You might also like

- SINGAPORE INVESTORS FUNDDocument2 pagesSINGAPORE INVESTORS FUNDNadeem LalaniNo ratings yet

- Stitch Fix Inc NasdaqGS SFIX FinancialsDocument41 pagesStitch Fix Inc NasdaqGS SFIX FinancialsanamNo ratings yet

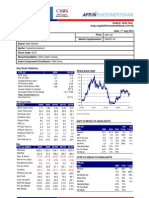

- Hiap Teck RN 20100701 AffinDocument3 pagesHiap Teck RN 20100701 Affinlimml63No ratings yet

- Bank of Japan: Monthly Report On The Corporate Goods Price IndexDocument8 pagesBank of Japan: Monthly Report On The Corporate Goods Price IndexHong AnhNo ratings yet

- Cambodia 2009Document2 pagesCambodia 2009Sry NeathNo ratings yet

- Pakistan State Oil Company Limited (Pso)Document6 pagesPakistan State Oil Company Limited (Pso)Maaz HanifNo ratings yet

- Black Gold - AnalysisDocument12 pagesBlack Gold - AnalysisAbdulrahman DhabaanNo ratings yet

- Roku Inc (ROKU US) - AdjustedDocument9 pagesRoku Inc (ROKU US) - Adjustedjustinbui85No ratings yet

- Birla Sun Life 95 Fund performance and returnsDocument9 pagesBirla Sun Life 95 Fund performance and returnsCompu ServNo ratings yet

- Econ of ActsDocument1 pageEcon of ActsChris GobbiNo ratings yet

- Lyxor China Case SolutionDocument4 pagesLyxor China Case SolutionSyeda Alisha FatimaNo ratings yet

- LG Electronics 4Q'19 Earnings ReleaseDocument19 pagesLG Electronics 4Q'19 Earnings ReleaseОverlord 4No ratings yet

- 6 Japan and The Rest of Asia (2020!08!15 14-09-52 UTC)Document17 pages6 Japan and The Rest of Asia (2020!08!15 14-09-52 UTC)Robert TirtawigoenaNo ratings yet

- Traxis Fund Confidential: Performance Review - February 28Document17 pagesTraxis Fund Confidential: Performance Review - February 28ZerohedgeNo ratings yet

- Mangalam Seeds CashflowDocument2 pagesMangalam Seeds Cashflowgraheeth26No ratings yet

- Colombian Fiscal PolicyDocument24 pagesColombian Fiscal PolicyAndres OlayaNo ratings yet

- ValueResearchFundcard KotakGiltInvestmentRegular 2010nov24Document6 pagesValueResearchFundcard KotakGiltInvestmentRegular 2010nov24zankurNo ratings yet

- Overview of the International Sukuk Market in 2020Document6 pagesOverview of the International Sukuk Market in 2020Febyyanita MirzaNo ratings yet

- Ii. Fiscal Situation: Combined Government Finances: 2008-09Document7 pagesIi. Fiscal Situation: Combined Government Finances: 2008-09gkmishra2001 at gmail.comNo ratings yet

- Fortis Healthcare Limited BSE 532843 FinancialsDocument44 pagesFortis Healthcare Limited BSE 532843 Financialsakumar4uNo ratings yet

- Bank Appraisal Memo For CC TLDocument16 pagesBank Appraisal Memo For CC TLYash BaneNo ratings yet

- FDI in PakistanDocument17 pagesFDI in PakistanGhulam HussainNo ratings yet

- Anual Nationa AccountsDocument2 pagesAnual Nationa AccountsVinay MadgavkarNo ratings yet

- ValueResearchFundcard HDFCEquity 2012jul30Document6 pagesValueResearchFundcard HDFCEquity 2012jul30Rachit GoyalNo ratings yet

- Tesco Financials - Capital IQDocument48 pagesTesco Financials - Capital IQÑízãr ÑzrNo ratings yet

- 2016 Q2 Presentation 01Document9 pages2016 Q2 Presentation 01Floppy gsellNo ratings yet

