You might also like

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Larsen & Toubro: Performance HighlightsDocument14 pagesLarsen & Toubro: Performance HighlightsrajpersonalNo ratings yet

- Alembic Angel 020810Document12 pagesAlembic Angel 020810giridesh3No ratings yet

- Amara Raja Batteries: Performance HighlightsDocument10 pagesAmara Raja Batteries: Performance HighlightssuneshsNo ratings yet

- Performance Highlights: NeutralDocument10 pagesPerformance Highlights: Neutralvipin51No ratings yet

- IVRCL Infrastructure: Performance HighlightsDocument11 pagesIVRCL Infrastructure: Performance HighlightsPratik GanatraNo ratings yet

- Bharat Forge: Performance HighlightsDocument13 pagesBharat Forge: Performance HighlightsarikuldeepNo ratings yet

- AngelBrokingResearch AshokLayland 1QFY2016RU 140815 PDFDocument11 pagesAngelBrokingResearch AshokLayland 1QFY2016RU 140815 PDFAbhishek SinhaNo ratings yet

- JSW Energy: Fully PricedDocument13 pagesJSW Energy: Fully Pricedmihir_ajNo ratings yet

- Vascon Engineers - Kotak PCG PDFDocument7 pagesVascon Engineers - Kotak PCG PDFdarshanmadeNo ratings yet

- Simplex Infrastructures: Performance HighlightsDocument11 pagesSimplex Infrastructures: Performance Highlightskrishna615No ratings yet

- Ashok Leyland: Performance HighlightsDocument9 pagesAshok Leyland: Performance HighlightsSandeep ManglikNo ratings yet

- Bhel-3qfy11 Ru-210111Document12 pagesBhel-3qfy11 Ru-210111kshintlNo ratings yet

- Solarvest - 1QFY24Document4 pagesSolarvest - 1QFY24gee.yeap3959No ratings yet

- KEC International: Performance HighlightsDocument12 pagesKEC International: Performance HighlightsAnand MishraNo ratings yet

- Kirloskar Oil Engines: Performance HighlightsDocument12 pagesKirloskar Oil Engines: Performance Highlightsjetorres1No ratings yet

- Tata Motors: Performance HighlightsDocument10 pagesTata Motors: Performance HighlightsandrewpereiraNo ratings yet

- BHEL - Rock Solid - RBS - Jan2011Document8 pagesBHEL - Rock Solid - RBS - Jan2011Jitender KumarNo ratings yet

- No Quick Turnaround Seen For The San Gabriel: First Gen CorporationDocument2 pagesNo Quick Turnaround Seen For The San Gabriel: First Gen CorporationJohn Kyle LluzNo ratings yet

- Titan Industries: Performance HighlightsDocument10 pagesTitan Industries: Performance Highlightscbz786skNo ratings yet

- Latest Ceat ReportDocument6 pagesLatest Ceat Reportshubhamkumar.bhagat.23mbNo ratings yet

- KEC International - : Benefit From US$233bn Investment in The T&D SegmentDocument8 pagesKEC International - : Benefit From US$233bn Investment in The T&D Segmentharshul yadavNo ratings yet

- Inox RU4QFY2008 110608Document4 pagesInox RU4QFY2008 110608api-3862995No ratings yet

- Havells India Ltd. - INDSECDocument12 pagesHavells India Ltd. - INDSECResearch ReportsNo ratings yet

- Slowing Growth: Results Review 3qfy17 13 FEB 2017Document10 pagesSlowing Growth: Results Review 3qfy17 13 FEB 2017arun_algoNo ratings yet

- Eicher Motors LTD: Key Financial IndicatorsDocument4 pagesEicher Motors LTD: Key Financial IndicatorsSonam BaghaNo ratings yet

- Enil 25 8 08 PLDocument12 pagesEnil 25 8 08 PLapi-3862995No ratings yet

- Angel One - Update - Jul23 - HSIE-202307170719227368733Document9 pagesAngel One - Update - Jul23 - HSIE-202307170719227368733Ram JaneNo ratings yet

- Shiv Vani - IIFLDocument10 pagesShiv Vani - IIFLjunejagauravNo ratings yet

- Nomura - May 6 - CEATDocument12 pagesNomura - May 6 - CEATPrem SagarNo ratings yet

- Serba Dinamik: Hit To Reputation Amid Audit FlagsDocument4 pagesSerba Dinamik: Hit To Reputation Amid Audit FlagsRichbull TraderNo ratings yet

- A E L (AEL) : Mber Nterprises TDDocument8 pagesA E L (AEL) : Mber Nterprises TDdarshanmadeNo ratings yet

