You might also like

- Account DeterminationDocument13 pagesAccount DeterminationVenkat KumarNo ratings yet

- IS Audit Checklist Bank SystemsDocument37 pagesIS Audit Checklist Bank SystemsAkash AgarwalNo ratings yet

- Tax Planning For Setting New BusinessDocument6 pagesTax Planning For Setting New BusinessHardipsinh Yadav56% (9)

- Advertising and Promotion - An Integrated Marketing Communications Perspective (10 - E) - Chapter 1 - George E. Belch, Michael A. Belch - 1081393Document24 pagesAdvertising and Promotion - An Integrated Marketing Communications Perspective (10 - E) - Chapter 1 - George E. Belch, Michael A. Belch - 1081393Nhu QuynhNo ratings yet

- Report on India's Ceramic Tiles IndustryDocument34 pagesReport on India's Ceramic Tiles Industryshahid_cute18No ratings yet

- Central Excise Administration and ReturnsDocument22 pagesCentral Excise Administration and ReturnsSubhasish ChatterjeeNo ratings yet

- Excise DutyDocument4 pagesExcise DutyDigvijay LakdeNo ratings yet

- DR - MGR E & RI - Chennai - 28.05.2021-1Document21 pagesDR - MGR E & RI - Chennai - 28.05.2021-1Sha dowNo ratings yet

- GST Unit VDocument29 pagesGST Unit VMani Maran123No ratings yet

- Record Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Document16 pagesRecord Notebook Faculty of Arts & Commerce Department of Cost & Management Accounting (Cma)Sha dowNo ratings yet

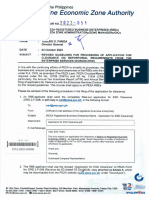

- WHAT YOU SHOULD KNOW ABOUT PEZAs REPORTORIAL REQUIREMENTSDocument5 pagesWHAT YOU SHOULD KNOW ABOUT PEZAs REPORTORIAL REQUIREMENTSPatrickNo ratings yet

- Composition Levy: Presentation By: Vishal Somai Sr. Faculty of Direct & Indirect TaxDocument19 pagesComposition Levy: Presentation By: Vishal Somai Sr. Faculty of Direct & Indirect TaxTRANSFORMERS PRIMENo ratings yet

- Eturns: This Chapter Will Equip You ToDocument52 pagesEturns: This Chapter Will Equip You ToShowkat MalikNo ratings yet

- Indirect Tax - Budget 2019Document43 pagesIndirect Tax - Budget 2019Brijesh PitrodaNo ratings yet

- Returns: FAQ'sDocument25 pagesReturns: FAQ'smun1barejaNo ratings yet

- Taxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTDocument5 pagesTaxguru - In-Section 10 CGST Act 2017 Composition Levy Under GSTTheEnigmatic AccountantNo ratings yet

- (Updated July 2010) (2.2.1) Corporation Tax - General BackgroundDocument13 pages(Updated July 2010) (2.2.1) Corporation Tax - General BackgroundjfjkavanaghNo ratings yet

- Small Scale Exemption SchemeDocument8 pagesSmall Scale Exemption SchemebakulhariaNo ratings yet

- Faqs On New GST Retu Rns FormsDocument14 pagesFaqs On New GST Retu Rns FormsFizo KjNo ratings yet

- Indirect Tax AmendmentsDocument46 pagesIndirect Tax AmendmentsCeciro LodhamNo ratings yet

- Eturns: After Studying This Chapter, You Will Be Able ToDocument70 pagesEturns: After Studying This Chapter, You Will Be Able ToChandan ganapathi HcNo ratings yet

- BDO Budget Snapshot - 2012-13Document9 pagesBDO Budget Snapshot - 2012-13Pulluri Ravikumar YugandarNo ratings yet

- x220 Lenovo LaptopsDocument20 pagesx220 Lenovo LaptopsEmmanuel MoyoNo ratings yet

- Finance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiDocument43 pagesFinance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New Delhipuritansoul100% (2)

