You might also like

- Entrepreneurship and RecessionDocument48 pagesEntrepreneurship and RecessionWestley GomezNo ratings yet

- Unemployment: Demi Corrigan and Kerry MelloDocument21 pagesUnemployment: Demi Corrigan and Kerry MelloDemi CorriganNo ratings yet

- Weekly Market Commentary 10-24-11Document5 pagesWeekly Market Commentary 10-24-11monarchadvisorygroupNo ratings yet

- Uk Productivity PuzzleDocument4 pagesUk Productivity Puzzleapi-53255207No ratings yet

- Weekly Economic Commentary 10-10-11Document8 pagesWeekly Economic Commentary 10-10-11monarchadvisorygroupNo ratings yet

- Weekly Economic Commentary 11-5-2012Document5 pagesWeekly Economic Commentary 11-5-2012monarchadvisorygroupNo ratings yet

- Weekly Economic Commentar 10-17-11Document4 pagesWeekly Economic Commentar 10-17-11monarchadvisorygroupNo ratings yet

- Newton KuNe Neg 01 - Blue Valley Southwest OctasDocument27 pagesNewton KuNe Neg 01 - Blue Valley Southwest OctasEmronNo ratings yet

- Economist Insights 2012Document2 pagesEconomist Insights 2012buyanalystlondonNo ratings yet

- JC 4Document31 pagesJC 4Yiha FenteNo ratings yet

- Ferreira 1994Document38 pagesFerreira 1994StegabNo ratings yet

- Business Cycles and Economic Indicators: Journal, Jan 22, 1993, C1) : "There Are Two Kinds of Forecasters: Those Who Don'tDocument3 pagesBusiness Cycles and Economic Indicators: Journal, Jan 22, 1993, C1) : "There Are Two Kinds of Forecasters: Those Who Don'tbruhaspati1210No ratings yet

- Yellen Speech 7.10Document15 pagesYellen Speech 7.10ZerohedgeNo ratings yet

- The Small Business Sector in Recent RecoveriesDocument29 pagesThe Small Business Sector in Recent RecoveriesOlaru LorenaNo ratings yet

- Other Aging America Dominance Older Firms Hathaway LitanDocument18 pagesOther Aging America Dominance Older Firms Hathaway Litanrichardck61No ratings yet

- Luigi PistaferriDocument63 pagesLuigi PistaferriTBP_Think_TankNo ratings yet

- Finance vs. Wal-Mart: Why Are Financial Services So Expensive?Document14 pagesFinance vs. Wal-Mart: Why Are Financial Services So Expensive?ritvik.singh2827No ratings yet

- Philippon (2008) Wages and Human Capital in The U.S. Financial IndustryDocument60 pagesPhilippon (2008) Wages and Human Capital in The U.S. Financial IndustryunendedNo ratings yet

- Bernanke 20121120 ADocument16 pagesBernanke 20121120 Atax9654No ratings yet

- Low Interest RatesDocument2 pagesLow Interest RatescaitlynharveyNo ratings yet

- Weekly Market Commentary 11-7-11Document6 pagesWeekly Market Commentary 11-7-11monarchadvisorygroupNo ratings yet

- Paul Craig Roberts: Economy US ViewpointsDocument3 pagesPaul Craig Roberts: Economy US Viewpointskwintencirkel3715No ratings yet

- Module 2-Case Economic Indicators BUS305 - Competitive Analysis and Business Cycles August 18, 2012Document13 pagesModule 2-Case Economic Indicators BUS305 - Competitive Analysis and Business Cycles August 18, 2012cnrose4229No ratings yet

- Weekly Economic Commentary 11-3-11Document7 pagesWeekly Economic Commentary 11-3-11monarchadvisorygroupNo ratings yet

- StPaulCentral UlBa Aff 03 - Iowa Caucus Round 2Document32 pagesStPaulCentral UlBa Aff 03 - Iowa Caucus Round 2EmronNo ratings yet

- Federal Reserve Bank of New York Staff ReportsDocument35 pagesFederal Reserve Bank of New York Staff ReportsVlasti MilanovicNo ratings yet

- Hunger Ford, TL - Business Investment and Employment Tax Incentives To Stimulate The EconomyDocument19 pagesHunger Ford, TL - Business Investment and Employment Tax Incentives To Stimulate The EconomytfjieldNo ratings yet

- Reader Article 5Document7 pagesReader Article 5lullermanNo ratings yet

- The Business Cycle in A Changing Economy: Conceptualization, Measurement, DatingDocument11 pagesThe Business Cycle in A Changing Economy: Conceptualization, Measurement, DatingGuanino RoroNo ratings yet

- Weekly Economic Commentary 02-08-12Document4 pagesWeekly Economic Commentary 02-08-12monarchadvisorygroupNo ratings yet

- Is The Economy Turning Around?Document4 pagesIs The Economy Turning Around?Rana WaqasNo ratings yet