- 28658920-95a5-49ed-80cf-1c8bf1c4d9d3.xlsxDocument1 page28658920-95a5-49ed-80cf-1c8bf1c4d9d3.xlsxM AneeshwarNo ratings yet

- Profitability: 31-Dec Sales Ebitda Net Income EPS Euro M Euro M Euro M EuroDocument21 pagesProfitability: 31-Dec Sales Ebitda Net Income EPS Euro M Euro M Euro M Euroapi-19513024No ratings yet

- Investor Digest: Equity Research - 24 January 2022Document5 pagesInvestor Digest: Equity Research - 24 January 2022Radityo Hari WibowoNo ratings yet

- 915 529 Supplement Landmark XLS ENGDocument32 pages915 529 Supplement Landmark XLS ENGPaco ColínNo ratings yet

- Monthly Economic DataDocument2 pagesMonthly Economic Dataapi-25887578No ratings yet

- Arif Habib Sec. Ltd. Financial Performance 2011-2005Document1 pageArif Habib Sec. Ltd. Financial Performance 2011-2005Umema UsmanNo ratings yet

- Internship Report on Ratio Analysis of Jamuna BankDocument5 pagesInternship Report on Ratio Analysis of Jamuna BanksahhhhhhhNo ratings yet

- DLF Announces Annual Results For FY10: HistoryDocument7 pagesDLF Announces Annual Results For FY10: HistoryShalinee SinghNo ratings yet

- Schroder GAIA Egerton Equity: Quarterly Fund UpdateDocument7 pagesSchroder GAIA Egerton Equity: Quarterly Fund UpdatejackefellerNo ratings yet

- 20 3Q Earning Release of LGEDocument19 pages20 3Q Earning Release of LGEMandeepNo ratings yet

- Trade Deficit (Net Exports) NX Exports (X) - Imports (M) in Relation To Un-Employment and Inflation For Last 20-Years Performance-Hongkong & DenmarkDocument4 pagesTrade Deficit (Net Exports) NX Exports (X) - Imports (M) in Relation To Un-Employment and Inflation For Last 20-Years Performance-Hongkong & DenmarkShabab MansoorNo ratings yet

- Select Economic IndicatorsDocument1 pageSelect Economic Indicatorspls2019No ratings yet

- Fraport Interim Report q2 6m 2018Document36 pagesFraport Interim Report q2 6m 2018TatianaNo ratings yet

- Fund Performance: Managed Equity Dollar January 04, 2021 Money MarketDocument5 pagesFund Performance: Managed Equity Dollar January 04, 2021 Money MarketRon CatalanNo ratings yet

- Index: Yield Curve (1m) Yield Curve (6m) Yield Curve (1y)Document1 pageIndex: Yield Curve (1m) Yield Curve (6m) Yield Curve (1y)dennisjoeNo ratings yet

- Skechers USA Inc. (SKX) : (Net Income ÷ Sales) (Sales ÷ Total Assets) (Total Assets ÷ Shareholders Equity)Document2 pagesSkechers USA Inc. (SKX) : (Net Income ÷ Sales) (Sales ÷ Total Assets) (Total Assets ÷ Shareholders Equity)AndrianaAndina100% (1)

- Claas Gb14 EnDocument134 pagesClaas Gb14 Enalaynnastaabx786No ratings yet

- Pepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsDocument28 pagesPepsico, Inc. (Nasdaqgs:Pep) Financials Key StatsJulio CesarNo ratings yet

- Schroder GAIA Egerton Equity: Quarterly Fund UpdateDocument8 pagesSchroder GAIA Egerton Equity: Quarterly Fund UpdatejackefellerNo ratings yet

- Corporate Finance Profit and Loss AnalysisDocument13 pagesCorporate Finance Profit and Loss AnalysisChaitanya GembaliNo ratings yet

- 22 3Q Earning Release of LGEDocument18 pages22 3Q Earning Release of LGEIgnacio ElliotNo ratings yet

