You might also like

- FM - Master BudgetDocument5 pagesFM - Master BudgetChristine Angeli AritaNo ratings yet

- Budgeting - ExamplesDocument2 pagesBudgeting - Examplessunil.ctNo ratings yet

- Corp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284Document4 pagesCorp-Bgt#IUP-X#Sept21#Aldira Jasmine R A#12010119190284aldira jasmineNo ratings yet

- Budget Format Sales Budget: Cash Collection Total Budgeted SalesDocument6 pagesBudget Format Sales Budget: Cash Collection Total Budgeted Salessernhaow_658673991No ratings yet

- Manufacturing Company BudgetingDocument10 pagesManufacturing Company BudgetingSajakul SornNo ratings yet

- Budgeting - Planning: A325 Discussion - March 19, 2012Document8 pagesBudgeting - Planning: A325 Discussion - March 19, 2012alfaNo ratings yet

- Prepare flexible budgets and cash budgets for business managementDocument3 pagesPrepare flexible budgets and cash budgets for business managementSHARATH JNo ratings yet

- Panta budget schedules for production, materials, laborDocument10 pagesPanta budget schedules for production, materials, laborFiles OrganizedNo ratings yet

- RF Ltd Cash BudgetDocument26 pagesRF Ltd Cash BudgetRiaz Baloch Notezai100% (1)

- Acctg 202Document9 pagesAcctg 202Lore Desa CenizaNo ratings yet

- SCM 2ND SemDocument9 pagesSCM 2ND SemRiki AsahiNo ratings yet

- Master Budgeting (Sample Problems With Answers)Document11 pagesMaster Budgeting (Sample Problems With Answers)Jonalyn TaboNo ratings yet

- SolutionDocument6 pagesSolutionJhazzie Dolor100% (1)

- Budgeting and Forecasting for BusinessesDocument4 pagesBudgeting and Forecasting for BusinessesSoumendra RoyNo ratings yet

- Quiz 2Document4 pagesQuiz 2VAIBHAV RAJNo ratings yet

- Turabi Ltd income statement and balance sheetDocument7 pagesTurabi Ltd income statement and balance sheetFarwa SamreenNo ratings yet

- CH 22 Various Exercises Setup 27 Ed.Document6 pagesCH 22 Various Exercises Setup 27 Ed.Kearrion BryantNo ratings yet

- Bud GettingDocument8 pagesBud GettingLorena Mae LasquiteNo ratings yet

- Reggie's BudgetDocument5 pagesReggie's BudgetYazan AdamNo ratings yet

- Financial Forecasting: Production Requirements (LO2) Sales For Western Boot Stores Are Expected To Be 40,000Document13 pagesFinancial Forecasting: Production Requirements (LO2) Sales For Western Boot Stores Are Expected To Be 40,000Juliet Dorado100% (1)

- Chapter 4 ExerciseDocument7 pagesChapter 4 ExerciseJoe DicksonNo ratings yet

- Profitability DemoDocument225 pagesProfitability Demoshahin2014No ratings yet

- Tahbeer Financial Plan - Financial PlanDocument7 pagesTahbeer Financial Plan - Financial PlanSonam GulzarNo ratings yet

- Cash BudgetingDocument3 pagesCash Budgetingsunil.ctNo ratings yet

- Opal ProjectsDocument3 pagesOpal ProjectsMigs CruzNo ratings yet

- 5 38Document15 pages5 38Seth CabreraNo ratings yet

- Comprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFDocument9 pagesComprehensive Illustration of Consolidated Financial Statements - Intercompany Sale of Inventories PDFamie honnagNo ratings yet

- Unit 7 Budgeting SolutionsDocument15 pagesUnit 7 Budgeting SolutionsYogesh BandiNo ratings yet

- Asynchronous Statement of Financial Position XYZ CompanyDocument5 pagesAsynchronous Statement of Financial Position XYZ CompanyDiana Fernandez MagnoNo ratings yet

- 99 A Benzeer Tanha Funfin FinalsDocument7 pages99 A Benzeer Tanha Funfin FinalsBenzeer TanhaNo ratings yet

- Budgeting Problems PDFDocument5 pagesBudgeting Problems PDFER Aditya DasNo ratings yet

- Ms-04: Accounting and Finance For Managers: Dear StudentsDocument3 pagesMs-04: Accounting and Finance For Managers: Dear Studentsshajirbran7769100% (1)

- Penyusutan - Peralatan KantorDocument16 pagesPenyusutan - Peralatan KantorSiti Hajar AsmawiahNo ratings yet

- Cash Management QuestionsDocument5 pagesCash Management QuestionsManasi Jamsandekar100% (1)

- Handout - Week 6 - Financial Planning and Forecasting-1662440842139Document8 pagesHandout - Week 6 - Financial Planning and Forecasting-1662440842139Muhammad Raihan AzicaNo ratings yet

