You might also like

- Utkarsh FinalDocument32 pagesUtkarsh FinalSunit ShandilyaNo ratings yet

- Case Study SCM at Wal-MartDocument4 pagesCase Study SCM at Wal-MartVarnika GuptaNo ratings yet

- ITCreport Accounts 2012Document215 pagesITCreport Accounts 2012sadafkhan21No ratings yet

- Project Report OnDocument55 pagesProject Report OnPratik Patel100% (1)

- Dabur SCMDocument36 pagesDabur SCMEkta Roy0% (1)

- Project On Parag MilkDocument26 pagesProject On Parag MilktechcaresystemNo ratings yet

- Adani WilmarkDocument78 pagesAdani WilmarkDeepak SinghalNo ratings yet

- Marico LTD.: ME Final Project PresentationDocument28 pagesMarico LTD.: ME Final Project PresentationSaumitra AmbegaokarNo ratings yet

- Assignment Topic: Risk Factors Involved in FMCG Sector / in Any Manufacturing UnitDocument13 pagesAssignment Topic: Risk Factors Involved in FMCG Sector / in Any Manufacturing UnitGaurav DeshwalNo ratings yet

- GUPTA - Export Import Management-MC GRAW HILL INDIA (2017)Document354 pagesGUPTA - Export Import Management-MC GRAW HILL INDIA (2017)rUTHNo ratings yet

- Behavioral Drivers of Brand Equity - Head and ShouldersDocument18 pagesBehavioral Drivers of Brand Equity - Head and ShouldersNihal GoudNo ratings yet

- VivaDocument29 pagesVivaA. ShanmugamNo ratings yet

- Advertising Strategy of AirtelDocument21 pagesAdvertising Strategy of AirtelChandu Thakur50% (2)

- Macro Economic Factors Affecting Pharma IndustryDocument2 pagesMacro Economic Factors Affecting Pharma IndustryDayaNo ratings yet

- Report On Sri Lanka CrisisDocument25 pagesReport On Sri Lanka CrisisRohit DoreNo ratings yet

- Marks & Spencer CaseDocument10 pagesMarks & Spencer CaseVanvisa KhunkrittiNo ratings yet

- Advanced Cost AccountingDocument2 pagesAdvanced Cost Accountingpooja sainiNo ratings yet

- WS-Demand Forecasting ScopeDocument24 pagesWS-Demand Forecasting ScopedhatchayaniramkumaNo ratings yet

- Micromax Case Study - Operations ManagementDocument7 pagesMicromax Case Study - Operations Managementkhem_singhNo ratings yet

- Arya Nandakumar - Week 4 Monday & Tuesday TaskDocument12 pagesArya Nandakumar - Week 4 Monday & Tuesday TaskJaya SuryaNo ratings yet

- The Raymond Limited: A Study: Director (Research) ICSI-CCGRT, Navi MumbaiDocument14 pagesThe Raymond Limited: A Study: Director (Research) ICSI-CCGRT, Navi Mumbaioptra ceraNo ratings yet

- International Business Notes MBA-III-Semster Osmania University - 248931546Document10 pagesInternational Business Notes MBA-III-Semster Osmania University - 248931546SujeetDhakal100% (1)

- PM Assignment 2 Bharti Walmart 31 39Document16 pagesPM Assignment 2 Bharti Walmart 31 39Ranjan MondalNo ratings yet

- Project On Parag MilkDocument74 pagesProject On Parag MilkraisNo ratings yet

- Presentasi Ethics GOMEDocument24 pagesPresentasi Ethics GOMERiandy Ar RasyidNo ratings yet

- Air Engine With DC Air CompressorDocument54 pagesAir Engine With DC Air CompressorvinothNo ratings yet

- Jilan ProjectDocument76 pagesJilan ProjectJai Ganesh100% (1)

- Dmba102 Business CommunicationDocument8 pagesDmba102 Business CommunicationShashi SainiNo ratings yet

- Amul PPTDocument25 pagesAmul PPTVivek VashisthaNo ratings yet

- Session-6 OutsourcingDocument54 pagesSession-6 OutsourcingMehulNo ratings yet

- The Impact of Working Capital Management On The Performance of Food and Beverages IndustryDocument6 pagesThe Impact of Working Capital Management On The Performance of Food and Beverages IndustrySaheed NureinNo ratings yet

- Parle ProjectDocument22 pagesParle Projectabhinav_mishra67121983% (6)

- Sales Promotional Activities by Air IndiaDocument15 pagesSales Promotional Activities by Air IndiaChandan Kumar SinghNo ratings yet

- Marico Industries: External Analysis Porter's Five Force ModelDocument3 pagesMarico Industries: External Analysis Porter's Five Force ModelAllan Edward GJ100% (2)

