You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Bill Williams New Trading DimensionsDocument24 pagesBill Williams New Trading DimensionsAmine Elghazi50% (2)

- Internet Trading Course The Complete Course in Online InvestmentDocument353 pagesInternet Trading Course The Complete Course in Online InvestmentAmine ElghaziNo ratings yet

- Ganapathy Vidyamurthy Pairs TradingDocument475 pagesGanapathy Vidyamurthy Pairs TradingAmine ElghaziNo ratings yet

- Swing Trading Simplified Larry D Spears PDFDocument115 pagesSwing Trading Simplified Larry D Spears PDFAmine Elghazi100% (4)

- Moving From SBS To Office 365 and Azure: @directorciaDocument50 pagesMoving From SBS To Office 365 and Azure: @directorciaAmine ElghaziNo ratings yet

- Remote Desktop Support With VNCDocument3 pagesRemote Desktop Support With VNCAmine ElghaziNo ratings yet

- Islamic Hire Purchase - Ijarah - in Dual Banking SystemsDocument25 pagesIslamic Hire Purchase - Ijarah - in Dual Banking SystemsAmine ElghaziNo ratings yet

- Islamic Hire-Purchase - IjarahDocument28 pagesIslamic Hire-Purchase - IjarahAmine ElghaziNo ratings yet

- Khiyar Aib Dalam Ba'i Al-MurabahahDocument9 pagesKhiyar Aib Dalam Ba'i Al-MurabahahmasterridNo ratings yet

- Al Rahn and Mortgage in Islamic Home FinancingDocument13 pagesAl Rahn and Mortgage in Islamic Home FinancingAmine ElghaziNo ratings yet

- Simulation in Islamic EconomicsDocument39 pagesSimulation in Islamic EconomicsAmine ElghaziNo ratings yet

- Microeconomics Within The Islamic FrameworkDocument1 pageMicroeconomics Within The Islamic FrameworkAmine ElghaziNo ratings yet

- The Role Objectives and Instrumentsof The Government For Helping Realize The Maqasid Alshari Ah in An Islamic Economy2Document10 pagesThe Role Objectives and Instrumentsof The Government For Helping Realize The Maqasid Alshari Ah in An Islamic Economy2Amine ElghaziNo ratings yet

- Promoting Employment and Minimizing Unemployment in An Islamic EconomyDocument16 pagesPromoting Employment and Minimizing Unemployment in An Islamic EconomyAmine ElghaziNo ratings yet

- Macroeconomics Within Islamic Framework 2Document14 pagesMacroeconomics Within Islamic Framework 2Amine Elghazi100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Case Study Grameen BankDocument7 pagesCase Study Grameen BankkatnavNo ratings yet

- Current Account 05 June 2021 To 02 July 2021: Your Account Arranged Overdraft Limit 240Document5 pagesCurrent Account 05 June 2021 To 02 July 2021: Your Account Arranged Overdraft Limit 240Carla GomesNo ratings yet

- OutputDocument31 pagesOutputvenkatachalapathy.thNo ratings yet

- Sadiq Hoi PDFDocument2 pagesSadiq Hoi PDFHafiz Shoaib MaqsoodNo ratings yet

- Comparative Study of Education Loan Between Sbi and IciciDocument82 pagesComparative Study of Education Loan Between Sbi and IciciAvtaar Singh50% (2)

- Metropolitan Bank and Trust Company, Petitioner, The First National City Bank and The Court of AppealsDocument2 pagesMetropolitan Bank and Trust Company, Petitioner, The First National City Bank and The Court of AppealsrdNo ratings yet

- The IB League Case StudyDocument6 pagesThe IB League Case StudyNidhi KumarNo ratings yet

- A Study On Customer Satisfaction of Reliance Life Insurance at HyderabadDocument8 pagesA Study On Customer Satisfaction of Reliance Life Insurance at Hyderabads_kumaresh_raghavanNo ratings yet

- Investment BankingDocument57 pagesInvestment BankingKinnari Singh75% (4)

- File0 108375089566351Document8 pagesFile0 108375089566351apark_100% (1)

- Transfer of Certificate of InsuranceDocument3 pagesTransfer of Certificate of InsuranceAnkur ChopraNo ratings yet

- Chief Executive Officer President in Minneapolis ST Paul MN Resume Gregory GottsackerDocument3 pagesChief Executive Officer President in Minneapolis ST Paul MN Resume Gregory GottsackerGregoryGottsacker100% (1)

- JPM Insurance PrimerDocument104 pagesJPM Insurance Primerdamon_enola3313No ratings yet

- SCA Reading ListDocument13 pagesSCA Reading ListMaria Lea Bernadeth OticoNo ratings yet

- Bank Statement EditedDocument4 pagesBank Statement EditedAllen MedinaNo ratings yet

- ISDA Standard CDS Contract Converter Specification - Sept 4, 2009Document4 pagesISDA Standard CDS Contract Converter Specification - Sept 4, 2009Ymae AlmonteNo ratings yet

- PDF DocumentDocument9 pagesPDF DocumentnahidahcomNo ratings yet

- HDFC Bank CV MAHARASHTRA Online Auction - 11-09-2020: Event CatalogueDocument8 pagesHDFC Bank CV MAHARASHTRA Online Auction - 11-09-2020: Event Catalogueatul4uNo ratings yet

- Housing LoanDocument36 pagesHousing LoanHabeeb UppinangadyNo ratings yet

- VXV DY23 LCD 47 C QGDocument2 pagesVXV DY23 LCD 47 C QGhp34thNo ratings yet

- Description: Tags: GAFRGuideandDPIFinalDocument2 pagesDescription: Tags: GAFRGuideandDPIFinalanon-210008No ratings yet

- ShineDocument15 pagesShinemahajan.gouravNo ratings yet

- Freddie Mac & Fannie Mae and MGIC Underwriting GuidelinesDocument6 pagesFreddie Mac & Fannie Mae and MGIC Underwriting Guidelines83jjmackNo ratings yet

- Audit of ReceivablesDocument9 pagesAudit of Receivablesmissy100% (2)

- Midterm Exam Global Stumble PDFDocument2 pagesMidterm Exam Global Stumble PDFBim BimNo ratings yet

- Insurance Written ReportDocument6 pagesInsurance Written ReportChasmere MagloyuanNo ratings yet

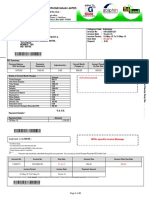

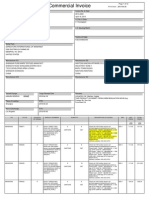

- Commercial Invoice: Consignee L/C Issuing BankDocument12 pagesCommercial Invoice: Consignee L/C Issuing Bankmz007No ratings yet

- Force Majeure Clauses in ICC Rules 1559904833 PDFDocument27 pagesForce Majeure Clauses in ICC Rules 1559904833 PDFReena TahirNo ratings yet

- LC Business Overseas BranchesDocument202 pagesLC Business Overseas BranchesSumalNo ratings yet

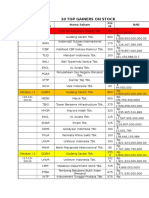

- 10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABDocument6 pages10 Top Gainers On Stock: Bulan/Min Ggu Kode Saham Nama Saham Poi NT NABFajRin WiCaksonoNo ratings yet