- LIN, Ken-Hou DeVEY, Donald. Financialization and U.S. Income Inequality, 1970-2008Document46 pagesLIN, Ken-Hou DeVEY, Donald. Financialization and U.S. Income Inequality, 1970-2008Henrique SantosNo ratings yet

- Glenn Stevens: The Economic Outlook in 2002: The US Business CycleDocument8 pagesGlenn Stevens: The Economic Outlook in 2002: The US Business CycleFlaviub23No ratings yet

- Debt Be Not ProudDocument11 pagesDebt Be Not Proudsilver999No ratings yet

- Weekly Economic Commentary 9/10/2012Document4 pagesWeekly Economic Commentary 9/10/2012monarchadvisorygroupNo ratings yet

- Weekly Economic Commentary 07-11-2011Document4 pagesWeekly Economic Commentary 07-11-2011Jeremy A. MillerNo ratings yet

- Shadow Economy and Unemployment Rate in USA: Is There A Structural Relationship? An Empirical AnalysisDocument20 pagesShadow Economy and Unemployment Rate in USA: Is There A Structural Relationship? An Empirical AnalysismsjonahNo ratings yet

- Looking Behind The Aggregates: A Reply To "Facts and Myths About The Financial Crisis of 2008"Document18 pagesLooking Behind The Aggregates: A Reply To "Facts and Myths About The Financial Crisis of 2008"StonerNo ratings yet

- The US Stock Market Wants To Go Up Part II 03-31-20111 - by Economist Mike AstrachanDocument11 pagesThe US Stock Market Wants To Go Up Part II 03-31-20111 - by Economist Mike AstrachanShlomiNo ratings yet

- Economic Growth in China: Productivity and Policy Editorial IntroductionDocument3 pagesEconomic Growth in China: Productivity and Policy Editorial IntroductionBianca AlexandraNo ratings yet

- Final Thesis AmbendanoDocument30 pagesFinal Thesis AmbendanoMylin Garciano AngcogNo ratings yet

- The Outlook For Recovery in The U.S. EconomyDocument13 pagesThe Outlook For Recovery in The U.S. EconomyZerohedgeNo ratings yet

- Intangible Capital and Us Economic GrowthDocument52 pagesIntangible Capital and Us Economic GrowthKári FinnssonNo ratings yet

- Economy Results Due To Faulty Legal System and Unjust State of Georgia Convictions On All 5 Counts of Banks' Cases of Innocent Srinivas VaddeDocument1,553 pagesEconomy Results Due To Faulty Legal System and Unjust State of Georgia Convictions On All 5 Counts of Banks' Cases of Innocent Srinivas VaddesvvpassNo ratings yet

- Weekly Economic Commentary 4-13-12Document8 pagesWeekly Economic Commentary 4-13-12monarchadvisorygroupNo ratings yet

- Weekly Economic Commentary 11/112013Document5 pagesWeekly Economic Commentary 11/112013monarchadvisorygroupNo ratings yet

- 5 MythsDocument6 pages5 MythsParvesh KhuranaNo ratings yet

- Cheney's Patterns of Industrial GrowthDocument14 pagesCheney's Patterns of Industrial GrowthProf B Sudhakar Reddy100% (1)

- Sept Jobs SummaryDocument3 pagesSept Jobs SummarySanjeev88No ratings yet

- Declining Business Dynamism in The United States A Look at States and MetrosDocument8 pagesDeclining Business Dynamism in The United States A Look at States and MetrosBrookings InstitutionNo ratings yet

- Highest-Employing Industries in 2011Document6 pagesHighest-Employing Industries in 2011sandra_lenoisNo ratings yet

- Macro Chap 01Document4 pagesMacro Chap 01saurabhsaurs100% (2)

- Hoisington Q4Document6 pagesHoisington Q4ZerohedgeNo ratings yet

- Revenue Status Report FY 2011-2012 - General Fund 20111231Document19 pagesRevenue Status Report FY 2011-2012 - General Fund 20111231Infosys GriffinNo ratings yet

- Beware of The "End Contractualization!" Battle CryDocument32 pagesBeware of The "End Contractualization!" Battle CryJay TeeNo ratings yet

- Monetary Morphine and The Job MarketDocument3 pagesMonetary Morphine and The Job MarketPrieto PabloNo ratings yet

- Powell 20210210 ADocument20 pagesPowell 20210210 AZerohedgeNo ratings yet

- 2012: THE WEAK ECONOMY AND HOW TO DEAL WITH IT TO EMPOWER THE CITIZENSFrom Everand2012: THE WEAK ECONOMY AND HOW TO DEAL WITH IT TO EMPOWER THE CITIZENSNo ratings yet

- TBP Conf Oct 2012Document27 pagesTBP Conf Oct 2012annawitkowski88No ratings yet

- People V JP Morgan ComplaintDocument31 pagesPeople V JP Morgan ComplaintJames EdwardsNo ratings yet

- Single SlideDocument1 pageSingle Slideannawitkowski88No ratings yet

- Research Division: Federal Reserve Bank of St. LouisDocument43 pagesResearch Division: Federal Reserve Bank of St. Louisannawitkowski88No ratings yet

