You might also like

- Schaum's Outline of Principles of Accounting I, Fifth EditionFrom EverandSchaum's Outline of Principles of Accounting I, Fifth EditionRating: 5 out of 5 stars5/5 (3)

- AfarDocument128 pagesAfarlloyd77% (57)

- Afar PDFDocument128 pagesAfar PDFMelyn Bustamante100% (1)

- Political Law ReviewerDocument188 pagesPolitical Law ReviewerJaelein Nicey A. MonteclaroNo ratings yet

- Corporate Financial AnalysisDocument21 pagesCorporate Financial AnalysisMOHD.ARISH100% (1)

- How to read French Financial StatementsDocument4 pagesHow to read French Financial StatementsPurmah Vik100% (1)

- Petrol Pump Project ReportDocument3 pagesPetrol Pump Project ReportShubham50% (2)

- Pals Legal Ethics ReviewedDocument66 pagesPals Legal Ethics ReviewedRaymund Christian Ong AbrantesNo ratings yet

- Finova - PD Format Oct 2019Document8 pagesFinova - PD Format Oct 2019Madhusudan ParwalNo ratings yet

- IPC Transcript 4 Manresa FULL - 4th YrDocument44 pagesIPC Transcript 4 Manresa FULL - 4th YrRaymund Christian Ong AbrantesNo ratings yet

- FAR Problem Quiz 1 SolDocument3 pagesFAR Problem Quiz 1 SolEdnalyn CruzNo ratings yet

- BIR Form 1905 PDFDocument2 pagesBIR Form 1905 PDFHeidi85% (13)

- BIR Form 1905 PDFDocument2 pagesBIR Form 1905 PDFHeidi85% (13)

- Suggested Answers in Civil Law Bar Exams1990 2006Document154 pagesSuggested Answers in Civil Law Bar Exams1990 2006Raymund Christian Ong AbrantesNo ratings yet

- Merchandising - Completing The Cycle 1 - Christine Santos BagsDocument12 pagesMerchandising - Completing The Cycle 1 - Christine Santos BagsJowelyn Casignia100% (3)

- Power Markets and Economics: Energy Costs, Trading, EmissionsFrom EverandPower Markets and Economics: Energy Costs, Trading, EmissionsNo ratings yet

- Civil Procedure Rules GuideDocument239 pagesCivil Procedure Rules GuideRaymund Christian Ong AbrantesNo ratings yet

- Acctg Module 1 QuarterDocument22 pagesAcctg Module 1 QuarterAlthea Escarpe MartinezNo ratings yet

- Afar SolutionDocument8 pagesAfar SolutionAsnifah AlinorNo ratings yet

- AUD315 Q2 quiz accounting problems and solutionsDocument6 pagesAUD315 Q2 quiz accounting problems and solutionsLorraineMartinNo ratings yet

- TrialBal (1) - 2Document1 pageTrialBal (1) - 2shreygautam12No ratings yet

- SOLUTION FUNAC FINALEXAM2019 20 1Document21 pagesSOLUTION FUNAC FINALEXAM2019 20 1Rynette FloresNo ratings yet

- Pasahol-Far-Adjusting Entries 2Document7 pagesPasahol-Far-Adjusting Entries 2Angel Pasahol100% (1)

- Fin Accts 2 AdditionalDocument5 pagesFin Accts 2 AdditionalChevonne OatesNo ratings yet

- Intac QuizDocument4 pagesIntac QuizPamela Joy AlvarezNo ratings yet

- 5.ast - Installment & FranchisingDocument12 pages5.ast - Installment & FranchisingElaineJrV-IgotNo ratings yet

- Solution in Partnership Liquidation LumpsumDocument4 pagesSolution in Partnership Liquidation LumpsumNikki GarciaNo ratings yet

- Receivables Practice SolvingDocument15 pagesReceivables Practice SolvingddalgisznNo ratings yet

- 1.november - 2018 - Monthly - ReportDocument1 page1.november - 2018 - Monthly - ReportShafin2008No ratings yet

- Financial Statement Preparation from Adjusted Trial BalanceDocument1 pageFinancial Statement Preparation from Adjusted Trial BalanceJohn Michael Gaoiran GajotanNo ratings yet

- Review Answer SheetDocument13 pagesReview Answer SheetKeycee Rhaye RivasNo ratings yet

- Kunci Quiz 3 Bond BaruDocument1 pageKunci Quiz 3 Bond BaruKoko D'DemonsongNo ratings yet

- Trial BalDocument1 pageTrial Balvihanjangid223No ratings yet

- REBYUDocument16 pagesREBYUChi EstrellaNo ratings yet

- FAR Problem Quiz 2Document3 pagesFAR Problem Quiz 2Ednalyn CruzNo ratings yet

- Trial BalanceDocument1 pageTrial Balancebhoomika.shah0624No ratings yet

- Chapter 06 - AdjustmentsDocument26 pagesChapter 06 - AdjustmentsMkhonto Xulu100% (1)