- Bank of China Limited SEHK 3988 FinancialsDocument47 pagesBank of China Limited SEHK 3988 FinancialsJaime Vara De ReyNo ratings yet

- 16 Financial HighlightsDocument2 pages16 Financial HighlightswasiumNo ratings yet

- Ashmore Investment Management Limited Asian High Yield Debt Class ZDocument3 pagesAshmore Investment Management Limited Asian High Yield Debt Class Zcena1987No ratings yet

- 1.3 Huawei Solution 04.11.2020Document10 pages1.3 Huawei Solution 04.11.2020Partha Protim SahaNo ratings yet

- United Bank Limited United Bank Limited United Bank Limited United Bank LimitedDocument34 pagesUnited Bank Limited United Bank Limited United Bank Limited United Bank LimitedZeeshan YaqubNo ratings yet

- Current Ratio Analysis of Major FMCG CompaniesDocument86 pagesCurrent Ratio Analysis of Major FMCG CompaniesMAYUGAMNo ratings yet

- 2008 A 2017 Economatica USIMINASDocument45 pages2008 A 2017 Economatica USIMINASDanny AndradeNo ratings yet

- Global Growth Weakening As Some Risks Materialise OECD Interim Economic Outlook Handout March 2019Document13 pagesGlobal Growth Weakening As Some Risks Materialise OECD Interim Economic Outlook Handout March 2019Valter SilveiraNo ratings yet

- AMOREPACIFIC 2019 Revenue Up 5.7% to KRW 5.6 TrillionDocument7 pagesAMOREPACIFIC 2019 Revenue Up 5.7% to KRW 5.6 Trillionjon jonNo ratings yet

- Eco!) @ A5Document8 pagesEco!) @ A5Vedansh shahNo ratings yet

- BHMF Risk Report March 2021 ADV012607Document6 pagesBHMF Risk Report March 2021 ADV012607danehalNo ratings yet

- Math Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesFrom EverandMath Practice Simplified: Decimals & Percents (Book H): Practicing the Concepts of Decimals and PercentagesRating: 5 out of 5 stars5/5 (3)

- Hoisington 1 Quarter 2012Document13 pagesHoisington 1 Quarter 2012pick6No ratings yet

- The Absolute Return Letter 10/11Document8 pagesThe Absolute Return Letter 10/11pick6No ratings yet

- SautDocument6 pagesSautpick6No ratings yet

- Albert Edwards On The Resurgence of TheDocument6 pagesAlbert Edwards On The Resurgence of Thepick6No ratings yet

- February 23, 2011 Interview With Dr. Marc FaberDocument10 pagesFebruary 23, 2011 Interview With Dr. Marc Faberpick6No ratings yet

- Warren Buffett 2010 Berkshire Hathaway LetterDocument27 pagesWarren Buffett 2010 Berkshire Hathaway LetterFortuneNo ratings yet

- Eclectica China CDSDocument12 pagesEclectica China CDSpick6No ratings yet

- Eclectica January ReportDocument2 pagesEclectica January Reportpick6No ratings yet

- CF Eclectica Agriculture Fund - Performance Attribution Report - December 2010Document2 pagesCF Eclectica Agriculture Fund - Performance Attribution Report - December 2010pick6No ratings yet

- TPL Jan 26 11Document18 pagesTPL Jan 26 11pick6No ratings yet

- CF Eclectica Agriculture Fund - Performance Attribution Report - January 2011Document2 pagesCF Eclectica Agriculture Fund - Performance Attribution Report - January 2011pick6No ratings yet

- Faber 012011Document22 pagesFaber 012011FlorianGeyerNo ratings yet

- Crispin Odey's Transcript Q4-10Document10 pagesCrispin Odey's Transcript Q4-10pick6No ratings yet

- Making The Best ofDocument5 pagesMaking The Best ofpick6No ratings yet

- NATIONAL SPOT EXCHANGE SCAM EXPOSEDDocument25 pagesNATIONAL SPOT EXCHANGE SCAM EXPOSEDSarvjeetNo ratings yet