- Annual Return - Salem BranchDocument23 pagesAnnual Return - Salem BranchSureshkumarNo ratings yet

- Statement Outwrad SupplyDocument4 pagesStatement Outwrad SupplyTushar GoelNo ratings yet

- Overview of Key Amendments to the Philippine Tax Code under the TRAIN LawDocument28 pagesOverview of Key Amendments to the Philippine Tax Code under the TRAIN LawScarlette CooperaNo ratings yet

- Finance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiDocument43 pagesFinance Bill 2009 - Direct Tax Proposals: Presentation By: CA. Kapil Goel, ACA, LLB Chartered Accountant New DelhiPrasad KadamNo ratings yet

- Unit 2 - Part III - Returns Under GST - 30!07!2021Document4 pagesUnit 2 - Part III - Returns Under GST - 30!07!2021Milan ChandaranaNo ratings yet

- Mc2023051 (Application for ESD Clearance)Document7 pagesMc2023051 (Application for ESD Clearance)jgagarinNo ratings yet

- PEZA Reportorial RequirementsDocument25 pagesPEZA Reportorial RequirementsDarioNo ratings yet

- Tax AmnestyDocument38 pagesTax AmnestyElsha dela penaNo ratings yet

- Return ChapterDocument8 pagesReturn ChapterShubham KuberkarNo ratings yet

- GST Returns and ComplianceDocument11 pagesGST Returns and ComplianceJay PawarNo ratings yet

- LDCE Notes/Notes For LDCE-LGS/12Document12 pagesLDCE Notes/Notes For LDCE-LGS/12R Sathish KumarNo ratings yet

- Chapter 12 - Returns - NotesDocument15 pagesChapter 12 - Returns - NotesPuran GuptaNo ratings yet

- Exemption From Customs DutyDocument4 pagesExemption From Customs DutyRavikumar PaNo ratings yet

- GST - GOODS & Service Tax What Is GSTDocument4 pagesGST - GOODS & Service Tax What Is GSTsubbiah kailasamNo ratings yet

- Cenvat Credit in Easy StepsDocument7 pagesCenvat Credit in Easy StepsNiravMakwanaNo ratings yet

- Composition SchemeDocument12 pagesComposition Scheme311903736No ratings yet

- GST-603 Unit 5Document3 pagesGST-603 Unit 5GauharNo ratings yet

- Amendments to the Tax Code under TRAIN LawDocument23 pagesAmendments to the Tax Code under TRAIN LawCha GalangNo ratings yet

- Recent Developments in GSTDocument27 pagesRecent Developments in GSTAravindNo ratings yet

- GSTR 9 and 9CDocument4 pagesGSTR 9 and 9Cnitin01.snetNo ratings yet

- E2 E3 Financee2 E3 If Capital Goods On Which Cenvat Credit Has Been TakenDocument32 pagesE2 E3 Financee2 E3 If Capital Goods On Which Cenvat Credit Has Been Takenpintu_dyNo ratings yet

- Certificates Forming Part of CRS March 2018Document48 pagesCertificates Forming Part of CRS March 2018Venkat UppalapatiNo ratings yet

- Returns GSTDocument25 pagesReturns GSTRahul RockzzNo ratings yet

- Chapter 5 Composition Scheme Nov 2020Document41 pagesChapter 5 Composition Scheme Nov 2020Alka GuptaNo ratings yet

- Presentation (2) (1) - 1Document12 pagesPresentation (2) (1) - 1drawback979No ratings yet

- Chapter 8 Composition Scheme Under GSTDocument12 pagesChapter 8 Composition Scheme Under GSTDR. PREETI JINDALNo ratings yet

- GST Council 43rd Meeting Key RecommendationsDocument6 pagesGST Council 43rd Meeting Key Recommendationssuhani singhNo ratings yet

- Understanding On: Tax Audit U/s 44AB of I.T. ActDocument29 pagesUnderstanding On: Tax Audit U/s 44AB of I.T. Actspchheda4996No ratings yet