- Accounting For Special Transactions and Business CombinationsDocument3 pagesAccounting For Special Transactions and Business CombinationsJustine Reine CornicoNo ratings yet

- Book 1Document4 pagesBook 1almira garciaNo ratings yet

- ShubhamTrial PDFDocument1 pageShubhamTrial PDFI am DannyHNo ratings yet

- Kaya Mo Yan-Finac - Investment PropertyDocument8 pagesKaya Mo Yan-Finac - Investment PropertyTrixie JeramieNo ratings yet

- Final Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDocument3 pagesFinal Summative Assessment - Ae112 (1St Sem 2020-2021) - Quiz 1 Suggested Key AnswerDjunah ArellanoNo ratings yet

- FIRST PB FAR Solutions PDFDocument6 pagesFIRST PB FAR Solutions PDFStephanie Joy NogollosNo ratings yet

- Illustration PRAC - AUD Page 13Document4 pagesIllustration PRAC - AUD Page 13The BoxNo ratings yet

- 22 25 AstDocument10 pages22 25 AstJotaro KujoNo ratings yet

- Answer Key Quiz 5 Actbas2 T3 PDFDocument5 pagesAnswer Key Quiz 5 Actbas2 T3 PDFCharles TuazonNo ratings yet

- Worksheet - Service - Cotton CompanyDocument7 pagesWorksheet - Service - Cotton CompanyJasmine ActaNo ratings yet

- Chapter 27Document12 pagesChapter 27Crizel DarioNo ratings yet

- Kaya Mo Yan-Finac - Chap 22 Investment PropertyDocument8 pagesKaya Mo Yan-Finac - Chap 22 Investment PropertyTrixie JeramieNo ratings yet

- Accounting AssignmentDocument13 pagesAccounting AssignmentPetrinaNo ratings yet

- Prelim SolutionDocument5 pagesPrelim SolutionMst TeriousNo ratings yet

- Case 1Document6 pagesCase 1Nicolyn Rae EscalanteNo ratings yet

- Case 1Document6 pagesCase 1Nicolyn Rae EscalanteNo ratings yet

- FPQ1 - Answer KeyDocument6 pagesFPQ1 - Answer KeyJi YuNo ratings yet

- MASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Document35 pagesMASTERY CLASS IN AUDITING PROBLEMS Part 1 Prob 1 9Mark Gelo WinchesterNo ratings yet

- 1-1hkg 2002 Dec ADocument8 pages1-1hkg 2002 Dec AWing Yan KatieNo ratings yet

- Homework SolutionsDocument5 pagesHomework SolutionsAnonymous CuUAaRSNNo ratings yet

- Computation For Exercise 1Document10 pagesComputation For Exercise 1Xyzra AlfonsoNo ratings yet

- Activity (Worksheet Preparation)Document3 pagesActivity (Worksheet Preparation)Lehnard Delos Reyes GellorNo ratings yet

- ACCT 4410 Depreciation Allowance Illustration (DA) (2023S)Document2 pagesACCT 4410 Depreciation Allowance Illustration (DA) (2023S)何健珩No ratings yet

- Accounts List Summary PDFDocument2 pagesAccounts List Summary PDFOkie FernandaNo ratings yet

- Part 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalDocument8 pagesPart 1 Examination - Paper 1.1 (INT) Preparing Financial Statements (InternationalAUDITOR97No ratings yet

- P and L and BSDocument8 pagesP and L and BSgautam48128No ratings yet

- Trial BalDocument1 pageTrial BalSun ShineNo ratings yet

- Chapter 1 - Teacher's Manual - Afar Part 1-1Document10 pagesChapter 1 - Teacher's Manual - Afar Part 1-1Mayeth BotinNo ratings yet

- Cash Management Chapter: Cash Budgets and ForecastingDocument5 pagesCash Management Chapter: Cash Budgets and ForecastingMukul KadyanNo ratings yet

- R&L Company: Assignment 1 Premium Liability, Warranty LiabilityDocument6 pagesR&L Company: Assignment 1 Premium Liability, Warranty Liabilityangelian bagadiongNo ratings yet

- Civil Law CasesDocument23 pagesCivil Law CasesRaymund Christian Ong AbrantesNo ratings yet

- Rediscovering the Resulting TrustDocument22 pagesRediscovering the Resulting TrustRaymund Christian Ong AbrantesNo ratings yet

- Dissolution-Changes in OwnershipDocument72 pagesDissolution-Changes in OwnershipmonneNo ratings yet

- 2013-2014 Remedial CasesDocument42 pages2013-2014 Remedial CasesRaymund Christian Ong AbrantesNo ratings yet

- Civil Law CasesDocument161 pagesCivil Law CasesRaymund Christian Ong AbrantesNo ratings yet

- Affidavit of Support for Travel VisaDocument1 pageAffidavit of Support for Travel VisaRaymund Christian Ong AbrantesNo ratings yet

- Sample of Employment Contact PT EngDocument3 pagesSample of Employment Contact PT EngjaciemNo ratings yet

