You might also like

- How to Trade Gold: Gold Trading Strategies That WorkFrom EverandHow to Trade Gold: Gold Trading Strategies That WorkRating: 1 out of 5 stars1/5 (1)

- AHA Article - Review of TradesDocument6 pagesAHA Article - Review of TradesMaheswarReddy SathelaNo ratings yet

- Gold Vs Gold StocksDocument4 pagesGold Vs Gold StocksZerohedgeNo ratings yet

- Silver's Subtle Indication PDFDocument13 pagesSilver's Subtle Indication PDFantoniogoldmanhNo ratings yet

- James Turk of GLDDocument2 pagesJames Turk of GLDcap0jayNo ratings yet

- Gold Stock Analyst FreeDocument3 pagesGold Stock Analyst FreeNikkiNo ratings yet

- Curtis Hesler - It's No Time To Ditch Gold AnalysisDocument3 pagesCurtis Hesler - It's No Time To Ditch Gold AnalysisDraženSNo ratings yet

- Stock Market Returns and The Price of Gold: BstractDocument26 pagesStock Market Returns and The Price of Gold: BstractAnonymous rOv67RNo ratings yet

- Gold Furutes PDFDocument9 pagesGold Furutes PDFAnoop KumarNo ratings yet

- Commodity Trading-Mutual FundsDocument17 pagesCommodity Trading-Mutual Fundsapi-3832523No ratings yet

- The 5 Best Ways To Invest in GoldDocument3 pagesThe 5 Best Ways To Invest in GoldCarlos Alberto GarayNo ratings yet

- Delta Global Partners Research:: Chart I: Is GOLD The New "United Future World Currency"?Document4 pagesDelta Global Partners Research:: Chart I: Is GOLD The New "United Future World Currency"?devnevNo ratings yet

- The Investment Case For Junior Mining Companies: Part I: Technical ViewDocument9 pagesThe Investment Case For Junior Mining Companies: Part I: Technical ViewLuisMendiolaNo ratings yet

- Master Thesis Gold PriceDocument8 pagesMaster Thesis Gold PriceCustomPaperCanada100% (2)

- 1 - Contract Specifications - Quanto Futures - MetalsDocument7 pages1 - Contract Specifications - Quanto Futures - MetalsQuant_GeekNo ratings yet

- How To Trade GoldDocument10 pagesHow To Trade GoldSadiq AbdulazeezNo ratings yet

- Gold Price Fluctuation Research PaperDocument4 pagesGold Price Fluctuation Research Papergz91rnat100% (1)

- Major Divergence in Gold Asset Classes January 2012Document7 pagesMajor Divergence in Gold Asset Classes January 2012Peter L. BrandtNo ratings yet

- THE TREND READER - GOLD STOCKS ARE PATIENTLY AWAITING THEIR TURN - Olaf SztabaDocument3 pagesTHE TREND READER - GOLD STOCKS ARE PATIENTLY AWAITING THEIR TURN - Olaf SztabaChester Yukon GoldNo ratings yet

- A Comparative Study On Investing in Gold Related AssetsDocument5 pagesA Comparative Study On Investing in Gold Related AssetsLakskmi Priya M CNo ratings yet

- Aileron Market Balance: Issue 21Document8 pagesAileron Market Balance: Issue 21Dan ShyNo ratings yet

- Why Invest in GoldDocument7 pagesWhy Invest in GoldSaket AgarwalNo ratings yet

- How to Invest in Gold & Silver: A Complete Guide With a Focus on Mining StocksFrom EverandHow to Invest in Gold & Silver: A Complete Guide With a Focus on Mining StocksRating: 5 out of 5 stars5/5 (2)

- Commodity Trading: Acm Gold Mock Trading Term ReportDocument10 pagesCommodity Trading: Acm Gold Mock Trading Term ReportTalhaSirajNo ratings yet

- 55 Gold FeverDocument5 pages55 Gold FeverACasey101No ratings yet

- K-Ratio - Gold Timing by KaeppelDocument4 pagesK-Ratio - Gold Timing by Kaeppelstummel6636No ratings yet

- A Comparative Study On Investing in Gold Related Assets: January 2013Document6 pagesA Comparative Study On Investing in Gold Related Assets: January 2013REDDYNo ratings yet

- Weekly Options Watch Trade Ideas JWN, NVDA, CSCO, GWWDocument12 pagesWeekly Options Watch Trade Ideas JWN, NVDA, CSCO, GWWgneymanNo ratings yet