- PEZA REPORTORIAL REQUIREMENTS As of Feb 2023Document2 pagesPEZA REPORTORIAL REQUIREMENTS As of Feb 2023MarkNo ratings yet

- IDT AmendementsDocument20 pagesIDT AmendementstharunhimNo ratings yet

- GST Annual Return TypesDocument24 pagesGST Annual Return TypesPushpraj SinghNo ratings yet

- 74824bos60500 cp15Document90 pages74824bos60500 cp15soni12c2004No ratings yet

- Composition SchemeDocument4 pagesComposition Schemecloudstorage567No ratings yet

- All About GST Annual ReturnsDocument9 pagesAll About GST Annual ReturnsinfoNo ratings yet

- Step by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?Document7 pagesStep by Step Compliances Under RCM: How Composition Dealer Will Be Affected by RCM?arpit jainNo ratings yet

- CA CS CMA Final Statutory Updates For Nov Dec 2020Document43 pagesCA CS CMA Final Statutory Updates For Nov Dec 2020Anu GraphicsNo ratings yet

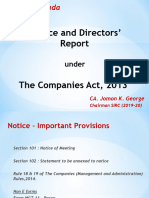

- Notice & DRDocument25 pagesNotice & DRvermasanjay69No ratings yet

- GST Annual Return Filing DeadlineDocument61 pagesGST Annual Return Filing DeadlineRishav AnandNo ratings yet

- Project ReportDocument58 pagesProject ReportAkash Agarwal100% (1)

- Secretarial Checklist under Companies Act 1956Document6 pagesSecretarial Checklist under Companies Act 1956Akash AgarwalNo ratings yet

- GST MigrationDocument1 pageGST MigrationAkash AgarwalNo ratings yet

- Value Added Tax in TallyDocument14 pagesValue Added Tax in TallyAkash AgarwalNo ratings yet

- Bank Audit FinalDocument4 pagesBank Audit FinalAkash AgarwalNo ratings yet

- Summary of Capital Gains For Final CA - 11 PagesDocument12 pagesSummary of Capital Gains For Final CA - 11 PagesKumar GauravNo ratings yet

- Bank Audit FinalDocument4 pagesBank Audit FinalAkash AgarwalNo ratings yet

- CONCURRENT AUDIT CHECKLISTDocument15 pagesCONCURRENT AUDIT CHECKLISTNaveen KondabathulaNo ratings yet

- Rbi To Control NpaDocument11 pagesRbi To Control NpaSneha HanumanthappaNo ratings yet

- Summary of Capital Gains For Final CA - 11 PagesDocument12 pagesSummary of Capital Gains For Final CA - 11 PagesKumar GauravNo ratings yet

- Law On Taxability of Gifts A Comprehensive AnalysisDocument24 pagesLaw On Taxability of Gifts A Comprehensive AnalysisAkash AgarwalNo ratings yet

- CONCURRENT AUDIT CHECKLISTDocument15 pagesCONCURRENT AUDIT CHECKLISTNaveen KondabathulaNo ratings yet

- Assessment ProcedureDocument7 pagesAssessment Procedurebabajan_4No ratings yet

- CONCURRENT AUDIT SCOPEDocument15 pagesCONCURRENT AUDIT SCOPEcaonkarsinghNo ratings yet

- Prudential Norms On Income Recognition, Asset Classification and Provisioning Pertaining To AdvancesDocument52 pagesPrudential Norms On Income Recognition, Asset Classification and Provisioning Pertaining To AdvancesArya NaveenNo ratings yet

- Concurrent AuditDocument15 pagesConcurrent AuditAkash Agarwal100% (2)

- Forex AuditDocument25 pagesForex AuditAkash AgarwalNo ratings yet

- Bank Branch Audit ManualDocument55 pagesBank Branch Audit ManualAkash AgarwalNo ratings yet

- 20 ListofLoanQueries 1Document10 pages20 ListofLoanQueries 1Akash AgarwalNo ratings yet

- Reserve Bank of IndiaDocument32 pagesReserve Bank of IndiaAkash AgarwalNo ratings yet

