You might also like

- Case 2 - PG Japan The SK-II Globalization Project - SpreadsheetDocument7 pagesCase 2 - PG Japan The SK-II Globalization Project - SpreadsheetCAI DongningNo ratings yet

- IndexDocument50 pagesIndexensyngnNo ratings yet

- Chapter 2 Sample FileDocument40 pagesChapter 2 Sample Filemozammel80No ratings yet

- Poultry Brochure 3Document8 pagesPoultry Brochure 3Yasir MukhtarNo ratings yet

- Greenko Dutch B.V. Combined Statement of Profit and LossDocument2 pagesGreenko Dutch B.V. Combined Statement of Profit and LosshNo ratings yet

- Statistical Tables Hypostat 2020Document90 pagesStatistical Tables Hypostat 2020Ahmad Jawad HassaanNo ratings yet

- Pharma Case Excel File For StudentsDocument53 pagesPharma Case Excel File For StudentsJerodNo ratings yet

- IM - Cogent HRDocument14 pagesIM - Cogent HRAaron WilsonNo ratings yet

- PBOR Pension BenifitDocument9 pagesPBOR Pension Benifitशिवा यादव सोनूNo ratings yet

- United Food Pakistan Balance SheetDocument34 pagesUnited Food Pakistan Balance Sheettech& GamingNo ratings yet

- Wapic Smart LifeSavers PlanDocument8 pagesWapic Smart LifeSavers PlanSalifu AbdulNo ratings yet

- Income Statement: General Selling and Administration ExpensesDocument8 pagesIncome Statement: General Selling and Administration ExpensesShehzadi Mahum (F-Name :Sohail Ahmed)No ratings yet

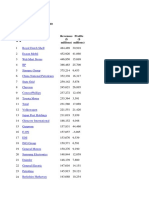

- 2010 List: Fortune Global 500Document28 pages2010 List: Fortune Global 500Tushar SawhneyNo ratings yet

- Rank 1: Wal-Mart Stores BP Exxon Mobil Royal Dutch/ Shell GroupDocument4 pagesRank 1: Wal-Mart Stores BP Exxon Mobil Royal Dutch/ Shell GroupibtiNo ratings yet

- 2022 Cause Death Report - Society of Actuaries Research Institute, LIMRA, RGA, and TAI.Document46 pages2022 Cause Death Report - Society of Actuaries Research Institute, LIMRA, RGA, and TAI.CFHeatherNo ratings yet

- Open Workshop - ISO 26000: In/Id - Yyyy-Mm-Dd Title / Titre - 1Document52 pagesOpen Workshop - ISO 26000: In/Id - Yyyy-Mm-Dd Title / Titre - 1김진우No ratings yet

- Risk Benefit Charges ExplainedDocument2 pagesRisk Benefit Charges ExplainedRaju JainNo ratings yet

- Single Premium Endowment Plan Licindiagov - inDocument5 pagesSingle Premium Endowment Plan Licindiagov - inSampiNo ratings yet

- Petrolera Zuata Petrozuata CA. AnswerDocument8 pagesPetrolera Zuata Petrozuata CA. AnswerKelvinItemuagbor100% (1)

- Exportadores Periodo 2012 1 2013 2 2014 3 2015 4 2016 5: Demanda en El MundoDocument6 pagesExportadores Periodo 2012 1 2013 2 2014 3 2015 4 2016 5: Demanda en El MundoJenryAvalosNo ratings yet

- 19.3 FMP 2Document38 pages19.3 FMP 2Javneet KaurNo ratings yet

- The Division Gear Attribute SheetDocument24 pagesThe Division Gear Attribute SheetbrunoNo ratings yet

- AM92 Mortality Table AnalysisDocument44 pagesAM92 Mortality Table AnalysisDeepanshu Sharma0% (2)

- Black Week VolksDocument2 pagesBlack Week VolksmaxwenneNo ratings yet

- Basic Mathematics - Pareto Chart - Data Sheet For Exercise 2Document5 pagesBasic Mathematics - Pareto Chart - Data Sheet For Exercise 2Ravi ParekhNo ratings yet

- Upr 2228669Document4 pagesUpr 2228669sammanihardware171No ratings yet

- Solloso Aida..global IssuesDocument9 pagesSolloso Aida..global IssuesMaria Reiena Gerodias BenigayNo ratings yet