- What Are Gold Futures?: Why Invest in Gold?Document3 pagesWhat Are Gold Futures?: Why Invest in Gold?Tariq HameedNo ratings yet

- Guide To Investing in Gold & SilverDocument12 pagesGuide To Investing in Gold & Silveravoman123100% (1)

- Hedging at Its Most Basic: Ian LevyDocument3 pagesHedging at Its Most Basic: Ian Levyivanuska90100% (1)

- Gold Ebook (6490)Document24 pagesGold Ebook (6490)Bukelwa MabuyaNo ratings yet

- Tutorials in Applied Technical Analysis: Managing ExitsDocument15 pagesTutorials in Applied Technical Analysis: Managing ExitsPinky BhagwatNo ratings yet

- 7-31-12 Breakout in Gold?Document3 pages7-31-12 Breakout in Gold?The Gold SpeculatorNo ratings yet

- Beginner's Guide To FuturesDocument15 pagesBeginner's Guide To FuturesAnupam BhardwajNo ratings yet

- AWN ThePerfectGoldPortfolioDocument8 pagesAWN ThePerfectGoldPortfolioCraig CannonNo ratings yet

- FREE, 9-17-22 Weekend Metals ReportDocument16 pagesFREE, 9-17-22 Weekend Metals ReportMarco BourdonNo ratings yet

- Investing in Gold 172Document4 pagesInvesting in Gold 172drkwngNo ratings yet

- Gold DerivativesDocument19 pagesGold DerivativesvinusachdevNo ratings yet

- Contango vs. Normal BackwardationDocument2 pagesContango vs. Normal BackwardationmksscribdNo ratings yet

- Aileron Market Balance: Issue 18Document6 pagesAileron Market Balance: Issue 18Dan ShyNo ratings yet

- Great Gold Silver Ride 2012Document26 pagesGreat Gold Silver Ride 2012shamikbhoseNo ratings yet

- Double Calendar Spreads, How Can We Use Them?Document6 pagesDouble Calendar Spreads, How Can We Use Them?John Klein120% (2)

- Tactical Playbook 10222012 - IdeafarmDocument28 pagesTactical Playbook 10222012 - IdeafarmmaikubNo ratings yet

- Literature Review Gold InvestmentDocument8 pagesLiterature Review Gold Investmentfvg4bacd100% (1)

- The Futures Market The Futures Market: Introduction and and Mechanics MechanicsDocument13 pagesThe Futures Market The Futures Market: Introduction and and Mechanics MechanicsCcudi ARslanNo ratings yet

- CNBC Dec4 Shamik Gold InterviewDocument4 pagesCNBC Dec4 Shamik Gold InterviewshamikbhoseNo ratings yet

- Commodity PrimerDocument6 pagesCommodity PrimerSammus LeeNo ratings yet

- Spot Rates: Chapter 13 - The Foreign-Exchange MarketDocument8 pagesSpot Rates: Chapter 13 - The Foreign-Exchange Marketzeebee17No ratings yet

- Daily Metals Newsletter - 01-12-16Document1 pageDaily Metals Newsletter - 01-12-16Jaeson Rian ParsonsNo ratings yet

- SPDR Gold ETFDocument2 pagesSPDR Gold ETFpicchu144No ratings yet

- Answers HBS Case Goldman Sachs Nikkei Put WarrentDocument8 pagesAnswers HBS Case Goldman Sachs Nikkei Put WarrentSander Chewy67% (3)

- Hedge (Finance) : What Does Hedge Mean?Document4 pagesHedge (Finance) : What Does Hedge Mean?kkrathodNo ratings yet

- In GOLD We TRUST 2013 - Incrementum Extended VersionDocument54 pagesIn GOLD We TRUST 2013 - Incrementum Extended VersionZerohedgeNo ratings yet

- Article Summary On Gold or Gold EtfDocument6 pagesArticle Summary On Gold or Gold EtfarushpratyushNo ratings yet

- DerivativesDocument130 pagesDerivativesPavithran ChandarNo ratings yet

- Banking BriefDocument449 pagesBanking Briefprasadkh90No ratings yet

- Test Bank For Fundamentals of Investing 14th by SmartDocument25 pagesTest Bank For Fundamentals of Investing 14th by SmartPatrick Kavanaugh100% (40)

- Performance Appraisal of Gold ETFS in India: Finance ManagementDocument4 pagesPerformance Appraisal of Gold ETFS in India: Finance ManagementpatelaxayNo ratings yet