- Acn202 AssignmentDocument5 pagesAcn202 AssignmentAvijit Kumar SahaNo ratings yet

- Ca Ipcc Costing and Financial Management Suggested Answers May 2015Document20 pagesCa Ipcc Costing and Financial Management Suggested Answers May 2015Prasanna KumarNo ratings yet

- Questions On Cash Budget-2Document7 pagesQuestions On Cash Budget-2Mpolokeng HlabanaNo ratings yet

- FSA Vertical FormatDocument10 pagesFSA Vertical FormatMayank BahetiNo ratings yet

- Master BudgetDocument12 pagesMaster Budgetshi shiiisshhNo ratings yet

- Financial and Management AccountingDocument2 pagesFinancial and Management AccountingHarshithNo ratings yet

- Mba 104 PDFDocument2 pagesMba 104 PDFSimanta KalitaNo ratings yet

- AFM-Session 25Document13 pagesAFM-Session 25abhijit.kundu23-25No ratings yet

- Final Budget ProjectDocument102 pagesFinal Budget Projectapi-354593764No ratings yet

- AFM Solution SumitDocument4 pagesAFM Solution SumitSumitNo ratings yet

- Sales Budget and Production Plan AnalysisDocument19 pagesSales Budget and Production Plan AnalysisMervin MalaranNo ratings yet

- CHP 2AnalysisInterpretationofAccountsDocument5 pagesCHP 2AnalysisInterpretationofAccountsalpeshmahto2004No ratings yet

- Exercises 7A1 and 7B1: Book: Administrative AccountingDocument9 pagesExercises 7A1 and 7B1: Book: Administrative AccountingScribdTranslationsNo ratings yet

- Budget and B Udgetary C OntrolDocument6 pagesBudget and B Udgetary C OntrolKanika DahiyaNo ratings yet

- IA Chapter-11-14Document7 pagesIA Chapter-11-14Christine Joyce EnriquezNo ratings yet

- Butle 1Document17 pagesButle 1Gursharan KohliNo ratings yet

- 12-Month Rolling Incentive and Commission Plan for Net New BusinessDocument1 page12-Month Rolling Incentive and Commission Plan for Net New BusinessChay CruzNo ratings yet

- MASTER-BUDGETDocument36 pagesMASTER-BUDGETRafols AnnabelleNo ratings yet

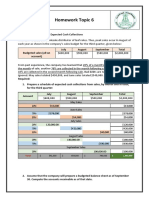

- Homework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionsDocument3 pagesHomework Topic 6: EXERCISE 8-1 Schedule of Expected Cash CollectionskhetamNo ratings yet

- Acct 2020 EportfolioDocument5 pagesAcct 2020 Eportfolioapi-311375616No ratings yet

- Budgeting 30 NOvDocument8 pagesBudgeting 30 NOvHaris HasanNo ratings yet

- Budgetary ControlDocument5 pagesBudgetary ControlJasdeep Singh DeepuNo ratings yet

- Coupons For Jobs 03-08-10Document21 pagesCoupons For Jobs 03-08-10jack9778No ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- Economic & Budget Forecast Workbook: Economic workbook with worksheetFrom EverandEconomic & Budget Forecast Workbook: Economic workbook with worksheetNo ratings yet

- NullDocument2 pagesNullajithsubramanianNo ratings yet

- NullDocument2 pagesNullajithsubramanianNo ratings yet

- Budgetind Concepts and Forecoasting TechniquesDocument26 pagesBudgetind Concepts and Forecoasting TechniquesajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- Cma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)Document8 pagesCma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)ajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- NullDocument2 pagesNullajithsubramanianNo ratings yet

- NullDocument1 pageNullajithsubramanianNo ratings yet

- Cma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)Document8 pagesCma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)ajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- Cma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)Document8 pagesCma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)ajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- NullDocument10 pagesNullajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- NullDocument10 pagesNullajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- NullDocument10 pagesNullajithsubramanianNo ratings yet

- NullDocument10 pagesNullajithsubramanianNo ratings yet

- Cma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)Document8 pagesCma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)ajithsubramanianNo ratings yet

- Cma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)Document8 pagesCma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)ajithsubramanianNo ratings yet

- File NOT FOUND:content - CasestudyDocument1 pageFile NOT FOUND:content - CasestudyajithsubramanianNo ratings yet

- Budgeting Concepts and Forecasting TechniquesDocument26 pagesBudgeting Concepts and Forecasting TechniquesajithsubramanianNo ratings yet

- NullDocument13 pagesNullajithsubramanianNo ratings yet

- Cma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)Document8 pagesCma 2010 Curriculum and Format: Content Specification Overview (Effective May 1, 2010)ajithsubramanianNo ratings yet

- Budgeting Concepts and Forecasting TechniquesDocument26 pagesBudgeting Concepts and Forecasting TechniquesajithsubramanianNo ratings yet

- File NOT FOUND:content - CasestudyDocument1 pageFile NOT FOUND:content - CasestudyajithsubramanianNo ratings yet

