You might also like

- Certificate of Payment of Foreign Death Tax: For Paperwork Reduction Act Notice, See The Back of This FormDocument2 pagesCertificate of Payment of Foreign Death Tax: For Paperwork Reduction Act Notice, See The Back of This FormFrancis Wolfgang UrbanNo ratings yet

- WWW - Irs.gov Pub Irs-PDF f4506tDocument2 pagesWWW - Irs.gov Pub Irs-PDF f4506tJennifer GonzalezNo ratings yet

- Sav 3500Document1 pageSav 3500MichaelNo ratings yet

- Received: Return of Organization Exempt From Income TaxDocument16 pagesReceived: Return of Organization Exempt From Income Taxcmf8926No ratings yet

- Tally Accounting Package Shortcut KeysDocument40 pagesTally Accounting Package Shortcut KeysRaja Vishnudas100% (1)

- SFF IRS Form990 2013Document27 pagesSFF IRS Form990 2013Space Frontier FoundationNo ratings yet

- DT 2008 990Document53 pagesDT 2008 990shimeralumNo ratings yet

- Exemption of Utah Safety and Emission Requirements For Vehicles Not in UtahDocument2 pagesExemption of Utah Safety and Emission Requirements For Vehicles Not in Utahtrustkonan100% (1)

- Instructions For Form 1120Document31 pagesInstructions For Form 1120A.F. GRANADANo ratings yet

- Secretary of State LLC Filing for DSJ Real Estate HoldingsDocument2 pagesSecretary of State LLC Filing for DSJ Real Estate HoldingsDoo Soo KimNo ratings yet

- Complaint: Federal Trade Commission (FTC) : Complaints Against Sean Hannity, Freedom Concerts and Freedom Alliance: 3/29/10 - FTC Complaint CitationsDocument254 pagesComplaint: Federal Trade Commission (FTC) : Complaints Against Sean Hannity, Freedom Concerts and Freedom Alliance: 3/29/10 - FTC Complaint CitationsCREWNo ratings yet

- Reporting Agent Authorization Form 8655Document2 pagesReporting Agent Authorization Form 8655bilalNo ratings yet

- Bloomberg 2012Document316 pagesBloomberg 2012josephlordNo ratings yet

- SCC Irs Form 990 2013Document27 pagesSCC Irs Form 990 2013L. A. PatersonNo ratings yet

- Expat Tax AzDocument6 pagesExpat Tax Azkcr240No ratings yet

- Submitting Your U.S. Tax Documents: Print, Sign, MailDocument5 pagesSubmitting Your U.S. Tax Documents: Print, Sign, MailGia Han100% (1)

- US Internal Revenue Service: f1099c - 2005Document6 pagesUS Internal Revenue Service: f1099c - 2005IRSNo ratings yet

- 2018 PDFDocument138 pages2018 PDFaaronweNo ratings yet

- The Gift Tax Made Simple - TurboTax Tax Tips & VideosDocument4 pagesThe Gift Tax Made Simple - TurboTax Tax Tips & Videossrinivas NNo ratings yet

- 2009 Form 990-EZDocument4 pages2009 Form 990-EZCircuit MediaNo ratings yet

- F 8655Document2 pagesF 8655IRSNo ratings yet

- F 1040 VDocument2 pagesF 1040 VNotarys To Go0% (1)

- Form of Protest Which May in Terms of Section Ninety-Eight ofDocument3 pagesForm of Protest Which May in Terms of Section Ninety-Eight ofJohn KronnickNo ratings yet

- I 843Document6 pagesI 843ayi imaduddinNo ratings yet

- Temn Cert 2Document2 pagesTemn Cert 2smallcapsmarketNo ratings yet

- 1040x2 PDFDocument2 pages1040x2 PDFolddiggerNo ratings yet

- Processed: Form6 Full and Public Disclosure of 2012 Financial InterestsDocument2 pagesProcessed: Form6 Full and Public Disclosure of 2012 Financial InterestsMy-Acts Of-SeditionNo ratings yet

- Foreign Earned Income: 34 For Use by U.S. Citizens and Resident Aliens OnlyDocument3 pagesForeign Earned Income: 34 For Use by U.S. Citizens and Resident Aliens OnlyballsinhandNo ratings yet

- Public Law 95-147 95th Congress An ActDocument3 pagesPublic Law 95-147 95th Congress An ActSylvester MooreNo ratings yet