- CISI Mock Exam Questionnaires (Consolidated)Document17 pagesCISI Mock Exam Questionnaires (Consolidated)Jerome GaliciaNo ratings yet

- Eric Parnell Getting Defensive With Utilities, Consumer Staples, Precious Metals, TIPS, Agency MBS - SeekinDocument16 pagesEric Parnell Getting Defensive With Utilities, Consumer Staples, Precious Metals, TIPS, Agency MBS - Seekinambasyapare1No ratings yet

- BUSS 207 Quiz 3 - SolutionDocument3 pagesBUSS 207 Quiz 3 - Solutiontom dussekNo ratings yet

- A Study On The Impact of Volatility in Gold Price On The CustomersDocument12 pagesA Study On The Impact of Volatility in Gold Price On The CustomersVishwas DeveeraNo ratings yet

- INDEX TradingDocument221 pagesINDEX TradingREVANSIDDHA83% (6)

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- Anurag PIS - Week 3 ReviewDocument4 pagesAnurag PIS - Week 3 ReviewANURAG JENANo ratings yet

- BlackRock 2023 Investor DayDocument138 pagesBlackRock 2023 Investor DayDaniele Pronestì100% (1)

- Personal Finance BulletinDocument7 pagesPersonal Finance Bulletinfarazalam08No ratings yet

- IDX Monthly Mar 2016Document108 pagesIDX Monthly Mar 2016miieko50% (2)

- Is Sovereign Gold Bond Is Better Than Other Gold Investment?Document5 pagesIs Sovereign Gold Bond Is Better Than Other Gold Investment?MohmmedKhayyumNo ratings yet

- Informe de JP Morgan Sobre Las Elecciones Regionales en Colombia 2023Document6 pagesInforme de JP Morgan Sobre Las Elecciones Regionales en Colombia 2023economiaparalapipolNo ratings yet

- Description: S&P Biotechnology Select Industry IndexDocument7 pagesDescription: S&P Biotechnology Select Industry IndexRandom LifeNo ratings yet

- Dimensional Fund Advisors 2002 Case SolutionDocument10 pagesDimensional Fund Advisors 2002 Case SolutionRohit Kumar80% (5)

- Indonesia, 8.50% 12oct2035, USDDocument1 pageIndonesia, 8.50% 12oct2035, USDFreddy Daniel NababanNo ratings yet

- ARGA Investment Management L.P. About The FirmDocument1 pageARGA Investment Management L.P. About The FirmkunalNo ratings yet

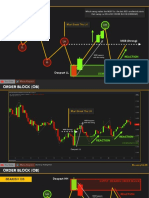

- OB - Order BlockDocument25 pagesOB - Order BlockParaschiv Bogdan100% (11)

- Comparison of Mutual Funds With Other Investment OptionsDocument56 pagesComparison of Mutual Funds With Other Investment OptionsDiiivya86% (14)

- Gold InvestmentDocument4 pagesGold InvestmentvinitclairNo ratings yet

- Equity QUIZDocument8 pagesEquity QUIZSaYeD SeeDooNo ratings yet

- Seven Deadly Trading Sins 7 Trading SinsDocument61 pagesSeven Deadly Trading Sins 7 Trading SinsJarvis Angelo DaquiganNo ratings yet

- September 30, 2021, Quarter-To-Date Statement: Do Not Use For Account Transactions PO BOX 3009 MONROE, WI 53566-8309Document10 pagesSeptember 30, 2021, Quarter-To-Date Statement: Do Not Use For Account Transactions PO BOX 3009 MONROE, WI 53566-8309vagabondstar100% (1)

- Top Chart Traders - Insider Tips - Best High Performance Indicators PDFDocument133 pagesTop Chart Traders - Insider Tips - Best High Performance Indicators PDFlior199No ratings yet

- Trading QuestionsDocument11 pagesTrading QuestionsViacheslav BaykovNo ratings yet

- ARK Space Exploration & Innovation ETF: Holdings Data - ARKXDocument2 pagesARK Space Exploration & Innovation ETF: Holdings Data - ARKXqwertyNo ratings yet

- Reconstitution: Russell 3000 Index - AdditionsDocument10 pagesReconstitution: Russell 3000 Index - AdditionsepbeaverNo ratings yet

- Three-Fund Portfolio - BoogleheadsDocument11 pagesThree-Fund Portfolio - BoogleheadsMRT10100% (4)