- Bus - Valuation - StudentDocument5 pagesBus - Valuation - StudentMilan TilvaNo ratings yet

- Who's Holding The Bag?Document64 pagesWho's Holding The Bag?char1eylu100% (4)

- Whitney CFA Level 2 AnswerDocument6 pagesWhitney CFA Level 2 Answerprint doc100% (1)

- JetBlue Airways IPO ValuationDocument15 pagesJetBlue Airways IPO ValuationThossapron Apinyapanja0% (2)

- CorpF ReviseDocument5 pagesCorpF ReviseTrang DangNo ratings yet

- 30-Stock-Portfolio-tracker V 1 2Document18 pages30-Stock-Portfolio-tracker V 1 2SomashekharNsNo ratings yet

- Unit - Ii: Securities MarketsDocument53 pagesUnit - Ii: Securities MarketsAlavudeen ShajahanNo ratings yet

- Gamma Scalping & Pyramiding Long StraddleDocument3 pagesGamma Scalping & Pyramiding Long StraddleMayuresh Deshpande0% (2)

- TaxDocument4 pagesTaxShakti YadavNo ratings yet

- FINA3203 Solution 2Document6 pagesFINA3203 Solution 2simonsin6a30No ratings yet

- Introduction To Derivatives and Risk Management 10th Edition Chance Test BankDocument8 pagesIntroduction To Derivatives and Risk Management 10th Edition Chance Test BankMavos OdinNo ratings yet

- Activity: Basic Earnings Per ShareDocument2 pagesActivity: Basic Earnings Per Sharebi23450% (1)

- Open Interest Analysis: Trend Actio N Interpretatio N OI Change Price ChangeDocument23 pagesOpen Interest Analysis: Trend Actio N Interpretatio N OI Change Price ChangeAkki vaidNo ratings yet

- Sample Quiz QuestionsDocument2 pagesSample Quiz QuestionsSuperGuyNo ratings yet

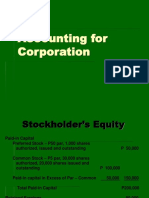

- Accounting For CorporationDocument11 pagesAccounting For CorporationMaricar D. VillarazaNo ratings yet

- Option Pricing Models - BinomialDocument10 pagesOption Pricing Models - BinomialSahinNo ratings yet

- Factors Affecting Stock MarketDocument80 pagesFactors Affecting Stock MarketAjay SanthNo ratings yet

- Bse Project Class 11Document22 pagesBse Project Class 11Suparn WadhiNo ratings yet

- Mid Test IB1708 SE161403 Nguyễn Trọng BằngDocument14 pagesMid Test IB1708 SE161403 Nguyễn Trọng BằngNguyen Trong Bang (K16HCM)No ratings yet

- Mark Minervini Quotes (@MinerviniQuote) - Twitter1Document1 pageMark Minervini Quotes (@MinerviniQuote) - Twitter1LNo ratings yet

- Finance Quiz 2Document4 pagesFinance Quiz 2studentNo ratings yet

- Class TestDocument8 pagesClass TestMayank kaushikNo ratings yet

- Salomon FRNDocument36 pagesSalomon FRNisas100% (1)

- Ruchi Soya Industries Limited: 15140MH1986PLC038536Document10 pagesRuchi Soya Industries Limited: 15140MH1986PLC038536Lalit SutharNo ratings yet

- Delta Neutral Vega LongDocument6 pagesDelta Neutral Vega LongPankajNo ratings yet

- Tugas Akm Ii Pertemuan 13Document5 pagesTugas Akm Ii Pertemuan 13Alisya UmariNo ratings yet

- 4 Valuation of SecuritiesDocument13 pages4 Valuation of SecuritiesPhạm Trần Thanh TúNo ratings yet

- A Study On InvestmentDocument4 pagesA Study On InvestmentSaloni GoyalNo ratings yet

- Mutual Funds: Project Report OnDocument40 pagesMutual Funds: Project Report OnShilpi_Mathur_7616No ratings yet