You might also like

- Welding Quality ControlDocument7 pagesWelding Quality ControlPRAMOD KUMAR SETHI S100% (1)

- HDFC LifeDocument66 pagesHDFC LifeChetan PahwaNo ratings yet

- Insurance Black BookDocument61 pagesInsurance Black BookKunal Charaniya100% (1)

- A Comparative Study of Life Insurance and Private CompanyDocument16 pagesA Comparative Study of Life Insurance and Private CompanyHarshvardhan RathoreNo ratings yet

- Jussie Smollett's Emergency MotionDocument393 pagesJussie Smollett's Emergency MotionLouis R. FasulloNo ratings yet

- Commercial Lendings by BanksDocument65 pagesCommercial Lendings by Banksvivek satviNo ratings yet

- Ic-11-Practice of General Insurance PDFDocument287 pagesIc-11-Practice of General Insurance PDFprabhat87aish40% (5)

- Padua Vs PeopleDocument1 pagePadua Vs PeopleKlaire EsdenNo ratings yet

- Motor Vehicle Insurance (9930380385 Contac Me - ) ) - 80754995-1Document70 pagesMotor Vehicle Insurance (9930380385 Contac Me - ) ) - 80754995-1RiSHI KeSH GawaINo ratings yet

- "PROFITABILITY OF LIFE INSURANCE" Shailesh Kumar Singh and Prof. Peeyush Kumar PandeyDocument9 pages"PROFITABILITY OF LIFE INSURANCE" Shailesh Kumar Singh and Prof. Peeyush Kumar PandeySourya Pratap SinghNo ratings yet

- Insurance Sector of India Project ReportDocument81 pagesInsurance Sector of India Project ReportsnehkareerNo ratings yet

- Taxation As A Tool For Selling Life Insurance For IDBI Federal Life Insurance Co LTDDocument33 pagesTaxation As A Tool For Selling Life Insurance For IDBI Federal Life Insurance Co LTDAbhishek Singh0% (1)

- Brand Image of Icici Prudential Life InsuranceDocument40 pagesBrand Image of Icici Prudential Life InsuranceShehbaz KhannaNo ratings yet

- India's Insurance Sector History and Current StateDocument10 pagesIndia's Insurance Sector History and Current StateAman AmuNo ratings yet

- Insurance Project On ULIP-K JAINDocument66 pagesInsurance Project On ULIP-K JAINkhushboo_jain100% (1)

- Regional Rural Banks of India: Evolution, Performance and ManagementFrom EverandRegional Rural Banks of India: Evolution, Performance and ManagementNo ratings yet

- InsuranceDocument82 pagesInsuranceNikesh KothariNo ratings yet

- Study of Customer Perception Towards Insurance ServicesDocument65 pagesStudy of Customer Perception Towards Insurance Servicesanon_209987870No ratings yet

- Pacific Farms V Esguerra (1969)Document3 pagesPacific Farms V Esguerra (1969)Zan BillonesNo ratings yet

- Training and Development in BHARTI AXA Life InsuranceDocument73 pagesTraining and Development in BHARTI AXA Life Insuranceankitasachaan89No ratings yet

- CHANGES IN INSURANCE SECTOR (A Study On Public Awareness)Document47 pagesCHANGES IN INSURANCE SECTOR (A Study On Public Awareness)Ramaduta80% (5)

- Shriram Transport Finance Company LTD, MeghanDocument26 pagesShriram Transport Finance Company LTD, MeghanAnil Bambule100% (1)

- LICDocument8 pagesLICCharmi Joshi100% (1)

- Credit RatingDocument48 pagesCredit RatingChinmayee ChoudhuryNo ratings yet

- Reliance Life Insurance ReportDocument116 pagesReliance Life Insurance ReportTimothy Brown100% (1)

- Royal Sundaram General InsuranceDocument22 pagesRoyal Sundaram General InsuranceVinayak BhardwajNo ratings yet

- Report On BhartiDocument57 pagesReport On BhartiWendy CannonNo ratings yet

- Background and History of LICDocument82 pagesBackground and History of LICVittalrao Kilikile100% (1)

- Chapter - 1 Introduction To Insurance in India: Vivek College of CommerceDocument69 pagesChapter - 1 Introduction To Insurance in India: Vivek College of CommerceRutu_Ko_7037No ratings yet

