You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Paper Wrigley gr.4Document9 pagesPaper Wrigley gr.4shaherikhkhanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Final Project of IB Part#2Document16 pagesFinal Project of IB Part#2Azka Aasim0% (1)

- Shareholders' Agreement outlines ownership and operationsDocument13 pagesShareholders' Agreement outlines ownership and operationsRoselle Alteria100% (1)

- Moody's - Petromindo Indonesia Coal Market Summit 20201019 (Confidential)Document23 pagesMoody's - Petromindo Indonesia Coal Market Summit 20201019 (Confidential)mza.arifinNo ratings yet

- Urban Convention Hotel Design PDFDocument153 pagesUrban Convention Hotel Design PDFCamilla Fernandez100% (1)

- B.Ethics (Part 2)Document110 pagesB.Ethics (Part 2)Hamza KianiNo ratings yet

- SEC Small Business Capital Formation 11.21Document36 pagesSEC Small Business Capital Formation 11.21CrowdfundInsiderNo ratings yet

- Sec Office Investor Advocate Report On Objectives Fy2015Document36 pagesSec Office Investor Advocate Report On Objectives Fy2015CrowdfundInsiderNo ratings yet

- SEC FY 2015 Congressional Justification and Performance Plan & FY 2013 Annual Performance ReportDocument192 pagesSEC FY 2015 Congressional Justification and Performance Plan & FY 2013 Annual Performance ReportVanessa SchoenthalerNo ratings yet

- U.S. Securities and Exchange Commission Strategic Plan - Fiscal Year 2014-2018Document60 pagesU.S. Securities and Exchange Commission Strategic Plan - Fiscal Year 2014-2018Vanessa SchoenthalerNo ratings yet

- Letter From Congressman Garrett To SEC Chair White Regarding The Definition of Accredited Investor (Oct. 2013)Document6 pagesLetter From Congressman Garrett To SEC Chair White Regarding The Definition of Accredited Investor (Oct. 2013)Vanessa SchoenthalerNo ratings yet

- From The On-Ramp To The Freeway - Refueling Job Creation and Growth by Reconnecting Investors With Small-Cap CompaniesDocument31 pagesFrom The On-Ramp To The Freeway - Refueling Job Creation and Growth by Reconnecting Investors With Small-Cap CompaniesVanessa SchoenthalerNo ratings yet

- SEC FY 2015 Congressional Justification and Performance Plan & FY 2013 Annual Performance ReportDocument192 pagesSEC FY 2015 Congressional Justification and Performance Plan & FY 2013 Annual Performance ReportVanessa SchoenthalerNo ratings yet

- Letter From Chair WhiteDocument6 pagesLetter From Chair WhiteSteve QuinlivanNo ratings yet

- Report On Review of Disclosure Requirements in Regulation S-KDocument106 pagesReport On Review of Disclosure Requirements in Regulation S-KCrowdfundInsiderNo ratings yet

- SEC 2014 Chief FOIA Officer ReportDocument17 pagesSEC 2014 Chief FOIA Officer ReportVanessa SchoenthalerNo ratings yet

- U.S. Securities and Exchange Commission - Fiscal Year 2013 Agency Financial ReportDocument156 pagesU.S. Securities and Exchange Commission - Fiscal Year 2013 Agency Financial ReportVanessa SchoenthalerNo ratings yet

- U.S. Securities and Exchange Commission - Strategic Plan 2014-2018 (Draft)Document42 pagesU.S. Securities and Exchange Commission - Strategic Plan 2014-2018 (Draft)Vanessa SchoenthalerNo ratings yet

- U.S. Securities and Exchange Commission - Fiscal Year 2013 Agency Financial ReportDocument156 pagesU.S. Securities and Exchange Commission - Fiscal Year 2013 Agency Financial ReportVanessa SchoenthalerNo ratings yet

- Capital Raising in The U.S.-an Analysis of Unregistered Offerings Using The Regulation D Exemption (2009-2012)Document22 pagesCapital Raising in The U.S.-an Analysis of Unregistered Offerings Using The Regulation D Exemption (2009-2012)Vanessa SchoenthalerNo ratings yet

- Alternative Criteria For Qualifying As An Accredited Investor Should Be ConsideredDocument69 pagesAlternative Criteria For Qualifying As An Accredited Investor Should Be ConsideredVanessa SchoenthalerNo ratings yet

- IOSCO-WFE Report - Cyber-Crime, Securities Markets and Systemic RiskDocument59 pagesIOSCO-WFE Report - Cyber-Crime, Securities Markets and Systemic RiskVanessa SchoenthalerNo ratings yet

- Report On Authority To Enforce Exchange Act Rule 12g5-1 and Subsection (B)Document35 pagesReport On Authority To Enforce Exchange Act Rule 12g5-1 and Subsection (B)Vanessa SchoenthalerNo ratings yet

- NASAA Legislative Agenda 113th CongressDocument17 pagesNASAA Legislative Agenda 113th CongressVanessa SchoenthalerNo ratings yet

- Letter From Congressman McHenry To SEC Chairman Schapiro Regarding JOBS Act (Nov. 2012)Document6 pagesLetter From Congressman McHenry To SEC Chairman Schapiro Regarding JOBS Act (Nov. 2012)Vanessa SchoenthalerNo ratings yet

- SEC-OIG Semiannual Report To Congress (Oct 2012 To Mar 2013)Document40 pagesSEC-OIG Semiannual Report To Congress (Oct 2012 To Mar 2013)Vanessa SchoenthalerNo ratings yet