- File NOT FOUND:content - SyllabusDocument1 pageFile NOT FOUND:content - SyllabusajithsubramanianNo ratings yet

- NullDocument22 pagesNullajithsubramanianNo ratings yet

- Prof 7 - Capital Market SyllabusDocument10 pagesProf 7 - Capital Market SyllabusGo Ivanizerrckc100% (1)

- Evirtualguru Computerscience 43 PDFDocument8 pagesEvirtualguru Computerscience 43 PDFJAGANNATH THAWAITNo ratings yet

- HOTC 1 TheFoundingoftheChurchandtheEarlyChristians PPPDocument42 pagesHOTC 1 TheFoundingoftheChurchandtheEarlyChristians PPPSuma HashmiNo ratings yet

- Recommender Systems Research GuideDocument28 pagesRecommender Systems Research GuideSube Singh InsanNo ratings yet

- AGIL KENYA For Web - tcm141-76354Document4 pagesAGIL KENYA For Web - tcm141-76354Leah KimuhuNo ratings yet

- Chippernac: Vacuum Snout Attachment (Part Number 1901113)Document2 pagesChippernac: Vacuum Snout Attachment (Part Number 1901113)GeorgeNo ratings yet

- SuccessDocument146 pagesSuccessscribdNo ratings yet

- Introduction To ResearchDocument5 pagesIntroduction To Researchapi-385504653No ratings yet

- Lean Foundation TrainingDocument9 pagesLean Foundation TrainingSaja Unķnøwñ ĞirłNo ratings yet

- Bakhtar University: Graduate School of Business AdministrationDocument3 pagesBakhtar University: Graduate School of Business AdministrationIhsanulhaqnooriNo ratings yet

- Postmodern Dystopian Fiction: An Analysis of Bradbury's Fahrenheit 451' Maria AnwarDocument4 pagesPostmodern Dystopian Fiction: An Analysis of Bradbury's Fahrenheit 451' Maria AnwarAbdennour MaafaNo ratings yet

- A StarDocument59 pagesA Starshahjaydip19912103No ratings yet

- (Coffeemaker) Tas5542uc - Instructions - For - UseDocument74 pages(Coffeemaker) Tas5542uc - Instructions - For - UsePolina BikoulovNo ratings yet

- AMU2439 - EssayDocument4 pagesAMU2439 - EssayFrancesca DivaNo ratings yet

- State of Indiana, County of Marion, SS: Probable Cause AffidavitDocument1 pageState of Indiana, County of Marion, SS: Probable Cause AffidavitIndiana Public Media NewsNo ratings yet

- Configure Initial ISAM Network SettingsDocument4 pagesConfigure Initial ISAM Network SettingsnelusabieNo ratings yet

- How Should Management Be Structured British English StudentDocument7 pagesHow Should Management Be Structured British English Studentr i s uNo ratings yet

- Emilia Perroni-Play - Psychoanalytic Perspectives, Survival and Human Development-Routledge (2013) PDFDocument262 pagesEmilia Perroni-Play - Psychoanalytic Perspectives, Survival and Human Development-Routledge (2013) PDFMihaela Ioana MoldovanNo ratings yet

- Hays Grading System: Group Activity 3 Groups KH PS Acct TS JG PGDocument1 pageHays Grading System: Group Activity 3 Groups KH PS Acct TS JG PGkuku129No ratings yet

- Xtreme 5 (Answer-Key)Document120 pagesXtreme 5 (Answer-Key)arielsergio403No ratings yet

- Visual AnalysisDocument4 pagesVisual Analysisapi-35602981850% (2)

- Susan Oyama The Ontogeny of Information Developmental Systems and Evolution Science and Cultural Theory 2000Document297 pagesSusan Oyama The Ontogeny of Information Developmental Systems and Evolution Science and Cultural Theory 2000Marelin Hernández SaNo ratings yet

- VT JCXDocument35 pagesVT JCXAkshay WingriderNo ratings yet

- SubjectivityinArtHistoryandArt CriticismDocument12 pagesSubjectivityinArtHistoryandArt CriticismMohammad SalauddinNo ratings yet

- Drama For Kids A Mini Unit On Emotions and Character F 2Document5 pagesDrama For Kids A Mini Unit On Emotions and Character F 2api-355762287No ratings yet

- Good Paper On Time SerisDocument15 pagesGood Paper On Time SerisNamdev UpadhyayNo ratings yet

- PNP TELEPHONE DIRECTORY As of JUNE 2022Document184 pagesPNP TELEPHONE DIRECTORY As of JUNE 2022lalainecd0616No ratings yet

- I CEV20052 Structureofthe Food Service IndustryDocument98 pagesI CEV20052 Structureofthe Food Service IndustryJowee TigasNo ratings yet

- Cost Accounting - LabourDocument7 pagesCost Accounting - LabourSaad Khan YTNo ratings yet