- Snapdeal Freecharge AcquisitionDocument10 pagesSnapdeal Freecharge AcquisitionAnkitha Kuriakose100% (1)

- Bombay DyeingDocument8 pagesBombay DyeingAnmol JainNo ratings yet

- A Case Study On Process Costing System of Uniliver (BD) Limited-Chap-1-13Document30 pagesA Case Study On Process Costing System of Uniliver (BD) Limited-Chap-1-13Jehan MahmudNo ratings yet

- Chapter 4 - Material ManagementDocument15 pagesChapter 4 - Material ManagementRohit BadgujarNo ratings yet

- Defensive StrategiesDocument6 pagesDefensive StrategieskarenNo ratings yet

- Strategic Management - I: Porter'S 5 Forces ModelDocument4 pagesStrategic Management - I: Porter'S 5 Forces Modelsanket vermaNo ratings yet

- Voltas Report V3Document18 pagesVoltas Report V3Puneet AgarwalNo ratings yet

- Management Accounting Project Group Number: C21 Group Members Name Roll No. Mobile No. E-Mail SectionDocument17 pagesManagement Accounting Project Group Number: C21 Group Members Name Roll No. Mobile No. E-Mail SectionSankalp MathurNo ratings yet

- A Study On Liquidity Analysis of Tekishub Consulting ServicesDocument14 pagesA Study On Liquidity Analysis of Tekishub Consulting ServicesTalla madhuri SreeNo ratings yet

- Allwyn Nissan Group 8Document58 pagesAllwyn Nissan Group 8Jayesh VasavaNo ratings yet

- Suger Factory 2Document111 pagesSuger Factory 2Manoj Balla100% (1)

- Project Report On The Genesis of Hindustan Unilever Limited (HUL)Document44 pagesProject Report On The Genesis of Hindustan Unilever Limited (HUL)swapnil panmandNo ratings yet

- Functions of RetailingDocument18 pagesFunctions of RetailingPredator Helios 300No ratings yet

- Case Study Wal Mart in India FinalDocument19 pagesCase Study Wal Mart in India FinalSara AhmedNo ratings yet

- Kothari Sugar Factory Internshipproject SamoleDocument52 pagesKothari Sugar Factory Internshipproject Samolenoobwarrior3No ratings yet

- Case StudyDocument6 pagesCase Studyvsangadi3585No ratings yet

- Godrej Builds 'Sampark' With Distributors - E-Business - Express Computer IndiaDocument2 pagesGodrej Builds 'Sampark' With Distributors - E-Business - Express Computer IndiaPradeep DubeyNo ratings yet

- SWOT Analysis of Shopper's StopDocument8 pagesSWOT Analysis of Shopper's Stopsubham kunduNo ratings yet

- Kanpur ConfectionariesDocument11 pagesKanpur Confectionariesarvind1289No ratings yet

- Consumer Satisfaction On Biscuit in Bangladesh MarketDocument18 pagesConsumer Satisfaction On Biscuit in Bangladesh MarketKaziTanvirAhmedNo ratings yet

- Alpha Electronics PresentationDocument17 pagesAlpha Electronics PresentationAnushree Khandalkar0% (1)

- Retail Vedu Management AssignmentDocument13 pagesRetail Vedu Management AssignmentakbarNo ratings yet

- Big Bazar Company AnalysisDocument65 pagesBig Bazar Company AnalysisGurbachan SinghNo ratings yet

- introduction:: Watches TitanDocument15 pagesintroduction:: Watches TitanThirumalesh MkNo ratings yet

- Competition Between The Rival CompaniesDocument14 pagesCompetition Between The Rival Companiessid3286No ratings yet

- Final ch3 and ch4Document31 pagesFinal ch3 and ch4abhi1504No ratings yet

- Project ReportDocument42 pagesProject Reportanoopmangal33% (6)

- New Text DocumentDocument1 pageNew Text Documentabhi1504No ratings yet

- Bharti Walmart JVDocument25 pagesBharti Walmart JVabhi1504No ratings yet

- View Employee Profile - JOBAIDDocument3 pagesView Employee Profile - JOBAIDabhi1504No ratings yet

- Sustainable Coffee Supply Chain Management: A Case Study in Buon Me Thuot City, Daklak, VietnamDocument17 pagesSustainable Coffee Supply Chain Management: A Case Study in Buon Me Thuot City, Daklak, VietnamThox SicNo ratings yet

- Long Gabby Word04 FarmersDocument1 pageLong Gabby Word04 Farmersapi-548580990No ratings yet

