You might also like

- World Agricultural Production: Early Harvested Paraguay Soy Yields Are LowDocument26 pagesWorld Agricultural Production: Early Harvested Paraguay Soy Yields Are Lowapi-51572145No ratings yet

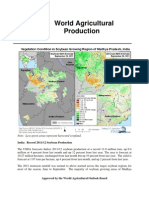

- World Agricultural Production: Foreign Agricultural Service Circular Series WAP 01-12 January 2012Document26 pagesWorld Agricultural Production: Foreign Agricultural Service Circular Series WAP 01-12 January 2012api-51572145No ratings yet

- World Agriculture Production-USDA Feb-2012Document25 pagesWorld Agriculture Production-USDA Feb-2012Dr-Khalid AbdullahNo ratings yet

- ArgentinaDocument6 pagesArgentinaapi-51572145No ratings yet

- Argentina Crops Feel The Heat, But Drought Fears OverblownDocument1 pageArgentina Crops Feel The Heat, But Drought Fears Overblownapi-51572145No ratings yet

- C C C CCCCCCCCCCDocument2 pagesC C C CCCCCCCCCCapi-51572145No ratings yet

- World Agricultural Production: Foreign Agricultural Service Circular Series WAP 12-11 December 2011Document26 pagesWorld Agricultural Production: Foreign Agricultural Service Circular Series WAP 12-11 December 2011api-51572145No ratings yet

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocument40 pagesWorld Agricultural Supply and Demand Estimates: United States Department of Agricultureapi-51572145No ratings yet

- World Agricultural Production: Southeast Asia Rice: Production Forecast Lower Owing To Widespread FloodingDocument27 pagesWorld Agricultural Production: Southeast Asia Rice: Production Forecast Lower Owing To Widespread Floodingapi-51572145No ratings yet

- SE ASIA: Widespread Flooding Impacts Regional Rice Production in 2011Document5 pagesSE ASIA: Widespread Flooding Impacts Regional Rice Production in 2011api-51572145No ratings yet

- World Agricultural Production: Kazakhstan Wheat: High Yield Prospects Following Beneficial RainfallDocument26 pagesWorld Agricultural Production: Kazakhstan Wheat: High Yield Prospects Following Beneficial Rainfallapi-51572145No ratings yet

- World Agricultural Supply and Demand Estimates: United States Department of AgricultureDocument40 pagesWorld Agricultural Supply and Demand Estimates: United States Department of Agricultureapi-51572145No ratings yet

- World Agricultural Production: Ukraine Wheat: Persistent Spring Dryness Reversed by Excessive July RainDocument24 pagesWorld Agricultural Production: Ukraine Wheat: Persistent Spring Dryness Reversed by Excessive July Rainapi-51572145No ratings yet

- UntitledDocument24 pagesUntitledapi-51572145No ratings yet

- UntitledDocument26 pagesUntitledapi-51572145No ratings yet

- UntitledDocument24 pagesUntitledapi-51572145No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Zlodjela Bolesnog UmaDocument106 pagesZlodjela Bolesnog UmaDZENAN SARACNo ratings yet

- Java Heritage Hotel ReportDocument11 pagesJava Heritage Hotel ReportنصرالحكمالغزلىNo ratings yet

- Luke 1.1-56 Intros & SummariesDocument8 pagesLuke 1.1-56 Intros & SummariesdkbusinessNo ratings yet

- LGGM Magallanes Floor PlanDocument1 pageLGGM Magallanes Floor PlanSheena Mae FullerosNo ratings yet

- Municipal Development Plan 1996 - 2001Document217 pagesMunicipal Development Plan 1996 - 2001TineNo ratings yet

- STS Learning Plan 1Document9 pagesSTS Learning Plan 1Lienol Pestañas Borreo0% (1)