- CCC 2941 Re ConveyanceDocument5 pagesCCC 2941 Re ConveyanceChelsea LeeNo ratings yet

- Advanced Scenario 7: Quincy and Marian Pike (2017)Document10 pagesAdvanced Scenario 7: Quincy and Marian Pike (2017)Center for Economic Progress100% (1)

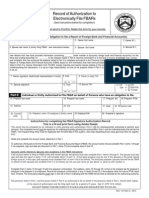

- Fincen FBAR 114Document1 pageFincen FBAR 114qwerasdf131100% (1)

- Project Homeless Connect 2012 990Document14 pagesProject Homeless Connect 2012 990auweia1No ratings yet

- Form 2220Document15 pagesForm 2220Kam 87No ratings yet

- Form 1040NR-EZ Tax Return for Nonresident AliensDocument2 pagesForm 1040NR-EZ Tax Return for Nonresident AliensElena Alexandra CărăvanNo ratings yet

- IRS Publication Form 706 GSTDocument3 pagesIRS Publication Form 706 GSTFrancis Wolfgang UrbanNo ratings yet

- Cannon FOIA ScreenshotsDocument252 pagesCannon FOIA ScreenshotsJ BambergNo ratings yet

- 2202 Schedule of Liabilities-508Document1 page2202 Schedule of Liabilities-508DjibzlaeNo ratings yet

- US Internal Revenue Service: f9325Document2 pagesUS Internal Revenue Service: f9325IRSNo ratings yet

- Direct Deposit Sign-Up Form (Philippines)Document3 pagesDirect Deposit Sign-Up Form (Philippines)Noeh PiedadNo ratings yet

- Texas Corporation Certificate of FormationDocument6 pagesTexas Corporation Certificate of FormationRocketLawyer100% (1)

- Introduction:-: WorksheetDocument24 pagesIntroduction:-: WorksheetbharatNo ratings yet

- Compilation of Guidelines For Redress of Public Grievances - Naresh KadyanDocument290 pagesCompilation of Guidelines For Redress of Public Grievances - Naresh KadyanNaresh KadyanNo ratings yet

- MSB Registration From FinCENDocument1 pageMSB Registration From FinCENCoin FireNo ratings yet

- Untermeyer 6751 Registration Statement 20191119 1Document7 pagesUntermeyer 6751 Registration Statement 20191119 1Yvonne LarsenNo ratings yet

- Electronically Available FSA-2041 Form AssignmentDocument2 pagesElectronically Available FSA-2041 Form AssignmentSteve NguyenNo ratings yet

- p4012 (2018)Document349 pagesp4012 (2018)Center for Economic ProgressNo ratings yet

- 2018 NoVo 990Document80 pages2018 NoVo 990Noam Blum100% (1)

- GKEDC Form 990 Page 1 For 2013 Through 2019Document7 pagesGKEDC Form 990 Page 1 For 2013 Through 2019Don MooreNo ratings yet

- Reporting Agent Authorization: Sign HereDocument1 pageReporting Agent Authorization: Sign HereSam OziegbeNo ratings yet

- OFAC Blocking Form v2Document2 pagesOFAC Blocking Form v2Ronald WederfoortNo ratings yet

- Federal Deposit Insurance Corporation v. Avery Cashion, III, 4th Cir. (2013)Document33 pagesFederal Deposit Insurance Corporation v. Avery Cashion, III, 4th Cir. (2013)Scribd Government DocsNo ratings yet

- 1921 Westerfield Banking Principles and Practice Vol 05 of 05Document308 pages1921 Westerfield Banking Principles and Practice Vol 05 of 05naturalvibesNo ratings yet

- Donors Capital Fund541934032 2007 048EED01SearchableDocument28 pagesDonors Capital Fund541934032 2007 048EED01Searchablecmf8926No ratings yet

- Donors Trust 2019 990Document113 pagesDonors Trust 2019 990jpeppardNo ratings yet

- You Are My Servant and I Have Chosen You: What It Means to Be Called, Chosen, Prepared and Ordained by God for MinistryFrom EverandYou Are My Servant and I Have Chosen You: What It Means to Be Called, Chosen, Prepared and Ordained by God for MinistryNo ratings yet

- Generally Accepted Auditing Standards A Complete Guide - 2020 EditionFrom EverandGenerally Accepted Auditing Standards A Complete Guide - 2020 EditionNo ratings yet