- US Exports OverviewDocument22 pagesUS Exports OverviewRaza AliNo ratings yet

- Tablas DinamicasDocument3 pagesTablas DinamicasJuan ApzNo ratings yet

- The World Is Open For Your Business: An Overview of Exporting OpportunitiesDocument37 pagesThe World Is Open For Your Business: An Overview of Exporting OpportunitiesSajjad HussainNo ratings yet

- The World Is Open For Business. Yours.: An Overview of The U.S. Commercial ServiceDocument37 pagesThe World Is Open For Business. Yours.: An Overview of The U.S. Commercial ServiceSyaibatul HamdiNo ratings yet

- Personal InvestmentDocument93 pagesPersonal InvestmentPratham Poovaiah MalavandaNo ratings yet

- Benefits of Buying: Insurance PolicyDocument2 pagesBenefits of Buying: Insurance PolicyNo nameNo ratings yet

- BMP Bav ReportDocument79 pagesBMP Bav ReportThu ThuNo ratings yet

- BMP Bav Report FinalDocument93 pagesBMP Bav Report FinalThu ThuNo ratings yet

- Invest MaximiserDocument301 pagesInvest MaximiseradarshsinghNo ratings yet

- WrittenbyM11Document14 pagesWrittenbyM11btstudiozNo ratings yet

- JEL Classification Codes: KeywordsDocument14 pagesJEL Classification Codes: KeywordsRam VarneshNo ratings yet

- Country Per Capita Beef Consumption (KG) 124.8 101.1 118.6 90.4 Population Urbanization Rate Urban Population Per Capita GDPDocument4 pagesCountry Per Capita Beef Consumption (KG) 124.8 101.1 118.6 90.4 Population Urbanization Rate Urban Population Per Capita GDPferoz_bilalNo ratings yet

- Excel ProjectDocument1 pageExcel ProjectDanielle ReddyNo ratings yet

- Book 2Document2 pagesBook 2Bharathi 3280No ratings yet

- Takaful Companies - Overall: ItemsDocument6 pagesTakaful Companies - Overall: ItemsZubair ArshadNo ratings yet

- Aspire - Rate Cards - v3Document83 pagesAspire - Rate Cards - v3Ronak RanaNo ratings yet

- Prezentare AccorDocument93 pagesPrezentare AccorIoana MarinNo ratings yet

- Motores Vendidos 2014Document9 pagesMotores Vendidos 2014jesus romanNo ratings yet

- Covered Call: Profit/LossDocument9 pagesCovered Call: Profit/LossAqid Ahmed AnsariNo ratings yet

- Immigration by age and sex trends 1995-2021Document10 pagesImmigration by age and sex trends 1995-2021Georgescu RaduNo ratings yet

- HS50020_Economics of InsuranceDocument3 pagesHS50020_Economics of Insurancewigeh54591No ratings yet

- Appendices Financial RatiosDocument3 pagesAppendices Financial RatiosCristopherson PerezNo ratings yet

- General Motors Financial Statement AnalysisDocument8 pagesGeneral Motors Financial Statement AnalysisDenis MuneneNo ratings yet

- Calculos TotalDocument29 pagesCalculos TotalMaria De Los Angeles YomeyeNo ratings yet

- Top 20 Fortune Global 500 Companies by RevenueDocument19 pagesTop 20 Fortune Global 500 Companies by RevenueVikas RNo ratings yet

- FDI in FiguresDocument31 pagesFDI in FiguresraviNo ratings yet

- Bismar OqiDocument44 pagesBismar OqiedwincrzNo ratings yet

- Fundamental Analysis of 3 Major Indian Automobile PlayersDocument13 pagesFundamental Analysis of 3 Major Indian Automobile Playersvikas dhanukaNo ratings yet

- Consulting Math DrillsDocument15 pagesConsulting Math DrillsHashaam Javed50% (2)

- MSIDritBikes PDFDocument20 pagesMSIDritBikes PDFShaowen LiuNo ratings yet

- IFFCO-Tokio Critical Illness Benefit Policy Sales LiteratureDocument4 pagesIFFCO-Tokio Critical Illness Benefit Policy Sales LiteratureMagix MoviesNo ratings yet

- BÀI TẬP KDQTDocument3 pagesBÀI TẬP KDQTnam HoàngNo ratings yet

- Managing change at UPSDocument18 pagesManaging change at UPSNeha Vyas100% (2)

- MPS Project Report on Entrepreneurial ActivityDocument4 pagesMPS Project Report on Entrepreneurial ActivityNeha VyasNo ratings yet