- G.R. No. 113899. October 13, 1999. Great Pacific Life Assurance Corp., Petitioner, vs. Court of Appeals and Medarda V. Leuterio, RespondentsDocument12 pagesG.R. No. 113899. October 13, 1999. Great Pacific Life Assurance Corp., Petitioner, vs. Court of Appeals and Medarda V. Leuterio, RespondentsdanexrainierNo ratings yet

- HSEMS PresentationDocument21 pagesHSEMS PresentationVeera RagavanNo ratings yet

- The Peace Report: Walking Together For Peace (Issue No. 2)Document26 pagesThe Peace Report: Walking Together For Peace (Issue No. 2)Our MoveNo ratings yet

- SAHANA Disaster Management System and Tracking Disaster VictimsDocument30 pagesSAHANA Disaster Management System and Tracking Disaster VictimsAmalkrishnaNo ratings yet

- Braintrain: Summer Camp WorksheetDocument9 pagesBraintrain: Summer Camp WorksheetPadhmennNo ratings yet

- 30 Iconic Filipino SongsDocument9 pages30 Iconic Filipino SongsAlwynBaloCruzNo ratings yet

- Micro PPT FinalDocument39 pagesMicro PPT FinalRyan Christopher PascualNo ratings yet

- 4 - ISO - 19650 - Guidance - Part - A - The - Information - Management - Function - and - Resources - Edition 3Document16 pages4 - ISO - 19650 - Guidance - Part - A - The - Information - Management - Function - and - Resources - Edition 3Rahul Tidke - ExcelizeNo ratings yet

- Crossen For Sale On Market - 05.23.2019Document26 pagesCrossen For Sale On Market - 05.23.2019Article LinksNo ratings yet

- Um Tagum CollegeDocument12 pagesUm Tagum Collegeneil0522No ratings yet

- Suez CanalDocument7 pagesSuez CanalUlaş GüllenoğluNo ratings yet

- The Second Oracle at DelphiDocument14 pagesThe Second Oracle at Delphiapi-302698865No ratings yet

- EEE Assignment 3Document8 pagesEEE Assignment 3shirleyNo ratings yet

- Outline 2018: Cultivating Professionals With Knowledge and Humanity, Thereby Contributing To People S Well-BeingDocument34 pagesOutline 2018: Cultivating Professionals With Knowledge and Humanity, Thereby Contributing To People S Well-BeingDd KNo ratings yet

- PRC AUD Prelim Wit Ans KeyDocument10 pagesPRC AUD Prelim Wit Ans KeyJeanette FormenteraNo ratings yet

- PMP Mock Exams 1, 200 Q&ADocument29 pagesPMP Mock Exams 1, 200 Q&Asfdfdf dfdfdf100% (1)

- Puyat vs. Arco Amusement Co (Gaspar)Document2 pagesPuyat vs. Arco Amusement Co (Gaspar)Maria Angela GasparNo ratings yet

- Online Learning Can Replace Classroom TeachingsDocument7 pagesOnline Learning Can Replace Classroom TeachingsSonam TobgayNo ratings yet

- Historical Allusions in The Book of Habakkuk: Aron PinkerDocument10 pagesHistorical Allusions in The Book of Habakkuk: Aron Pinkerstefa74No ratings yet

- View of Hebrews Ethan SmithDocument295 pagesView of Hebrews Ethan SmithOlvin Steve Rosales MenjivarNo ratings yet

- Deped Order 36Document22 pagesDeped Order 36Michael Green100% (1)

- Case Story: NZS SCM 930 - TransportationDocument8 pagesCase Story: NZS SCM 930 - TransportationJoão Marcelo de CarvalhoNo ratings yet

- Lesson Plan - ClimatechangeDocument7 pagesLesson Plan - ClimatechangeLikisha RaffyNo ratings yet

- OneSumX IFRS9 ECL Impairments Produc SheetDocument2 pagesOneSumX IFRS9 ECL Impairments Produc SheetRaju KaliperumalNo ratings yet