You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

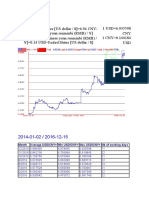

- Month Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysDocument3 pagesMonth Average USD/CNY Min USD/CNY Max USD/CNY NB of Working DaysZahid RizvyNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Cambridge International Advanced Subsidiary and Advanced LevelDocument8 pagesCambridge International Advanced Subsidiary and Advanced LevelNguyễn QuânNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Jose C. Guico For Petitioner. Wilfredo Cortez For Private RespondentsDocument5 pagesJose C. Guico For Petitioner. Wilfredo Cortez For Private Respondentsmichelle m. templadoNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Project CharterDocument8 pagesProject CharterVicky MandalNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 9th CAMC - FIDFDocument7 pages9th CAMC - FIDFSankarMohanNo ratings yet

- FOR Office USE Only: HDFC Life Sb/Ca/Cc/Sb-Nre/Sb-Nro/OtherDocument2 pagesFOR Office USE Only: HDFC Life Sb/Ca/Cc/Sb-Nre/Sb-Nro/OtherVIkashNo ratings yet

- University of Mumbai Project On Investment Banking Bachelor of CommerceDocument6 pagesUniversity of Mumbai Project On Investment Banking Bachelor of CommerceParag MoreNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Chicago 'Buycks' Lawsuit PlaintiffsDocument6 pagesChicago 'Buycks' Lawsuit PlaintiffsThe Daily CallerNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Bookmakers NightmareDocument50 pagesBookmakers NightmarefabihdroNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- AILET Last 5 Year Question Papers Answer Key 2019 2023Document196 pagesAILET Last 5 Year Question Papers Answer Key 2019 2023Pranav SinghNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Wec12 01 Que 20240120Document32 pagesWec12 01 Que 20240120Hatim RampurwalaNo ratings yet

- Team Energy Corporation, V. Cir G.R. No. 197770, March 14, 2018 Cir V. Covanta Energy Philippine Holdings, Inc., G.R. No. 203160, January 24, 2018Document5 pagesTeam Energy Corporation, V. Cir G.R. No. 197770, March 14, 2018 Cir V. Covanta Energy Philippine Holdings, Inc., G.R. No. 203160, January 24, 2018Raymarc Elizer AsuncionNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- TerraCycle Investment GuideDocument21 pagesTerraCycle Investment GuideMaria KennedyNo ratings yet

- Laboratory Rules and SafetyDocument2 pagesLaboratory Rules and SafetySamantha Tachtenberg100% (1)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Q3 Las WK 2 - Applied EconomicsDocument10 pagesQ3 Las WK 2 - Applied Economicsmichelle ann luzon100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- 2.01 Economic SystemsDocument16 pages2.01 Economic SystemsRessie Joy Catherine FelicesNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 13 Chapter V (Swot Analysis and Compitetor Analysis)Document3 pages13 Chapter V (Swot Analysis and Compitetor Analysis)hari tejaNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Managerial Economics Tutorial-1 SolutionsDocument11 pagesManagerial Economics Tutorial-1 Solutionsaritra mondalNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- List of Industries PackingDocument6 pagesList of Industries PackingRavichandran SNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- 2.3 Movie Time: Antonia TasconDocument2 pages2.3 Movie Time: Antonia TasconAntonia Tascon Z.100% (1)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- IELTS Writing Task 1 Sample - Bar Chart - ZIMDocument28 pagesIELTS Writing Task 1 Sample - Bar Chart - ZIMPhương Thư Nguyễn HoàngNo ratings yet

- Itinerario Cosco ShippingDocument2 pagesItinerario Cosco ShippingRelly CarrascoNo ratings yet

- Delegation of Powers As Per DPE GuidelinesDocument23 pagesDelegation of Powers As Per DPE GuidelinesVIJAYAKUMARMPLNo ratings yet

- Superstocks Final Advance Reviewer'sDocument250 pagesSuperstocks Final Advance Reviewer'sbanman8796% (24)

- Reliability Evaluation of Grid-Connected Photovoltaic Power SystemsDocument32 pagesReliability Evaluation of Grid-Connected Photovoltaic Power Systemssamsai88850% (2)

- Advantages and Disadvantages of Shares and DebentureDocument9 pagesAdvantages and Disadvantages of Shares and Debenturekomal komal100% (1)

- HI 5001 Accounting For Business DecisionsDocument5 pagesHI 5001 Accounting For Business Decisionsalka murarkaNo ratings yet

- The Pioneer 159 EnglishDocument14 pagesThe Pioneer 159 EnglishMuhammad AfzaalNo ratings yet

- Standard Chartered SWIFT CodesDocument3 pagesStandard Chartered SWIFT Codeskhan 6090No ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- HBA - 25 Lakhs Order PDFDocument4 pagesHBA - 25 Lakhs Order PDFkarik1897No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)