- KV XII ACC Question Bank of MCQ - Reason Based - Case Study Based Questions Rajan KapoorDocument151 pagesKV XII ACC Question Bank of MCQ - Reason Based - Case Study Based Questions Rajan KapoorMrityunjay KumarNo ratings yet

- Int B Assignment2 TIN PDFDocument12 pagesInt B Assignment2 TIN PDFJohn F CannadyNo ratings yet

- FH3 - Learner Guide - Module 1Document249 pagesFH3 - Learner Guide - Module 1ZwelizweleereevereNo ratings yet

- Market Positioning Strategies MKTDocument2 pagesMarket Positioning Strategies MKTrabiatulNo ratings yet

- Manage GoFin's Accounting Team & Financial ReportingDocument2 pagesManage GoFin's Accounting Team & Financial Reportingsitepu1223No ratings yet

- PM Process Groups, Phases & PMOsDocument30 pagesPM Process Groups, Phases & PMOsHaisham AliNo ratings yet

- Iwokazpy Fo - QR Forj.K Fuxe Fyfevsm: Purvanchal Vidyut Vitaran Nigam LTDDocument2 pagesIwokazpy Fo - QR Forj.K Fuxe Fyfevsm: Purvanchal Vidyut Vitaran Nigam LTDAvinash palNo ratings yet

- Ruhnke 2014Document31 pagesRuhnke 2014علي الماغوطNo ratings yet

- Practical Questions With HintsDocument4 pagesPractical Questions With HintsMff DeadsparkNo ratings yet

- CLASS 11 Accountancy NotesDocument11 pagesCLASS 11 Accountancy NotesVikram KumarNo ratings yet

- The Marketing Function's Main RolesDocument11 pagesThe Marketing Function's Main RolesNga Nga NguyenNo ratings yet

- The Examiner's Answers F2 - Financial Management September 2012Document16 pagesThe Examiner's Answers F2 - Financial Management September 2012FahadNo ratings yet

- Fairness Accountability Transparency and StewardsDocument19 pagesFairness Accountability Transparency and StewardsAngel Joy FulledoNo ratings yet

- Corperate StrategyDocument3 pagesCorperate StrategySaba AsimNo ratings yet

- Impact of Social Media On Our LivesDocument53 pagesImpact of Social Media On Our LivesFatima TahirNo ratings yet

- Tessitura Monti India-R-28032018Document7 pagesTessitura Monti India-R-28032018Pradeep AhireNo ratings yet

- Transportation SCMDocument34 pagesTransportation SCMsharathNo ratings yet

- Wellness Massage: Module 2: Development and MarketDocument19 pagesWellness Massage: Module 2: Development and MarketJicille BiayNo ratings yet

- FSAI EXAM2 Solutions Fraser 10thDocument14 pagesFSAI EXAM2 Solutions Fraser 10thGlaiza Dalayoan Flores0% (1)

- Paper On GSTDocument5 pagesPaper On GSTOlivia EmersonNo ratings yet

- Kumar Saurav: Course Name Name of The Institute Board/University Year of Passing CGPA/PercentageDocument2 pagesKumar Saurav: Course Name Name of The Institute Board/University Year of Passing CGPA/PercentagesunilkumarchaudharyNo ratings yet

- HR 2Document13 pagesHR 2Akhil Ranjan TarafderNo ratings yet

- Enl Integrated Report 2019 PDFDocument105 pagesEnl Integrated Report 2019 PDFHEMKESH CONHYENo ratings yet

- Resume BS Electrical EngineeringDocument1 pageResume BS Electrical EngineeringJUAN EUSEBIONo ratings yet

- QUESTIONNAIREDocument3 pagesQUESTIONNAIREtrang phạmNo ratings yet

- Financial Management:: Risk Analysis and Project EvaluationDocument79 pagesFinancial Management:: Risk Analysis and Project EvaluationSarah SaluquenNo ratings yet

- Week 5 - Listening 1 FDocument2 pagesWeek 5 - Listening 1 FRafael FletesNo ratings yet