You might also like

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- ACCCOB2 Chapter 4 ExercisesDocument4 pagesACCCOB2 Chapter 4 ExercisesChelcy Mari GugolNo ratings yet

- Digital Marketing StrategyDocument74 pagesDigital Marketing Strategymillionbemac8No ratings yet

- Liberty Shoes LTD PDFDocument8 pagesLiberty Shoes LTD PDFsakshamNo ratings yet

- Journal of Trading - Behind Stock Price MovementDocument12 pagesJournal of Trading - Behind Stock Price MovementRichard DennisNo ratings yet

- Corporate Finance Report On LegoDocument8 pagesCorporate Finance Report On LegoAnna StoychevaNo ratings yet

- Hyundai Motor Company 1q 2022 Consolidated FinalDocument61 pagesHyundai Motor Company 1q 2022 Consolidated FinalNitesh SinghNo ratings yet

- ACCT5001 2022 S2 - Module 2 - Lecture Slides StudentDocument33 pagesACCT5001 2022 S2 - Module 2 - Lecture Slides Studentwuzhen102110No ratings yet

- ACSM - Annual Report 2020 - Part 1Document27 pagesACSM - Annual Report 2020 - Part 1kokueiNo ratings yet

- Fi507e Fie Annexe 21 22 OnlineDocument5 pagesFi507e Fie Annexe 21 22 OnlinePoorvi AgrawalNo ratings yet

- Hortifrut - Comprar - La Compañía Fortalece Su Presencia en Europa A Lo Largo de La Cadena de ValorDocument2 pagesHortifrut - Comprar - La Compañía Fortalece Su Presencia en Europa A Lo Largo de La Cadena de ValorAndres UrrutiaNo ratings yet

- Chapter 6 GitmanDocument14 pagesChapter 6 GitmanLee Shaykh86% (7)

- Harrison 5ce ISM Ch03Document105 pagesHarrison 5ce ISM Ch03PmNo ratings yet

- Cash Flow Statement: (Cheat Sheet)Document5 pagesCash Flow Statement: (Cheat Sheet)LinyVatNo ratings yet

- Matheson ElectronicsDocument2 pagesMatheson ElectronicsReg Lagarteja80% (5)

- Cma End Game NotesDocument75 pagesCma End Game NotesManish BabuNo ratings yet

- Chapter 5 - Financial Management and Policies - SyllabusDocument7 pagesChapter 5 - Financial Management and Policies - SyllabusharithraaNo ratings yet

- Sample Questions:: Section I: Subjective QuestionsDocument8 pagesSample Questions:: Section I: Subjective QuestionsketanNo ratings yet

- Acc 109 Quiz 1 P3Document2 pagesAcc 109 Quiz 1 P3GargaritanoNo ratings yet

- Class 12 Accountancy Question Bank Nov 2023Document105 pagesClass 12 Accountancy Question Bank Nov 2023vansh555palNo ratings yet

- AssignmentDocument12 pagesAssignmentpavnijainNo ratings yet

- Company Law ProjectDocument6 pagesCompany Law ProjectKumar HarshNo ratings yet

- Chapter 8 Managing Transaction RisksDocument22 pagesChapter 8 Managing Transaction Risksmatthew kobulnickNo ratings yet

- 2023 December Nick Atkeson How To Make Money in A World Where Fin Analyst Are WrongDocument60 pages2023 December Nick Atkeson How To Make Money in A World Where Fin Analyst Are WrongBob ReeceNo ratings yet

- Financial Reporting and Analysis (OUpm001111)Document10 pagesFinancial Reporting and Analysis (OUpm001111)SagarPirtheeNo ratings yet

- FM Mbaquiz1Document4 pagesFM Mbaquiz1Pritee SinghNo ratings yet

- Mba Capital BudgetingDocument14 pagesMba Capital BudgetingGagan Deep0% (1)

- AFAR-09 (Separate & Consolidated Financial Statements)Document10 pagesAFAR-09 (Separate & Consolidated Financial Statements)Hasmin AmpatuaNo ratings yet

- Camel Analysis Meezan BankDocument11 pagesCamel Analysis Meezan BankHabiba PashaNo ratings yet

- HELP Bachelor of Business Subject Availability. - SUBANG CAMPUSDocument3 pagesHELP Bachelor of Business Subject Availability. - SUBANG CAMPUSjingen0203No ratings yet

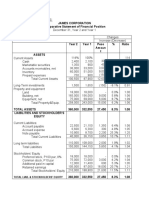

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionDocument7 pagesHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananNo ratings yet