- IVRCL Infrastructure: Performance HighlightsDocument7 pagesIVRCL Infrastructure: Performance Highlightsanudeep05No ratings yet

- Icmnbo Abn AmroDocument9 pagesIcmnbo Abn AmrodivyakashNo ratings yet

- InterGlobe Aviation 2QFY20 Result Reveiw 24-10-19Document7 pagesInterGlobe Aviation 2QFY20 Result Reveiw 24-10-19Khush GosraniNo ratings yet

- Earnings To Provide A Reality Check Sell: Reliance IndustriesDocument33 pagesEarnings To Provide A Reality Check Sell: Reliance IndustriesChetankumar ChandakNo ratings yet

- APM Automotive Holdings Berhad: Riding On Motor Sector's Growth Cycle - 29/7/2010Document7 pagesAPM Automotive Holdings Berhad: Riding On Motor Sector's Growth Cycle - 29/7/2010Rhb InvestNo ratings yet

- Etihad Etisalat Company (Mobily) Defining A League... July 22, 2008Document36 pagesEtihad Etisalat Company (Mobily) Defining A League... July 22, 2008AliNo ratings yet

- Ramco Cement Q2FY24 ResultsDocument8 pagesRamco Cement Q2FY24 ResultseknathNo ratings yet

- Tata Steel: Performance HighlightsDocument13 pagesTata Steel: Performance HighlightssunnysmvduNo ratings yet

- IDFC Bank: CMP: Inr63 TP: INR68 (8%)Document8 pagesIDFC Bank: CMP: Inr63 TP: INR68 (8%)Devendra SarafNo ratings yet

- Suprajit Engineering: Status QuoDocument10 pagesSuprajit Engineering: Status QuoDinesh ChoudharyNo ratings yet

- ICICI Securities Sees 34% UPSIDE in Info Edge Green Shoots VisibleDocument6 pagesICICI Securities Sees 34% UPSIDE in Info Edge Green Shoots Visiblemanitjainm21No ratings yet

- VATW Q1FY24 ResultsDocument7 pagesVATW Q1FY24 ResultsVishalNo ratings yet

- Gail (India)Document93 pagesGail (India)Ashley KamalasanNo ratings yet

- KNR Constructions: Outperformance Priced inDocument8 pagesKNR Constructions: Outperformance Priced inarun_algoNo ratings yet

- Reliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Document18 pagesReliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Abhiroop DasNo ratings yet

- Airtel AnalysisDocument15 pagesAirtel AnalysisPriyanshi JainNo ratings yet

- 7204 D&O KENANGA 2023-08-24 SELL 2.30 DOGreenTechnologiesSluggishNewOrders - 167722211Document4 pages7204 D&O KENANGA 2023-08-24 SELL 2.30 DOGreenTechnologiesSluggishNewOrders - 167722211Nicholas ChehNo ratings yet

- LG Balakrishnan Bros - HSL - 180923 - EBRDocument11 pagesLG Balakrishnan Bros - HSL - 180923 - EBRSriram RanganathanNo ratings yet

- Ashok Leyland: Preparing To Reap Fruits When The Recovery StartsDocument10 pagesAshok Leyland: Preparing To Reap Fruits When The Recovery StartsKiran KudtarkarNo ratings yet

- Cairn India: Performance HighlightsDocument10 pagesCairn India: Performance HighlightsAngel BrokingNo ratings yet

- Anand Rural Electrification Corp Buy 25oct10Document2 pagesAnand Rural Electrification Corp Buy 25oct10bhunkus1327No ratings yet

- Cairn India: Performance HighlightsDocument10 pagesCairn India: Performance HighlightsAngel BrokingNo ratings yet

- Mergerd SND Acquisitions Case Study: ABC's Acquisitions of Xyx Submitted by Kinay Dave .No 36Document7 pagesMergerd SND Acquisitions Case Study: ABC's Acquisitions of Xyx Submitted by Kinay Dave .No 36akshayNo ratings yet

- Blue Star: Performance HighlightsDocument8 pagesBlue Star: Performance HighlightskasimimudassarNo ratings yet

- Tata Motors LTD: Result Update Aiming Near Net Debt Free (Automotive) by FY24Document5 pagesTata Motors LTD: Result Update Aiming Near Net Debt Free (Automotive) by FY24Shiv NarangNo ratings yet

- Thermax: Performance HighlightsDocument10 pagesThermax: Performance HighlightsAngel BrokingNo ratings yet

- Axiata Group BHD: Company ReportDocument6 pagesAxiata Group BHD: Company Reportlimml63No ratings yet

- TCS RR 12042022 - Retail 12 April 2022 1386121995Document13 pagesTCS RR 12042022 - Retail 12 April 2022 1386121995uefqyaufdQNo ratings yet