- CompanytrackerfxDocument54 pagesCompanytrackerfxFélix PujolsNo ratings yet

- Class 5 CMADocument50 pagesClass 5 CMAKanika RustagiNo ratings yet

- Epc For Bab Gas Compression Project (BGCP) Phase - Iii Comment Resolution Sheet (CRS)Document2 pagesEpc For Bab Gas Compression Project (BGCP) Phase - Iii Comment Resolution Sheet (CRS)raghav abudhabiNo ratings yet

- Bopp FilmsDocument4 pagesBopp FilmsHimanshuNo ratings yet

- UKBA Register of Sponsors Tiers 2 & 5 Sub Tiers OnlyDocument1,673 pagesUKBA Register of Sponsors Tiers 2 & 5 Sub Tiers Onlytomnext70No ratings yet

- DGFT Pulses October 2020Document87 pagesDGFT Pulses October 2020AvijitSinharoyNo ratings yet

- Au Unlimited Checkbook Challenge Module 03 Qa June 2021Document17 pagesAu Unlimited Checkbook Challenge Module 03 Qa June 2021aljim alparaqueNo ratings yet

- Eshet Eilon ProfileDocument3 pagesEshet Eilon ProfileLuan NguyenNo ratings yet

- Lower Fars Heavy Oil FieldDocument6 pagesLower Fars Heavy Oil Fieldsalman KhanNo ratings yet

- MRF ProjectDocument98 pagesMRF ProjectThigilpandi07 YTNo ratings yet

- For Posting 568-NGCP-PEC (ASPA) OVH 2020-037RC 10.29.2020.rspv - Arg-Clean Copy Final.11 (SGD)Document12 pagesFor Posting 568-NGCP-PEC (ASPA) OVH 2020-037RC 10.29.2020.rspv - Arg-Clean Copy Final.11 (SGD)sinnyen.hengNo ratings yet

- Module 1 Capacity Planning and Line BalancingDocument2 pagesModule 1 Capacity Planning and Line BalancingJohnathan LavaredsNo ratings yet

- Manufacturing Target ListDocument5 pagesManufacturing Target ListDevesh JhaNo ratings yet

- Bayview Beach Resort PenangDocument2 pagesBayview Beach Resort PenangVeraNo ratings yet

- Role of Support Institutions and Management of Small BusinessDocument12 pagesRole of Support Institutions and Management of Small Businessneha sharma0% (1)

- BkashDocument3 pagesBkashSajib DevNo ratings yet

- Nepal Agricultural Insurance - Country Experience FactsheetDocument2 pagesNepal Agricultural Insurance - Country Experience FactsheetSUMNo ratings yet

- RTO Payment Receipt - AnkitDocument1 pageRTO Payment Receipt - AnkitVishal SinghNo ratings yet

- Tata Motors LTD: Ayushi Deepti ShwetaDocument18 pagesTata Motors LTD: Ayushi Deepti ShwetaAyushi GuptaNo ratings yet

- Supply Chain Management Systems of Square Pharmaceuticals LTDDocument33 pagesSupply Chain Management Systems of Square Pharmaceuticals LTDAminul Islam 2016209690No ratings yet

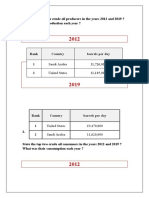

- State The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?Document6 pagesState The Top Two Crude Oil Producers in The Years 2012 and 2019 ? What Was Their Production Each Year ?laoy aolNo ratings yet

- Tijan Et AlDocument3 pagesTijan Et AlAnnisa AnandaNo ratings yet

- Educational Stories For Kids From Roma and Diana - YouTubeDocument1 pageEducational Stories For Kids From Roma and Diana - YouTubegdnqqbf99zNo ratings yet

- OPERATORI AERIENI ROMANI 07.11.2014 Rom-Eng PDFDocument26 pagesOPERATORI AERIENI ROMANI 07.11.2014 Rom-Eng PDFTraianBradNo ratings yet

- Solution Manual For Principles of Cost Accounting 17th Edition Vanderbeck Mitchell 1305087402 9781305087408Document36 pagesSolution Manual For Principles of Cost Accounting 17th Edition Vanderbeck Mitchell 1305087402 9781305087408thomasfraziermfbysxkzjn100% (27)

- Bill of Lading - Ageng Hana Prakoso - 195710009Document1 pageBill of Lading - Ageng Hana Prakoso - 195710009Ageng HanaNo ratings yet

- Agri-Food Commodity Chains and Globalising Networks 0754673367Document259 pagesAgri-Food Commodity Chains and Globalising Networks 0754673367ASHRUL TSANINo ratings yet

- Modern Banking Full NotesDocument49 pagesModern Banking Full NotesVishwa Lost userNo ratings yet