You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- MT103 522286795pdfDocument3 pagesMT103 522286795pdfMasoud Dastgerdi100% (4)

- Pre-Colonial AfricaDocument75 pagesPre-Colonial AfricaSean JoshuaNo ratings yet

- Profit From The PanicDocument202 pagesProfit From The PanicLau Wai KentNo ratings yet

- FormulaDocument10 pagesFormulaAngel Alejo Acoba100% (1)

- OpTransactionHistoryUX522 02 2024Document7 pagesOpTransactionHistoryUX522 02 2024piyush882676No ratings yet

- Sha611 Description Hungerford CaseDocument2 pagesSha611 Description Hungerford Casenhật minh phạm trầnNo ratings yet

- Fund Transfer Request - Combined Form: RTGS/NEFT/DD Issuance/RBL Account To Account Transfer (ATAT)Document1 pageFund Transfer Request - Combined Form: RTGS/NEFT/DD Issuance/RBL Account To Account Transfer (ATAT)shri halaNo ratings yet

- Trading and Profit and Loss Account Format: DR CRDocument14 pagesTrading and Profit and Loss Account Format: DR CRHarshini AkilandanNo ratings yet

- Difference Between Coupon and Yield To MaturityDocument2 pagesDifference Between Coupon and Yield To MaturitySACHINNo ratings yet

- Yen To Trade Full Curriculum UnitDocument148 pagesYen To Trade Full Curriculum UnitAlbert Kirby TardeoNo ratings yet

- Understanding Derivatives Chapter 2 Central Counterparty Clearing PDFDocument15 pagesUnderstanding Derivatives Chapter 2 Central Counterparty Clearing PDFOsas ImianvanNo ratings yet

- Visualizing Money PDFDocument22 pagesVisualizing Money PDFmalditongguy100% (1)

- Record Point of Sale (POS) Transaction in TallyPrimeDocument6 pagesRecord Point of Sale (POS) Transaction in TallyPrimeSubham DuttaNo ratings yet

- Goldline Defence Towers 04-Aug-23Document11 pagesGoldline Defence Towers 04-Aug-23Faizan KarsazNo ratings yet

- An Overview of Money Laundering Causes, Methods and EffectsDocument46 pagesAn Overview of Money Laundering Causes, Methods and EffectsMunir Ahmed KakarNo ratings yet

- A What Specific Recommendations Would You Give The Johnsons ForDocument1 pageA What Specific Recommendations Would You Give The Johnsons ForAmit PandeyNo ratings yet

- Inflation in 2022Document2 pagesInflation in 2022Lea Moureen KaibiganNo ratings yet

- Sample Illustration Financial StatementDocument3 pagesSample Illustration Financial StatementJuvy Jane DuarteNo ratings yet

- HDFC SecuritiesDocument85 pagesHDFC Securitiessuncancerian100% (1)

- Who Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)Document294 pagesWho Moved My Interest Rate - Leading The Reserve Bank of India Through Five Turbulent Years (PDFDrive)dev guptaNo ratings yet

- Boopathi Citibank Savings Account Statement-01August2019-31October2019Document10 pagesBoopathi Citibank Savings Account Statement-01August2019-31October2019VandanaNo ratings yet

- Windham Capital Multi Asset Income StrategiesDocument2 pagesWindham Capital Multi Asset Income StrategiesdimtharsNo ratings yet

- Option Markets & ContractsDocument46 pagesOption Markets & Contractsroshanidharma100% (1)

- Statement Summary: Statement Period Account NumberDocument5 pagesStatement Summary: Statement Period Account NumberSharon JonesNo ratings yet

- Activity 3Document2 pagesActivity 3Lea Yvette SaladinoNo ratings yet

- Sad - Text - en - Xls - r1Document17 pagesSad - Text - en - Xls - r1Samuel SantanaNo ratings yet

- Portfolio ManagmentDocument30 pagesPortfolio ManagmentMitali AmagdavNo ratings yet

- STMT 19680100009011 1673186518787Document11 pagesSTMT 19680100009011 1673186518787prabha sureshNo ratings yet

- SESSION14Document10 pagesSESSION14RADHIKA RASTOGINo ratings yet

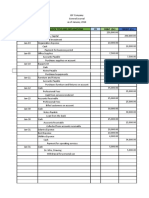

- JGF Company General Journal 2014Document5 pagesJGF Company General Journal 2014TJ JT100% (1)