ratings yet

- CFP Risk Analysis and Insurance Planning Practice Book SampleDocument34 pagesCFP Risk Analysis and Insurance Planning Practice Book SampleMeenakshi100% (7)

- CFP Introduction To Financial Planning Practice Book SampleDocument35 pagesCFP Introduction To Financial Planning Practice Book SampleMeenakshi100% (1)

- Financial Market Beginner Module Practice Book SampleDocument26 pagesFinancial Market Beginner Module Practice Book SampleMeenakshi79% (19)

- Macro Economics XII MCQs/One Mark Questions With AnswersDocument6 pagesMacro Economics XII MCQs/One Mark Questions With AnswersMeenakshiNo ratings yet

- NCFMNISM Online Question Bank AvailableDocument2 pagesNCFMNISM Online Question Bank AvailableMeenakshi100% (2)

- Commodity Practice Book Sample NewDocument26 pagesCommodity Practice Book Sample NewMeenakshiNo ratings yet

- CFP Risk Analysis and Insurance Planning Study Notes SampleDocument33 pagesCFP Risk Analysis and Insurance Planning Study Notes SampleMeenakshiNo ratings yet

- CFP Introduction To Financial Planning Study Notes SampleDocument42 pagesCFP Introduction To Financial Planning Study Notes SampleMeenakshiNo ratings yet

- CFP Investment Planning Practice Book SampleDocument51 pagesCFP Investment Planning Practice Book SampleMeenakshi100% (1)

- CFP Tax Planning & Estate Planning Practice Book SampleDocument35 pagesCFP Tax Planning & Estate Planning Practice Book SampleMeenakshi100% (1)

- Currency Derivavtive Practice Book SampleDocument26 pagesCurrency Derivavtive Practice Book SampleMeenakshi50% (2)

- CFP Retirerment Planning Practice Book SampleDocument43 pagesCFP Retirerment Planning Practice Book SampleMeenakshi100% (4)

- CFP Risk Analysis and Insurance Planning Practice Book SampleDocument34 pagesCFP Risk Analysis and Insurance Planning Practice Book SampleMeenakshi100% (7)

- CFP Tax Stduy Note SampleDocument51 pagesCFP Tax Stduy Note SampleMeenakshiNo ratings yet

- Roots Institute of Financial Markets RifmDocument24 pagesRoots Institute of Financial Markets RifmUtpal LahkarNo ratings yet

- Derivative Market Dealer Module Practice Book SampleDocument35 pagesDerivative Market Dealer Module Practice Book SampleMeenakshi0% (1)

- Securities Market Practice Book SampleDocument24 pagesSecurities Market Practice Book SampleMeenakshiNo ratings yet

- Capital Market Dealer Module Practice Book SampleDocument36 pagesCapital Market Dealer Module Practice Book SampleMeenakshi86% (7)

- Option Trading Strategies SampleDocument27 pagesOption Trading Strategies SampleMeenakshiNo ratings yet

- Advance Financial Planning Practice Book Part 1Document46 pagesAdvance Financial Planning Practice Book Part 1Meenakshi50% (2)

- RIFM BooksDocument1 pageRIFM BooksMeenakshiNo ratings yet

- CFP Intro Practice Book SampleDocument41 pagesCFP Intro Practice Book SampleMeenakshi100% (1)

- City of Houston Bond Issuance, March 8, 2006, Official StatementDocument224 pagesCity of Houston Bond Issuance, March 8, 2006, Official StatementTexas WatchdogNo ratings yet

- 634420393Document3 pages634420393Lucas De Paula CarneiroNo ratings yet

- Orden de Venta - 372 - 20181123 - 123904Document2 pagesOrden de Venta - 372 - 20181123 - 123904l2oNnYNo ratings yet

- Precious Metal AgreementDocument25 pagesPrecious Metal AgreementlboninsouzaNo ratings yet

- Philippine Interpretations Committee Operating ProceduresDocument5 pagesPhilippine Interpretations Committee Operating ProceduresJere Mae Bertuso TaganasNo ratings yet

- Executive Summary My ReportDocument1 pageExecutive Summary My ReportNirob Hasan VoorNo ratings yet

- Sindh ABS 0910Document86 pagesSindh ABS 0910Wajiha SaeedNo ratings yet

- The History of Global Banking - A Broken SystemDocument2 pagesThe History of Global Banking - A Broken SystemMariel ManzurNo ratings yet

- Vidhyaashram First Grade College Corporate Accounting III II AssignmentDocument4 pagesVidhyaashram First Grade College Corporate Accounting III II AssignmentveenaNo ratings yet

- Research MethodologyDocument34 pagesResearch MethodologySangeetaLakhesar80% (5)

- SbiDocument157 pagesSbijai2607No ratings yet

- Accounting Treatment of Goodwill at The Time of AdmissionDocument25 pagesAccounting Treatment of Goodwill at The Time of AdmissionMayurRawool100% (2)

- Transportation Case Digest: Mayer Steel Pipe Corp. V. CA (1997)Document2 pagesTransportation Case Digest: Mayer Steel Pipe Corp. V. CA (1997)jobelle barcellanoNo ratings yet

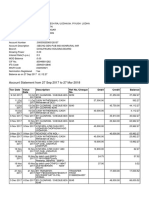

- Account statement details for Mr. Chandresh Raj LodhaDocument3 pagesAccount statement details for Mr. Chandresh Raj LodhaHemlata LodhaNo ratings yet

- Role of Service Marketing in Banking SectorDocument16 pagesRole of Service Marketing in Banking SectorWaseem AshrafNo ratings yet

- Struktur OrganisasiDocument1 pageStruktur OrganisasiRoudaNo ratings yet

- Fmutm Mock 05Document8 pagesFmutm Mock 05api-2686327667% (3)

- List of Kenya Counties and WardsDocument199 pagesList of Kenya Counties and WardsAnonymous E9xmcrKgSkNo ratings yet

- Training Material - Transaction Codes in SAP FICO PDFDocument17 pagesTraining Material - Transaction Codes in SAP FICO PDFSiva KumarNo ratings yet

- CIR Vs Manila Bankers' Life Insurance CorpDocument9 pagesCIR Vs Manila Bankers' Life Insurance CorpAnonymous vAVKlB1No ratings yet

- Estmt - 2023 05 05Document6 pagesEstmt - 2023 05 05manolo IamanditaNo ratings yet

- Banking-Finance Degree at Beirut Arab UniversityDocument5 pagesBanking-Finance Degree at Beirut Arab UniversityAA BB MMNo ratings yet

- Bank of MaharashtraDocument91 pagesBank of MaharashtraArun Savukar67% (3)

- QMS ProposalDocument22 pagesQMS Proposalflawlessy2kNo ratings yet

- The North Face Case Audit MaterialityDocument2 pagesThe North Face Case Audit MaterialityAjeng TriyanaNo ratings yet

- Ansbacher/Cayman ReportDocument506 pagesAnsbacher/Cayman ReportGavin SheridanNo ratings yet

- Top State Bank Customers in DelhiDocument56 pagesTop State Bank Customers in Delhidoon devbhoomi realtorsNo ratings yet