- Karan PPT NewDocument19 pagesKaran PPT NewNeha VyasNo ratings yet

- Hanuman MGTDocument1 pageHanuman MGTNeha VyasNo ratings yet

- Lecture 2 The Australian Health System Health Systems and Economics PUBH5752Document10 pagesLecture 2 The Australian Health System Health Systems and Economics PUBH5752Mia MacMillanNo ratings yet

- 1 The Health and Safety at Work Act 1974Document2 pages1 The Health and Safety at Work Act 1974nicolaeNo ratings yet

- Ao 1001 PDSDocument1 pageAo 1001 PDSben7251No ratings yet

- Slovak SPectator 1703Document16 pagesSlovak SPectator 1703The Slovak SpectatorNo ratings yet

- Glidden Man Accused of OWI 1st OffenseDocument2 pagesGlidden Man Accused of OWI 1st OffensethesacnewsNo ratings yet

- ICE Affirmative and Negative - Michigan7 2015Document345 pagesICE Affirmative and Negative - Michigan7 2015Davis HillNo ratings yet

- Inditex Annual Report 2015 WebDocument318 pagesInditex Annual Report 2015 WebAmrit KaurNo ratings yet

- Essentials of Good GovernanceDocument2 pagesEssentials of Good Governancedeepali02No ratings yet

- Clinical Data Quality ProcedureDocument17 pagesClinical Data Quality Procedurejhonron100% (1)

- North Shore LTP 2009to2024Document509 pagesNorth Shore LTP 2009to2024George WoodNo ratings yet

- USDA Animal Welfare Inspection Guide PDFDocument336 pagesUSDA Animal Welfare Inspection Guide PDFseanNo ratings yet

- R.A. 9275 - Philippine Clean Water Act of 2004Document19 pagesR.A. 9275 - Philippine Clean Water Act of 2004Ma Jhunelle A. BaduaNo ratings yet

- CITY GOV'T OF VALENZUELA CITIZEN'S CHARTER 2019Document582 pagesCITY GOV'T OF VALENZUELA CITIZEN'S CHARTER 2019Kaye Reyes-RoldanNo ratings yet

- Session 6 Meaning and Nature of RiskDocument20 pagesSession 6 Meaning and Nature of RiskPranit ShahNo ratings yet

- Managing Health For Field Operations in Oil and Gas ActivitiesDocument44 pagesManaging Health For Field Operations in Oil and Gas ActivitiesHaleemUrRashidBangashNo ratings yet

- Index 2Document2 pagesIndex 2yuffy011No ratings yet

- Bier Vs BierDocument1 pageBier Vs BierwesleybooksNo ratings yet

- Security Guard CV TemplateDocument3 pagesSecurity Guard CV TemplateArchana Singh100% (1)

- Certificate of Insurance: Patriot America PlusDocument24 pagesCertificate of Insurance: Patriot America PlusKARTHIK145No ratings yet

- DGMS Annul Report, 2008 PDFDocument151 pagesDGMS Annul Report, 2008 PDFKandagatla ManoharNo ratings yet

- Introduction to Healthcare Ethics TheoriesDocument4 pagesIntroduction to Healthcare Ethics TheoriesdirkdarrenNo ratings yet

- Final 2017 BLM Burning Man Event AARDocument28 pagesFinal 2017 BLM Burning Man Event AARReno Gazette JournalNo ratings yet

- Baku Youth Forum Summer School ApplicationDocument4 pagesBaku Youth Forum Summer School ApplicationAdyuta BanuNo ratings yet

- MSP Recovery, LLC V Allstate Insurance CompanyDocument18 pagesMSP Recovery, LLC V Allstate Insurance CompanySamuel RichardsonNo ratings yet

- Oddfellows HistoryDocument10 pagesOddfellows HistoryFuzzy_Wood_Person100% (1)

- Understanding Risk Bat Coronavirus Emergence Grant NoticeDocument528 pagesUnderstanding Risk Bat Coronavirus Emergence Grant NoticeNew York Post100% (6)

- Executive Order No. 385, 1996Document3 pagesExecutive Order No. 385, 1996VERA FilesNo ratings yet

- Mulekwa Curriculum VitaeDocument3 pagesMulekwa Curriculum VitaemulesabaNo ratings yet

- NSTP Module 5 1Document2 pagesNSTP Module 5 1Eden Faith Aggalao100% (1)

- Patients Autonomy and Informed ConsentDocument10 pagesPatients Autonomy and Informed ConsentSandra GabasNo ratings yet