- General InsuranceDocument85 pagesGeneral InsuranceNiket Dattani0% (2)

- Research On Life InsuranceDocument90 pagesResearch On Life InsuranceDhananjay SharmaNo ratings yet

- India Life Insurance Sector: Incentive Structures To Deliver Optimal ResultsDocument8 pagesIndia Life Insurance Sector: Incentive Structures To Deliver Optimal ResultssolukoyaNo ratings yet

- New Black Book General Insurance 2017Document69 pagesNew Black Book General Insurance 2017Siddhesh VarerkarNo ratings yet

- Brief History of InsuranceDocument9 pagesBrief History of InsuranceVijay100% (1)

- Birla Sun Life InsuranceDocument21 pagesBirla Sun Life Insurancecharu100% (3)

- Technicalites of Health Insurance: Underwriting, Actuarial, Reinsurance, TPA and Claims For Order: Harish@Document4 pagesTechnicalites of Health Insurance: Underwriting, Actuarial, Reinsurance, TPA and Claims For Order: Harish@Harish SihareNo ratings yet

- Reliance General Insurance Company LimitedDocument15 pagesReliance General Insurance Company LimitedSakshi DamwaniNo ratings yet

- Finacial Performance of Life InsuracneDocument24 pagesFinacial Performance of Life InsuracneCryptic LollNo ratings yet

- Presentation On Kotak Life InsuranceDocument15 pagesPresentation On Kotak Life Insurancehitesh38560% (1)

- Money Market in India: Presented By: Manish Jain Mridul Chawla Kunal GoelDocument22 pagesMoney Market in India: Presented By: Manish Jain Mridul Chawla Kunal Goelkunal goelNo ratings yet

- Shriram Llife Insurance Intership ProgrammeDocument9 pagesShriram Llife Insurance Intership ProgrammeGOMATHI VNo ratings yet

- Findings: Planning, Risk Coverage and SecuritiesDocument3 pagesFindings: Planning, Risk Coverage and SecuritiesManish RavatNo ratings yet

- Introduction to EXIM Bank's Objectives and OperationsDocument49 pagesIntroduction to EXIM Bank's Objectives and OperationsShruti Vikram0% (1)

- How Actuaries Help Plan for an Uncertain FutureDocument12 pagesHow Actuaries Help Plan for an Uncertain FuturePrajakta Kadam67% (3)

- Insurance SectorDocument38 pagesInsurance SectorAjyPriNo ratings yet

- Money Back PolicyDocument58 pagesMoney Back PolicyUppal Patel83% (6)

- Consumer Behavior & Customer Satisfaction Towards ICICI PrudDocument99 pagesConsumer Behavior & Customer Satisfaction Towards ICICI PrudShahzad SaifNo ratings yet

- Star CompanyDocument15 pagesStar CompanyCandsz JcaNo ratings yet

- Types of NBFCDocument16 pagesTypes of NBFCathiraNo ratings yet

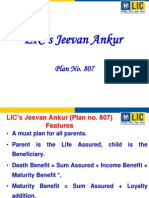

- Jeevan Ankur Ppt-Eng - LIC - 9884635430 - Child PlanDocument17 pagesJeevan Ankur Ppt-Eng - LIC - 9884635430 - Child PlanBabujee K.NNo ratings yet

- Indian Insurance Industry "An Overview"Document80 pagesIndian Insurance Industry "An Overview"Sharmili SanchitaNo ratings yet

- SBI Merger Boosts Size But Raises Stability RisksDocument9 pagesSBI Merger Boosts Size But Raises Stability RisksPrabhujot SinghNo ratings yet

- Debt MarketDocument104 pagesDebt MarketOmkar Rohekar100% (1)

- Liberalisation of Insurance Services RefinedDocument22 pagesLiberalisation of Insurance Services RefinedJojin JoseNo ratings yet

- Black Book 05Document68 pagesBlack Book 05vishal vhatkarNo ratings yet

- Project Report Lic IshwarDocument44 pagesProject Report Lic IshwarAbhi TiwariNo ratings yet

- DineshDocument62 pagesDineshDinesh KumarNo ratings yet

- Life Insurance ProjectDocument73 pagesLife Insurance ProjectSanthosh SomaNo ratings yet

