You might also like

- Baleno-Accessories Brochure PDFDocument8 pagesBaleno-Accessories Brochure PDFnapinnvoNo ratings yet

- Aug - 17 Vessels DetailsDocument2 pagesAug - 17 Vessels Detailssuneelmanage09No ratings yet

- ImpactAssessmentReport TISS2015Document117 pagesImpactAssessmentReport TISS2015suneelmanage09No ratings yet

- E´Ekõj·T Kõ+Πø‹Ø£ J·÷»E÷Q´ Dü+Düú: (Atma)Document8 pagesE´Ekõj·T Kõ+Πø‹Ø£ J·÷»E÷Q´ Dü+Düú: (Atma)suneelmanage09No ratings yet

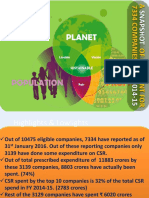

- On CSR Expenditure of 7334 Companies For F.Y 2014 15Document14 pagesOn CSR Expenditure of 7334 Companies For F.Y 2014 15suneelmanage09No ratings yet

- List of FPOs in The State of Andhra PradeshDocument1 pageList of FPOs in The State of Andhra Pradeshsuneelmanage09No ratings yet

- NCML BrochureDocument16 pagesNCML Brochuresuneelmanage09No ratings yet

- Associations Federations Councils Etc ContactsDocument20 pagesAssociations Federations Councils Etc Contactssuneelmanage09No ratings yet

- Import Export Detailed ReportDocument468 pagesImport Export Detailed Reportsharath_medishetty100% (1)

- Website Rating Certificate FileDocument58 pagesWebsite Rating Certificate Filesuneelmanage09No ratings yet

- A Value Chain On Ginger & Ginger ProductsDocument117 pagesA Value Chain On Ginger & Ginger Productssuneelmanage09100% (2)

- Hortstat GlanceDocument463 pagesHortstat GlancebhagatvarunNo ratings yet

- Kenya Leather Industry Diagnosis Strategy and Action PlanDocument126 pagesKenya Leather Industry Diagnosis Strategy and Action Plansuneelmanage09No ratings yet

- Food Supply Chains and Their Influence On Resurgence in Institutions of CommonsDocument18 pagesFood Supply Chains and Their Influence On Resurgence in Institutions of Commonssuneelmanage09No ratings yet

- FAO IGG TEA - Working Group On Organic Tea May 2014Document17 pagesFAO IGG TEA - Working Group On Organic Tea May 2014suneelmanage09No ratings yet

- Palm Jaggery Gur Making UnitDocument2 pagesPalm Jaggery Gur Making Unitsuneelmanage09No ratings yet

- 5.wheat Production 8IWC SS SinghDocument29 pages5.wheat Production 8IWC SS Singhsuneelmanage09No ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Orissa High Court FILING REPORT AS ON:21/10/2019Document44 pagesOrissa High Court FILING REPORT AS ON:21/10/2019sunita beharaNo ratings yet

- Neet Councelling 2021Document218 pagesNeet Councelling 2021pratap singhNo ratings yet

- The Textile MagazineDocument110 pagesThe Textile MagazineKayPeaB100% (1)

- Indo Pak History Past Papers Solved MCQs For CSSDocument68 pagesIndo Pak History Past Papers Solved MCQs For CSSSangeen Ali Pti87% (15)

- Janata PartyDocument10 pagesJanata PartySuresh RVNo ratings yet

- Jipmer Mbbs Result ObcDocument687 pagesJipmer Mbbs Result ObcMota Chashma60% (5)

- ShivajiDocument2 pagesShivajiŚáńtőśh MőkáśhíNo ratings yet

- JEE Previous Year Question Paper.Document5 pagesJEE Previous Year Question Paper.Pushpa palNo ratings yet

- Economy of India PDFDocument48 pagesEconomy of India PDFSugan PragasamNo ratings yet

- High Court For The State of TelanganaDocument4 pagesHigh Court For The State of TelanganaSiya PatilNo ratings yet

- Moot PropositionDocument3 pagesMoot PropositionShashank BajajNo ratings yet

- LovableDocument1 pageLovableKushal Akbari100% (1)

- Abhishek Dabur ReportDocument45 pagesAbhishek Dabur ReportAbhishek SinghNo ratings yet

- Vrat List 2012Document2 pagesVrat List 2012hindu_societyNo ratings yet

- CDS History Qustion BLDocument118 pagesCDS History Qustion BLharshit kuchhalNo ratings yet

- Tobha Tek Singh English TranslationDocument7 pagesTobha Tek Singh English TranslationJasdeep Singh100% (2)

- HiDocument3 pagesHiRaghuNo ratings yet

- Mintwise Regular Commemorative Coins of Republic IndiaDocument3 pagesMintwise Regular Commemorative Coins of Republic Indiashridhar_9788No ratings yet

- Retailing Intro and TheoryDocument135 pagesRetailing Intro and Theorymohitegaurv87No ratings yet

- Mrunal CAPF Answerkey 2015 - History & Culture Questions SolvedDocument9 pagesMrunal CAPF Answerkey 2015 - History & Culture Questions SolvedJambulingam SarangapaniNo ratings yet

- (Toppers Interview) Rohit Shukla (AIR 238 - CSE 2011) Shares Psychology Booklist and His Successful Journey MrunalDocument9 pages(Toppers Interview) Rohit Shukla (AIR 238 - CSE 2011) Shares Psychology Booklist and His Successful Journey MrunalPradeep Dubey100% (1)

- Ancient History of Bengal Lec - 02Document5 pagesAncient History of Bengal Lec - 02abdzawad00007No ratings yet

- Multi Polar IsmDocument18 pagesMulti Polar Ismprofu1969No ratings yet

- Bank of Maharashtra PO Results 2016 Out!Document61 pagesBank of Maharashtra PO Results 2016 Out!nidhi tripathi100% (1)

- 06 - Chapter 1Document10 pages06 - Chapter 1Loke RajpavanNo ratings yet

- Question Paper Pattern For University Examination M.A., Degree Examination Section - A (10 × 1 10)Document56 pagesQuestion Paper Pattern For University Examination M.A., Degree Examination Section - A (10 × 1 10)samarthNo ratings yet

- Ali, Chaudhry - Faridi (2012) - PORTRAYAL OF MUSLIMS, ShehzadAliDocument23 pagesAli, Chaudhry - Faridi (2012) - PORTRAYAL OF MUSLIMS, ShehzadAliShalini DixitNo ratings yet

- 2059 w15 QP 1Document4 pages2059 w15 QP 1Farghab RazaNo ratings yet

- GuidelineDocument490 pagesGuidelineRajesh BanwaniNo ratings yet

- Collector Guideline Shajapur 2020-21Document244 pagesCollector Guideline Shajapur 2020-21Shubham Mourya100% (1)