- Vaccination Centers On 11.10.2021Document4 pagesVaccination Centers On 11.10.2021Chanu On CTNo ratings yet

- Abuse of ProcessDocument31 pagesAbuse of Processkenemma6No ratings yet

- Introduction To Forensic Science Lecture 5 Forensic PathologyDocument89 pagesIntroduction To Forensic Science Lecture 5 Forensic PathologyBoţu Alexandru100% (4)

- Child Welfare League of America, Vol. 7, No. 1 (Summer 2008)Document15 pagesChild Welfare League of America, Vol. 7, No. 1 (Summer 2008)Tlecoz Huitzil100% (1)

- (Dragonlance Alt History) Age of The White HourglassDocument11 pages(Dragonlance Alt History) Age of The White HourglassWill HarperNo ratings yet

- Sloka Recitation: T L L B T A BDocument16 pagesSloka Recitation: T L L B T A Bleelakdd108No ratings yet

- Mock Bar Test 1Document9 pagesMock Bar Test 1Clark Vincent PonlaNo ratings yet

- Lolita PowerpointDocument7 pagesLolita Powerpointapi-374784915No ratings yet

- Guidelines For RemisiersDocument15 pagesGuidelines For Remisierssantosh.pw4230No ratings yet

- Past Tenses ExercisesDocument1 pagePast Tenses ExercisesChristina KaravidaNo ratings yet

- Basic Commerce Clause FrameworkDocument1 pageBasic Commerce Clause FrameworkBrat WurstNo ratings yet

- Reason For Popularity of Charlie ChaplinDocument4 pagesReason For Popularity of Charlie Chaplinmishra_ajay555No ratings yet

- All We NeedDocument1 pageAll We Needsheryl ambrocioNo ratings yet

- FILM CRITIQUEDocument14 pagesFILM CRITIQUERohan GeraNo ratings yet

- 06 - Chapter 1 - 2Document57 pages06 - Chapter 1 - 2RaviLahaneNo ratings yet

- Dreadful MutilationsDocument2 pagesDreadful Mutilationsstquinn864443No ratings yet

- Assignment: Grave and Sudden Provocation:An Analysis As Defence With Respect To Provisions of Indian Penal CodeDocument31 pagesAssignment: Grave and Sudden Provocation:An Analysis As Defence With Respect To Provisions of Indian Penal Codevinay sharmaNo ratings yet

- Aladdin Pitch FinishDocument10 pagesAladdin Pitch Finishapi-268965515No ratings yet

- Protocol Guide For Diplomatic Missions and Consular Posts January 2013Document101 pagesProtocol Guide For Diplomatic Missions and Consular Posts January 2013Nok Latana Siharaj100% (1)

- LVO 2020 40k Base Size Chart V1.0Document64 pagesLVO 2020 40k Base Size Chart V1.0JohnNo ratings yet

- Intermediate GW 12aDocument2 pagesIntermediate GW 12aKarol Nicole Huanca SanchoNo ratings yet

- Ra 442Document14 pagesRa 442Princess Melanie MelendezNo ratings yet

- LAWPBALLB254924rLawrPr - Joint and Independent TortfeasorsDocument3 pagesLAWPBALLB254924rLawrPr - Joint and Independent TortfeasorsSri Mugan100% (1)

- WFRP Warhammer Dark ElvesDocument19 pagesWFRP Warhammer Dark ElvesLance GoodthrustNo ratings yet

- mẫu hợp đồng dịch vụ bằng tiếng anhDocument5 pagesmẫu hợp đồng dịch vụ bằng tiếng anhJade Truong100% (1)

- Tarzi Akbar... Ideology of Modernization Iin AfghanistanDocument25 pagesTarzi Akbar... Ideology of Modernization Iin AfghanistanFayyaz AliNo ratings yet

- Juliette Binoche: French Actress' Career HighlightsDocument16 pagesJuliette Binoche: French Actress' Career HighlightsburkeNo ratings yet

- Oblicon QuestionsDocument1 pageOblicon QuestionsCaseylyn RonquilloNo ratings yet

- Juridical Capacity and Capacity To ActDocument4 pagesJuridical Capacity and Capacity To ActChap ChoyNo ratings yet

- LwOffz S-Z 2018 PDFDocument934 pagesLwOffz S-Z 2018 PDFJean Paul Sikkar100% (1)