- GR 192602 2017 PDFDocument8 pagesGR 192602 2017 PDFRaymund Christian Ong AbrantesNo ratings yet

- A PProblems (1) TiltonDocument30 pagesA PProblems (1) TiltonDana FrankNo ratings yet

- Inc in ACS RequirementDocument1 pageInc in ACS RequirementRaymund Christian Ong AbrantesNo ratings yet

- Willes 715Document31 pagesWilles 715Raymund Christian Ong AbrantesNo ratings yet

- GDocument4 pagesGRaymund Christian Ong AbrantesNo ratings yet

- General Banking Law - CompiledDocument35 pagesGeneral Banking Law - CompiledRaymund Christian Ong AbrantesNo ratings yet

- BIR Ruling No. 10-03, Sept. 8, 2003Document2 pagesBIR Ruling No. 10-03, Sept. 8, 2003Thomas EdisonNo ratings yet

- Cons TiDocument12 pagesCons TiRaymund Christian Ong AbrantesNo ratings yet

- Cred Tran1Document9 pagesCred Tran1Raymund Christian Ong AbrantesNo ratings yet

- Summary ProcedureDocument10 pagesSummary ProcedureRaymund Christian Ong AbrantesNo ratings yet

- Construction/Limitations, Section 3 of The COMELEC Rules of ProcedureDocument9 pagesConstruction/Limitations, Section 3 of The COMELEC Rules of ProcedureRaymund Christian Ong AbrantesNo ratings yet

- Lecture Notes On Financial ForecastingDocument7 pagesLecture Notes On Financial Forecastingpalkee100% (3)

- Ar 2011Document36 pagesAr 2011Micheal J JacsonNo ratings yet

- Create online test papersDocument9 pagesCreate online test papersNihalSoniNo ratings yet

- T.1042 Maliyy T Hlili Aynur F NdiyevaDocument15 pagesT.1042 Maliyy T Hlili Aynur F NdiyevaelvitaNo ratings yet

- Acct2302 E3Document12 pagesAcct2302 E3zeeshan100% (1)

- CF Jan 11 Leong Khai Heng 7640044Document11 pagesCF Jan 11 Leong Khai Heng 7640044vivianleongNo ratings yet

- HDFC Bank Balance Sheet and Profit Loss ReportsDocument7 pagesHDFC Bank Balance Sheet and Profit Loss ReportsSunny_Chatlani_8157No ratings yet

- Answer Sheet Week 7 & 8Document5 pagesAnswer Sheet Week 7 & 8Jamel Khia Albarando LisondraNo ratings yet

- Revision NotesDocument51 pagesRevision NotesMelody RoseNo ratings yet

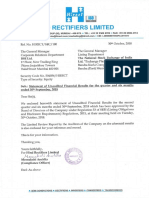

- Hind Rectifiers Financial Results for Q2FY19Document5 pagesHind Rectifiers Financial Results for Q2FY19javadeveloper lokeshNo ratings yet

- Pertemuan 1 - Hutang LancarDocument14 pagesPertemuan 1 - Hutang LancarSalma Nur AzizahNo ratings yet

- Balance Sheet of Bharti AirtelDocument7 pagesBalance Sheet of Bharti Airteltiku_048No ratings yet

- PROBSETz FARDocument6 pagesPROBSETz FARAi MelNo ratings yet

- EP60010 Funding New Venture PDFDocument2 pagesEP60010 Funding New Venture PDFRajat AgrawalNo ratings yet

- Arwana Citramulia TBK - 30 - 06 - 2021 - ReleasedDocument85 pagesArwana Citramulia TBK - 30 - 06 - 2021 - ReleasedM Fany AFNo ratings yet

- Taxation Law Mock BarDocument8 pagesTaxation Law Mock BarKC ManglapusNo ratings yet

- Accounting For Special Transaction 1Document9 pagesAccounting For Special Transaction 1Timon CarandangNo ratings yet

- Management's Restructuring PlansDocument1 pageManagement's Restructuring PlansHeaven HeartNo ratings yet

- Indian Economy On The Eve of IndependenceDocument37 pagesIndian Economy On The Eve of Independencezeeshanahmad11167% (3)

- Restaurant MirchiDocument32 pagesRestaurant MirchiDavidChenNo ratings yet

- Cma2 Ch2 Mgmt@DuDocument16 pagesCma2 Ch2 Mgmt@DuGosaye AbebeNo ratings yet

- Asahi Songwon performance back to normal after capacity expansionDocument6 pagesAsahi Songwon performance back to normal after capacity expansionshahavNo ratings yet

- Relevant CostsDocument46 pagesRelevant CostsManzzie100% (1)

- Research and Analysis Case 1Document3 pagesResearch and Analysis Case 1Jessica Harden McManigalNo ratings yet

- Exercise 5-5Document2 pagesExercise 5-5Ammar TuahNo ratings yet

- 305 FinalDocument33 pages305 FinalsmithteeNo ratings yet