You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ICFAI MIFA Course Group C Financial Markets Exam - Paper1Document27 pagesICFAI MIFA Course Group C Financial Markets Exam - Paper1Ameya RanadiveNo ratings yet

- Bus Com 3Document11 pagesBus Com 3Shiela Mae RedobleNo ratings yet

- Aldi RetailDocument32 pagesAldi RetailVVM100% (1)

- Final Exam MarketingDocument17 pagesFinal Exam MarketingABDUL AHADNo ratings yet

- Abm Apec Airs LM q1 w3 Lc4-5no-KeyanswerDocument15 pagesAbm Apec Airs LM q1 w3 Lc4-5no-KeyanswerKathleen Joyce ParangatNo ratings yet

- 4 Infibeam IPO Case StudyDocument2 pages4 Infibeam IPO Case StudychinmayNo ratings yet

- Tribal EconomyDocument11 pagesTribal EconomyNitisha GeedNo ratings yet

- Business Objectives and Stakeholder ObjectivesDocument4 pagesBusiness Objectives and Stakeholder ObjectivesVincent ChurchillNo ratings yet

- The Impact of Digital Marketing Communications On Consumers Brand Loyality Case Study of SOUMMAM BrandDocument18 pagesThe Impact of Digital Marketing Communications On Consumers Brand Loyality Case Study of SOUMMAM BrandBrahim BrahimNo ratings yet

- Marketing Real People Real Choices Global Edition 11Th Edition Michael Solomon Full ChapterDocument67 pagesMarketing Real People Real Choices Global Edition 11Th Edition Michael Solomon Full Chapterdyan.myers838100% (5)

- Digital MarketingDocument23 pagesDigital MarketingKonarkRawatNo ratings yet

- Boundaries of Firm EssayDocument6 pagesBoundaries of Firm EssayRajvinder BhachuNo ratings yet

- Ipa Crisis in Creative Effectiveness 2019Document25 pagesIpa Crisis in Creative Effectiveness 2019Jeffri Tanamal100% (2)

- Saptamana 4 Read The Information Carefully:: What Sales Thinks About Marketing?Document4 pagesSaptamana 4 Read The Information Carefully:: What Sales Thinks About Marketing?Delia LupascuNo ratings yet

- SLHT Business Finance WEEK 910Document7 pagesSLHT Business Finance WEEK 910Ian OcheaNo ratings yet

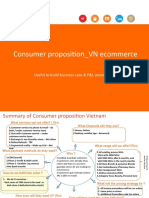

- Consumer Proposition - VN Ecommerce: Useful To Build Business Case & P&L AssumptionsDocument3 pagesConsumer Proposition - VN Ecommerce: Useful To Build Business Case & P&L AssumptionsvuquyhaiNo ratings yet

- DHL New RatesDocument12 pagesDHL New Ratessandeep12416No ratings yet

- Internship Report Front PageDocument6 pagesInternship Report Front PageNadim MahamudNo ratings yet

- Nature and Scope of GST: by Amandeep DrallDocument8 pagesNature and Scope of GST: by Amandeep DrallAman SinghNo ratings yet

- Furniture Order-MorletDocument1 pageFurniture Order-MorletroberthohdezNo ratings yet

- Instruction & CaseletDocument82 pagesInstruction & CaseletAnonymous 6Ht1ec0% (1)

- Texto en Ingles Finanzas CorporativasDocument2 pagesTexto en Ingles Finanzas CorporativasyercaNo ratings yet

- Briefing Paper No 3 CV Market Update 15 11 17 PDFDocument6 pagesBriefing Paper No 3 CV Market Update 15 11 17 PDFAlex WoodrowNo ratings yet

- 02 - The Bascis of Supply and Demand - sp2017Document50 pages02 - The Bascis of Supply and Demand - sp2017Tamil LearningNo ratings yet

- International Business: Marketing GloballyDocument23 pagesInternational Business: Marketing GloballyDavid KadeNo ratings yet

- Final Exam Bsma 1a June 15Document12 pagesFinal Exam Bsma 1a June 15Maeca Angela SerranoNo ratings yet

- Vanessa Joy V. Baluyut Grade Level: 11 Subject: Applied EconomicsDocument2 pagesVanessa Joy V. Baluyut Grade Level: 11 Subject: Applied Economicsvaniique100% (2)

- FESCO ONLINE BILL - CompressedDocument1 pageFESCO ONLINE BILL - CompressedInternal Audit FESCONo ratings yet

- SFM Theory Important Questions Notes by @divyesh - VaghelaDocument27 pagesSFM Theory Important Questions Notes by @divyesh - Vaghelasneh.officialworkNo ratings yet

- Chapter 01 Testbank: of Mcgraw-Hill EducationDocument58 pagesChapter 01 Testbank: of Mcgraw-Hill EducationshivnilNo ratings yet