- Reference Dataset For Section 8 of Deciphering Indus Script As A CryptogramDocument20 pagesReference Dataset For Section 8 of Deciphering Indus Script As A CryptogramPraveen Kumar DusiNo ratings yet

- LECTURE 2 Bending StressesDocument11 pagesLECTURE 2 Bending StressesIvana DincicNo ratings yet

- Pancha RudramDocument7 pagesPancha RudramPraveen Kumar DusiNo ratings yet

- Purchase Details: 37617673987 DecemberDocument55 pagesPurchase Details: 37617673987 DecemberPraveen Kumar DusiNo ratings yet

- Titration 14 BDocument21 pagesTitration 14 BPraveen Kumar DusiNo ratings yet

- True Stress-Strain DiagramDocument19 pagesTrue Stress-Strain DiagramAmruth Babu V T100% (1)

- Co Code Asset Code If Created in Case of Similar Item (Needed For Creation of Sub Asset)Document5 pagesCo Code Asset Code If Created in Case of Similar Item (Needed For Creation of Sub Asset)Praveen Kumar DusiNo ratings yet

- Quotation-Lc For Hume Pipe LayingDocument1 pageQuotation-Lc For Hume Pipe LayingPraveen Kumar DusiNo ratings yet

- MatSam581031Algebra2ResourceSampler LowDocument60 pagesMatSam581031Algebra2ResourceSampler LowPraveen Kumar Dusi100% (1)

- Andhra Pradesh D Code1Document876 pagesAndhra Pradesh D Code1Avinash Rai72% (32)

- Materaial For Question 3. - Cooling Load CLTD Example Ashrae PDFDocument5 pagesMateraial For Question 3. - Cooling Load CLTD Example Ashrae PDFkumarNo ratings yet

- Banking Awareness Digest PO Mains 2015 Final1Document21 pagesBanking Awareness Digest PO Mains 2015 Final1Neha PankiNo ratings yet

- Decision Tree ClassificationDocument60 pagesDecision Tree ClassificationrajeswarikannanNo ratings yet

- Analysis of Indeterminate Structures by Force MethodDocument17 pagesAnalysis of Indeterminate Structures by Force Methodatish k100% (2)

- Banking Awareness Digest PO Mains 2015 Final1Document21 pagesBanking Awareness Digest PO Mains 2015 Final1Neha PankiNo ratings yet

- Cenvat Credit ProblemsDocument17 pagesCenvat Credit ProblemsPraveen Kumar DusiNo ratings yet

- Common Shape CodesDocument1 pageCommon Shape CodesIrfanNo ratings yet

- Project Report - Praveen KumarDocument78 pagesProject Report - Praveen KumarPraveen Kumar DusiNo ratings yet

- AmalgamationDocument44 pagesAmalgamationPraveen Kumar DusiNo ratings yet

- IBPS PO Computer DigestDocument28 pagesIBPS PO Computer DigestAravind BhomboreNo ratings yet

- PRJT, Nit SilcharDocument4 pagesPRJT, Nit SilcharPraveen Kumar DusiNo ratings yet

- 4682460.0458672 p1 - 1500000 Rs. 1,723,214.29 p2 - 1260000 Rs. 1,267,857.14 p3 - 700000 Rs. 693,750.00 Rs. 26,978.66 8.7708Document2 pages4682460.0458672 p1 - 1500000 Rs. 1,723,214.29 p2 - 1260000 Rs. 1,267,857.14 p3 - 700000 Rs. 693,750.00 Rs. 26,978.66 8.7708Praveen Kumar DusiNo ratings yet

- 4682460.0458672 p1 - 1500000 Rs. 1,723,214.29 p2 - 1260000 Rs. 1,267,857.14 p3 - 700000 Rs. 693,750.00 Rs. 26,978.66 8.7708Document2 pages4682460.0458672 p1 - 1500000 Rs. 1,723,214.29 p2 - 1260000 Rs. 1,267,857.14 p3 - 700000 Rs. 693,750.00 Rs. 26,978.66 8.7708Praveen Kumar DusiNo ratings yet

- CMR T-School Survey 2013Document9 pagesCMR T-School Survey 2013Praveen Kumar DusiNo ratings yet

- The Arbitration Act, 1940 1Document10 pagesThe Arbitration Act, 1940 1Praveen Kumar DusiNo ratings yet

- Common Shape CodesDocument1 pageCommon Shape CodesIrfanNo ratings yet

- All Pages - Final 11-05-2012Document270 pagesAll Pages - Final 11-05-2012Praveen Kumar DusiNo ratings yet

