You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Dhiraj Airtel Research PlanDocument9 pagesDhiraj Airtel Research Planankit_tripathi_8No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Fiscal Policy in IndiaDocument10 pagesFiscal Policy in Indiaankit_tripathi_8No ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Conditions & Warren TiesDocument3 pagesConditions & Warren Tiesankit_tripathi_8No ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Effective Presentation SkillsDocument17 pagesEffective Presentation Skillsankit_tripathi_8No ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Calendars: Ankit Tripathi Kinnar Majithia Pradnya BoraDocument8 pagesCalendars: Ankit Tripathi Kinnar Majithia Pradnya Boraankit_tripathi_8No ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Poverty Eradication in PakistanDocument4 pagesPoverty Eradication in PakistanBilal KhalidNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Benson Enterprises Is Evaluating Alternative Uses For A Three Story ManufacturingDocument1 pageBenson Enterprises Is Evaluating Alternative Uses For A Three Story ManufacturingAmit PandeyNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- GJEPC FinalDocument21 pagesGJEPC FinalVishal RamrakhyaniNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- DisinvestmentDocument20 pagesDisinvestmentSai RameshNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Fill in The Blanks To Make The Following Statements Correct ADocument1 pageFill in The Blanks To Make The Following Statements Correct Atrilocksp SinghNo ratings yet

- JPMorgan Chase Partners With InvestCloud For Digital Wealth ManagementDocument1 pageJPMorgan Chase Partners With InvestCloud For Digital Wealth ManagementInvest CloudNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Unemployment Case StudyDocument2 pagesUnemployment Case StudyJamesNo ratings yet

- Ingles SenaDocument6 pagesIngles Senaginna ibarraNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2023 Asia Partners Internet ReportDocument332 pages2023 Asia Partners Internet ReportBen SetoNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- International Trade at A Casual Environment Exercise & Script - Listening ComprehensionDocument2 pagesInternational Trade at A Casual Environment Exercise & Script - Listening ComprehensionFrancisco J. Salinas B.No ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Banking Diploma, 79thDocument1 pageBanking Diploma, 79thbrikkhoNo ratings yet

- Shipping Sector of PakistanDocument12 pagesShipping Sector of PakistanZain BhikaNo ratings yet

- 3 The Balance of Payments: Chapter ObjectivesDocument12 pages3 The Balance of Payments: Chapter ObjectivesJayant312002 ChhabraNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Study On E-Commerce in India & Madhya Pradesh As A StateDocument4 pagesStudy On E-Commerce in India & Madhya Pradesh As A StateishanhbmehtaNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Payslip For The Month of June 2022: Kotak Mahindra Bank LTDDocument1 pagePayslip For The Month of June 2022: Kotak Mahindra Bank LTDshubham choure100% (1)

- India's Trade With GCC in The Age of Covid 19Document9 pagesIndia's Trade With GCC in The Age of Covid 19Editor IJTSRD100% (1)

- Answer 4 Early Life of Bhutto: Bhutto Undertook Large Scale Nationalization of Industry, Insurance and BankingDocument3 pagesAnswer 4 Early Life of Bhutto: Bhutto Undertook Large Scale Nationalization of Industry, Insurance and BankingSaniya sohailNo ratings yet

- PWD Budget 2019 - bp18Document76 pagesPWD Budget 2019 - bp18amitNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Grindly Gases Petrochemicals PVT LTD - 270 - 11!09!2021Document2 pagesGrindly Gases Petrochemicals PVT LTD - 270 - 11!09!2021Pragnesh PrajapatiNo ratings yet

- Inglés Jun 2017 PDFDocument2 pagesInglés Jun 2017 PDFbpxamz0% (1)

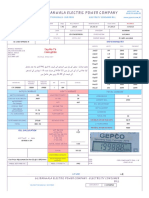

- Gepco Online BillDocument2 pagesGepco Online BillMehr UmairNo ratings yet

- 12 Pol Science Ncert CH 9Document5 pages12 Pol Science Ncert CH 9Mohit AntilNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Philippine National Bank History and FunctionsDocument10 pagesThe Philippine National Bank History and FunctionsJared Andre CarreonNo ratings yet

- INTERNATIONAL MARKETING MANAGEMENT MilleDocument9 pagesINTERNATIONAL MARKETING MANAGEMENT MilleLamillaNo ratings yet

- Debt Sustainability in The CaribbeanDocument15 pagesDebt Sustainability in The CaribbeanMaxens ANo ratings yet

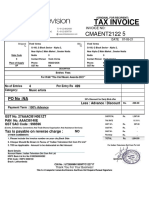

- Add: CGST Add: SGST Total Tax Amount: Total Amount Including Tax: Total Amount Excluding TaxDocument2 pagesAdd: CGST Add: SGST Total Tax Amount: Total Amount Including Tax: Total Amount Excluding TaxHajrabi ShaikhNo ratings yet

- Strategic Business Analysis Co9 Case Study Final: Norway'S Pension GlobalDocument2 pagesStrategic Business Analysis Co9 Case Study Final: Norway'S Pension GlobalShirley Ann ValenciaNo ratings yet

- 05 Vivek VermaDocument1 page05 Vivek VermaVivek VermaNo ratings yet

- Policy and Economic Reforms in IndiaDocument16 pagesPolicy and Economic Reforms in IndiaAshish kumar NairNo ratings yet

- Gahum Barangay-ProfileDocument2 pagesGahum Barangay-ProfileEmayvelleNo ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)