You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 3 Months Statement. SAUDA 18Document2 pages3 Months Statement. SAUDA 18Fikile Eem100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Just For Feet, Inc.: CASE 1.3Document11 pagesJust For Feet, Inc.: CASE 1.3ffffffff dfdfdfNo ratings yet

- AES Case PresentationDocument13 pagesAES Case PresentationClaire Marie Thomas67% (3)

- Seller'S Full LetterheadDocument4 pagesSeller'S Full LetterheadRailesUsados83% (6)

- Chapter 6 Sample ProblemsDocument3 pagesChapter 6 Sample ProblemsShaiTengcoNo ratings yet

- Aditya Birla Fashion and Retail Limited: Disc - Amt Disc% Item - Name Ean - Code HSN QTY MRP Net - Amt Tax - Rate TaxDocument2 pagesAditya Birla Fashion and Retail Limited: Disc - Amt Disc% Item - Name Ean - Code HSN QTY MRP Net - Amt Tax - Rate TaxAnirban GhoshNo ratings yet

- 3rd GovAcc 1SAY2324Document9 pages3rd GovAcc 1SAY2324Grand DuelistNo ratings yet

- Selected Banking Sector Data - Q4 2020Document39 pagesSelected Banking Sector Data - Q4 2020Nuriell OzNo ratings yet

- Final Reviewer Mathematics InvestmentDocument2 pagesFinal Reviewer Mathematics InvestmentChello Ann AsuncionNo ratings yet

- FS Complete 31 12 2007Document160 pagesFS Complete 31 12 2007samir dasNo ratings yet

- 2017documentary Requirements Lending Company Head OfficeDocument1 page2017documentary Requirements Lending Company Head OfficeLawrence PiNo ratings yet

- Presentaton On Review of LiteratureDocument27 pagesPresentaton On Review of LiteraturearchitNo ratings yet

- TT10 QuestionDocument1 pageTT10 QuestionUyển Nhi TrầnNo ratings yet

- CHINAMART 1 - PresentationDocument6 pagesCHINAMART 1 - PresentationRetro GirlNo ratings yet

- Report Financial ManagementDocument30 pagesReport Financial ManagementRishelle Mae C. AcademíaNo ratings yet

- Project Report On Analysis OF Investor's Perception Towards Derivatives As An Investment StrategyDocument99 pagesProject Report On Analysis OF Investor's Perception Towards Derivatives As An Investment StrategycityNo ratings yet

- Classification of AccountsDocument12 pagesClassification of AccountsNaurah Atika DinaNo ratings yet

- Chattel Mortgage Without Separate Promissory NoteDocument2 pagesChattel Mortgage Without Separate Promissory NoteJson GalvezNo ratings yet

- Lecture - Interest Rate SwapDocument26 pagesLecture - Interest Rate SwapKamran AbdullahNo ratings yet

- The Indian Capital Market - An Overview: Chapter-1 Gagandeep SinghDocument45 pagesThe Indian Capital Market - An Overview: Chapter-1 Gagandeep SinghgaganNo ratings yet

- Insurance MRPDocument30 pagesInsurance MRPritesh0201100% (1)

- Consumption Savings and InvestmentDocument32 pagesConsumption Savings and InvestmentVijay Chelani0% (1)

- Law 1.2Document7 pagesLaw 1.2CharlesNo ratings yet

- Factors Affecting Exchange RatesDocument2 pagesFactors Affecting Exchange Ratesanish-kc-8151No ratings yet

- Management July - New ModuleDocument160 pagesManagement July - New Moduletiglu nanoNo ratings yet

- Government of Pakistan Planning Commission Pc-1 Form (Social Sectors)Document6 pagesGovernment of Pakistan Planning Commission Pc-1 Form (Social Sectors)Usman Mani0% (1)

- Yijia Yijia Yijia Yijia Biz BIZ BIZ Biz Limited Limited Limited LimitedDocument1 pageYijia Yijia Yijia Yijia Biz BIZ BIZ Biz Limited Limited Limited LimitedMarcelo PeraltaNo ratings yet

- Sam Chapter - IDocument13 pagesSam Chapter - IsamsanthanamNo ratings yet

- 2017 ReportDocument67 pages2017 Reportআত্মজীবনীNo ratings yet

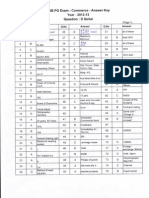

- TRB Commerce - PG - Answer Key 2012Document2 pagesTRB Commerce - PG - Answer Key 2012babu4in1No ratings yet