- National Workshop at NIT SilcharDocument2 pagesNational Workshop at NIT SilcharPraveen Kumar DusiNo ratings yet

- Rites Limited (A Govt. of India Enterprise)Document2 pagesRites Limited (A Govt. of India Enterprise)Praveen Kumar DusiNo ratings yet

- Class Resources Cribsheet1Document2 pagesClass Resources Cribsheet1Praveen Kumar DusiNo ratings yet

- FTDocumentDocument2 pagesFTDocumentGustavo UribeNo ratings yet

- 12th Balance of Payment MCQsDocument41 pages12th Balance of Payment MCQsrimjhim sahuNo ratings yet

- Sat YamDocument39 pagesSat YamShashank GuptaNo ratings yet

- 14643post 819 WircDocument945 pages14643post 819 WircRonak ShahNo ratings yet

- Report in BM 222Document5 pagesReport in BM 222Neil Dela Cruz AmmenNo ratings yet

- Follow Fibonacci Ratio Dynamic Approach in TradeDocument4 pagesFollow Fibonacci Ratio Dynamic Approach in TradeLatika DhamNo ratings yet

- Unit IvDocument26 pagesUnit Ivthella deva prasadNo ratings yet

- MCQ - LiabilitiesDocument4 pagesMCQ - LiabilitiesEshaNo ratings yet

- Quarterly Publication of Individuals, Who Have Chosen To Expatriate, As Required by Section 6039GDocument17 pagesQuarterly Publication of Individuals, Who Have Chosen To Expatriate, As Required by Section 6039GKelly Phillips ErbNo ratings yet

- Why Investors Must Wring Out HIGH Beta From Portfolio?Document4 pagesWhy Investors Must Wring Out HIGH Beta From Portfolio?Yogesh V GabaniNo ratings yet

- Issues and Challenges of Insurance Industry in IndiaDocument3 pagesIssues and Challenges of Insurance Industry in Indianishant b100% (1)

- Reinstatement of Provision of Earnest Money Deposit (Er (D) in BidsDocument10 pagesReinstatement of Provision of Earnest Money Deposit (Er (D) in BidsDevesh Kumar PandeyNo ratings yet

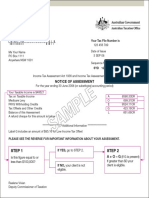

- Step 1 Step 2: Notice of AssessmentDocument1 pageStep 1 Step 2: Notice of Assessmentabinash manandharNo ratings yet

- MATRIX 2-Tax-RevDocument18 pagesMATRIX 2-Tax-RevJepoy FranciscoNo ratings yet

- 35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc MsDocument90 pages35 Financial Management FM 71 Imp Questions With Solution For CA Ipcc Msmysorevishnu75% (8)

- Invoice - Ali Abid - 000660485Document1 pageInvoice - Ali Abid - 000660485AliAbidNo ratings yet

- Cii Qualifications BrochureDocument45 pagesCii Qualifications BrochureErnest Kofi AsanteNo ratings yet

- Fac4863 104 - 2020 - 0 - BDocument93 pagesFac4863 104 - 2020 - 0 - BNISSIBETINo ratings yet

- ATC List 2017 Updated 5517Document47 pagesATC List 2017 Updated 5517Varinder AnandNo ratings yet

- ATT Receipt George PDFDocument1 pageATT Receipt George PDFBrennan BargerNo ratings yet

- ADVANCED FA Chap IIIDocument7 pagesADVANCED FA Chap IIIFasiko Asmaro100% (1)

- Topic 14 - Estate PlanningDocument57 pagesTopic 14 - Estate PlanningArun GhatanNo ratings yet

- Model Asset and Liability Affidavit D. VDocument12 pagesModel Asset and Liability Affidavit D. VsavagecommentorNo ratings yet

- Accounting Words IDocument1 pageAccounting Words IArnold SilvaNo ratings yet

- Investment Environment and Investment Management Process-1Document1 pageInvestment Environment and Investment Management Process-1CalvinsNo ratings yet

- Assignment On MoneybhaiDocument7 pagesAssignment On MoneybhaiKritibandhu SwainNo ratings yet

- Analysis of Systematic Investment PlanDocument35 pagesAnalysis of Systematic Investment PlanSAVINo ratings yet

- Rent Vs Buy CalculatorDocument10 pagesRent Vs Buy Calculatordesai ashokNo ratings yet

- Direst Selling Agent Policy-Retail & Consumer LendingDocument13 pagesDirest Selling Agent Policy-Retail & Consumer LendingVijay DubeyNo ratings yet

- Receivable ManagementDocument39 pagesReceivable ManagementIquesh Gupta100% (1)