- SEC Staff Review of Common Financial Reporting Issuers Facing Smaller Issuers (Dec. 2012)Document44 pagesSEC Staff Review of Common Financial Reporting Issuers Facing Smaller Issuers (Dec. 2012)Vanessa SchoenthalerNo ratings yet

- Third Report On The Implementation of SEC Organizational Reform RecommendationsDocument48 pagesThird Report On The Implementation of SEC Organizational Reform RecommendationsVanessa SchoenthalerNo ratings yet

- Report On Authority To Enforce Exchange Act Rule 12g5-1 and Subsection (B)Document35 pagesReport On Authority To Enforce Exchange Act Rule 12g5-1 and Subsection (B)Vanessa SchoenthalerNo ratings yet

- Evaluation of The SEC's Whistleblower ProgramDocument52 pagesEvaluation of The SEC's Whistleblower ProgramVanessa SchoenthalerNo ratings yet

- Letter From Congressman Garrett To SEC Chairman Schapiro Regarding JOBS Act (Nov. 2012)Document2 pagesLetter From Congressman Garrett To SEC Chairman Schapiro Regarding JOBS Act (Nov. 2012)Vanessa SchoenthalerNo ratings yet

- A Resource Guide To The U.S. Foreign Corrupt Practices ActDocument130 pagesA Resource Guide To The U.S. Foreign Corrupt Practices ActVanessa SchoenthalerNo ratings yet

- Response To Questions Posed by Commissioners Aguilar, Paredes and GallagherDocument98 pagesResponse To Questions Posed by Commissioners Aguilar, Paredes and GallagherVanessa SchoenthalerNo ratings yet

- SEC's Records Management PracticesDocument59 pagesSEC's Records Management PracticesVanessa SchoenthalerNo ratings yet

- SEC Report To Congress Credit Rating Standardization StudyDocument60 pagesSEC Report To Congress Credit Rating Standardization StudyVanessa SchoenthalerNo ratings yet

- Staff Summary Report On Examinations of Information Barriers - Broker-Dealer Practices Under Section 15 (G) of The Exchange ActDocument52 pagesStaff Summary Report On Examinations of Information Barriers - Broker-Dealer Practices Under Section 15 (G) of The Exchange ActVanessa SchoenthalerNo ratings yet

- Organisation Study On SHREE CEMENT BEAWARDocument89 pagesOrganisation Study On SHREE CEMENT BEAWARRajesh YadavNo ratings yet

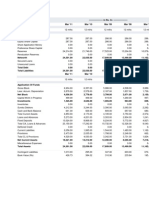

- Balance Sheet of InfosysDocument5 pagesBalance Sheet of InfosysLincy SubinNo ratings yet

- Legal Fundraising Donor List (For Public Distribution 082917) - FinalDocument3 pagesLegal Fundraising Donor List (For Public Distribution 082917) - FinalDarrenKrauseNo ratings yet

- CRM challenges in investment banking and financial marketsDocument16 pagesCRM challenges in investment banking and financial marketssarferazul_haqueNo ratings yet

- Capital StructureDocument7 pagesCapital StructurePrashanth MagadumNo ratings yet

- Practice Tests Partnership FormationDocument10 pagesPractice Tests Partnership FormationClaire RamosNo ratings yet

- Bank Company ActDocument16 pagesBank Company Actmd nazirul islam100% (2)

- BankingDocument236 pagesBankingamisha2562585No ratings yet

- © The Institute of Chartered Accountants of IndiaDocument56 pages© The Institute of Chartered Accountants of IndiaTejaNo ratings yet

- Chapter 3 Appendix ADocument16 pagesChapter 3 Appendix AOxana NeckagyNo ratings yet

- Group Assignment 2 - DraftDocument4 pagesGroup Assignment 2 - Draftsumeet kumarNo ratings yet

- SFM Nov 20Document20 pagesSFM Nov 20ritz meshNo ratings yet

- WhiteMonk HEG Equity Research ReportDocument15 pagesWhiteMonk HEG Equity Research ReportgirishamrNo ratings yet

- Municipal Real Property Asset Management:: An Application of Private Sector PracticesDocument8 pagesMunicipal Real Property Asset Management:: An Application of Private Sector PracticesIsgude GudeNo ratings yet

- National Income Accounting: Unit I PPT 2Document36 pagesNational Income Accounting: Unit I PPT 2Prateek TekchandaniNo ratings yet

- Ch10 TB RankinDocument6 pagesCh10 TB RankinAnton Vitali100% (1)

- Simply Syrup Incorporated A Maple Syrup Maker Reported The FollowingDocument1 pageSimply Syrup Incorporated A Maple Syrup Maker Reported The FollowingTaimour HassanNo ratings yet

- 01 Equity MethodDocument41 pages01 Equity MethodAngel Obligacion100% (1)

- General Re's Agreed Statement of FactsDocument14 pagesGeneral Re's Agreed Statement of FactsDealBookNo ratings yet

- Problem Solving Chapter 7Document3 pagesProblem Solving Chapter 7Kevin TW SalesNo ratings yet

- Fundamental #28 Have A Bias For Structure and Rebar.Document9 pagesFundamental #28 Have A Bias For Structure and Rebar.David FriedmanNo ratings yet

- Steamboat Springs City Council AgendaDocument265 pagesSteamboat Springs City Council AgendaScott FranzNo ratings yet

- 1st Mid Term Exam Fall 2015 AuditingDocument5 pages1st Mid Term Exam Fall 2015 AuditingSarahZeidatNo ratings yet