- SharanDocument62 pagesSharanRaj KumarNo ratings yet

- New Water RatesDocument83 pagesNew Water RatesScott FisherNo ratings yet

- MID-TERM EXAM ANSWER SHEETDocument11 pagesMID-TERM EXAM ANSWER SHEETbLaXe AssassinNo ratings yet

- Percentage Tax CTBDocument16 pagesPercentage Tax CTBDon CabasiNo ratings yet

- BP 22 NotesDocument2 pagesBP 22 NotesBay Ariel Sto TomasNo ratings yet

- Download free font with copyright infoDocument2 pagesDownload free font with copyright infoMaria CazacuNo ratings yet

- Test Bank 8Document13 pagesTest Bank 8Jason Lazaroff67% (3)

- OpenSAP Signavio1 Week 1 Unit 1 Intro PresentationDocument8 pagesOpenSAP Signavio1 Week 1 Unit 1 Intro PresentationMoyin OluwaNo ratings yet

- Guntaiah Vs Hambamma Air 2005 SC 4013Document6 pagesGuntaiah Vs Hambamma Air 2005 SC 4013Sridhara babu. N - ಶ್ರೀಧರ ಬಾಬು. ಎನ್100% (2)

- Form 1. Application For Travel and Accommodation Assistance - April 2019Document4 pagesForm 1. Application For Travel and Accommodation Assistance - April 2019chris tNo ratings yet

- E-Ticket: Travel InformationDocument2 pagesE-Ticket: Travel InformationAli BajwaNo ratings yet

- TIK Single Touch Payroll Processing GuideDocument23 pagesTIK Single Touch Payroll Processing GuideMargaret MationgNo ratings yet

- Declaratory ReliefDocument14 pagesDeclaratory ReliefJulius AlcantaraNo ratings yet

- B'H' What Is Shabbat Hagadol: The Household, A Lamb For Each Home (Document10 pagesB'H' What Is Shabbat Hagadol: The Household, A Lamb For Each Home (ජෛන සොහ්රාබ්No ratings yet

- A Proposal Made By: Shashwat Pratyush Roll No: 1761 Class: B.A.LL.B. (Hons.) Semester: 5Document30 pagesA Proposal Made By: Shashwat Pratyush Roll No: 1761 Class: B.A.LL.B. (Hons.) Semester: 5Shashwat PratyushNo ratings yet

- Autodesk® Revit® Structure Benutzerhandbuch (PDFDrive)Document1,782 pagesAutodesk® Revit® Structure Benutzerhandbuch (PDFDrive)ercNo ratings yet

- Pornography LawsDocument177 pagesPornography Lawsvishnu000No ratings yet

- English Department Phrasal Verbs LessonDocument6 pagesEnglish Department Phrasal Verbs LessonCarolina AndreaNo ratings yet

- RemLaw Transcript - Justice Laguilles Pt. 2Document25 pagesRemLaw Transcript - Justice Laguilles Pt. 2Mark MagnoNo ratings yet

- Problem For Practice: Accounting For Merchandise CompanyDocument1 pageProblem For Practice: Accounting For Merchandise CompanySiam FarhanNo ratings yet

- Purisima Vs Phil TobaccoDocument4 pagesPurisima Vs Phil TobaccoJohnde Martinez100% (1)

- Journal Reading 2 - Dr. Citra Manela, SP.F PDFDocument15 pagesJournal Reading 2 - Dr. Citra Manela, SP.F PDFSebrin FathiaNo ratings yet

- Davao City Water District vs. CSCDocument15 pagesDavao City Water District vs. CSCJudy Ann BilangelNo ratings yet

- Factsheet Alcohol and Risk TakingDocument2 pagesFactsheet Alcohol and Risk TakingDanny EnvisionNo ratings yet

- Compiled Digest PFR - Rev.1Document38 pagesCompiled Digest PFR - Rev.1Song Ong100% (1)

- Privacy and Personal Profiles in Web SearchDocument4 pagesPrivacy and Personal Profiles in Web SearchAlHasan Al-SamaraeNo ratings yet

- LG Eva MSDSDocument8 pagesLG Eva MSDSpbNo ratings yet