- SSRN Id2023011Document54 pagesSSRN Id2023011sterkejanNo ratings yet

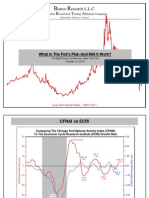

- Ianco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?Document44 pagesIanco Esearch L.L.C. A R T A: What Is The Fed's Plan and Will It Work?annawitkowski88No ratings yet

- Richmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative AssessmentDocument11 pagesRichmond Fed Research Digest: Frictional Wage Dispersion in Search Models: A Quantitative Assessmentannawitkowski88No ratings yet

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 pagesIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88No ratings yet

- Exhibit 15 - Whistleblower Affidavit (Redacted)Document11 pagesExhibit 15 - Whistleblower Affidavit (Redacted)annawitkowski88No ratings yet

- Fed SideDocument1 pageFed Sideannawitkowski88No ratings yet

- Income, Poverty, and Health Insurance Coverage in The United States: 2011Document89 pagesIncome, Poverty, and Health Insurance Coverage in The United States: 2011annawitkowski88No ratings yet

- Taxes and The EconomyDocument23 pagesTaxes and The Economychristian_trejbal100% (1)

- The Boom and Bust of U.S. Housing Prices From Various Geographic PerspectivesDocument29 pagesThe Boom and Bust of U.S. Housing Prices From Various Geographic Perspectivesannawitkowski88No ratings yet

- Woodford Rules Jackson Hole WyomingDocument97 pagesWoodford Rules Jackson Hole WyominglatecircleNo ratings yet

- Finance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.CDocument36 pagesFinance and Economics Discussion Series Divisions of Research & Statistics and Monetary Affairs Federal Reserve Board, Washington, D.Cannawitkowski88No ratings yet

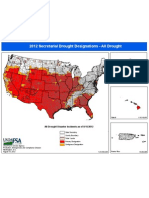

- Usda Drought Fast Track Designations 081512Document1 pageUsda Drought Fast Track Designations 081512annawitkowski88No ratings yet

- Amount of Casien in Diff Samples of Milk (U)Document15 pagesAmount of Casien in Diff Samples of Milk (U)VijayNo ratings yet

- QuexBook TutorialDocument14 pagesQuexBook TutorialJeffrey FarillasNo ratings yet

- Hướng Dẫn Chấm: Ngày thi: 27 tháng 7 năm 2019 Thời gian làm bài: 180 phút (không kể thời gian giao đề) HDC gồm có 4 trangDocument4 pagesHướng Dẫn Chấm: Ngày thi: 27 tháng 7 năm 2019 Thời gian làm bài: 180 phút (không kể thời gian giao đề) HDC gồm có 4 trangHưng Quân VõNo ratings yet

- Continue Practice Exam Test Questions Part 1 of The SeriesDocument7 pagesContinue Practice Exam Test Questions Part 1 of The SeriesKenn Earl Bringino VillanuevaNo ratings yet

- Recitation Math 001 - Term 221 (26166)Document36 pagesRecitation Math 001 - Term 221 (26166)Ma NaNo ratings yet

- An Evaluation of MGNREGA in SikkimDocument7 pagesAn Evaluation of MGNREGA in SikkimBittu SubbaNo ratings yet

- Listen and Arrange The Sentences Based On What You Have Heard!Document3 pagesListen and Arrange The Sentences Based On What You Have Heard!Dewi Hauri Naura HaufanhazzaNo ratings yet

- LSCM Course OutlineDocument13 pagesLSCM Course OutlineDeep SachetiNo ratings yet

- Neonatal Mortality - A Community ApproachDocument13 pagesNeonatal Mortality - A Community ApproachJalam Singh RathoreNo ratings yet

- Development Developmental Biology EmbryologyDocument6 pagesDevelopment Developmental Biology EmbryologyBiju ThomasNo ratings yet

- Fundamentals of Public Health ManagementDocument3 pagesFundamentals of Public Health ManagementHPMA globalNo ratings yet

- Chapter 13 (Automatic Transmission)Document26 pagesChapter 13 (Automatic Transmission)ZIBA KHADIBINo ratings yet

- The cardioprotective effect of astaxanthin against isoprenaline-induced myocardial injury in rats: involvement of TLR4/NF-κB signaling pathwayDocument7 pagesThe cardioprotective effect of astaxanthin against isoprenaline-induced myocardial injury in rats: involvement of TLR4/NF-κB signaling pathwayMennatallah AliNo ratings yet

- Promotion-Mix (: Tools For IMC)Document11 pagesPromotion-Mix (: Tools For IMC)Mehul RasadiyaNo ratings yet

- FuzzingBluetooth Paul ShenDocument8 pagesFuzzingBluetooth Paul Shen许昆No ratings yet

- Workbook Group TheoryDocument62 pagesWorkbook Group TheoryLi NguyenNo ratings yet

- Lecture 14 Direct Digital ManufacturingDocument27 pagesLecture 14 Direct Digital Manufacturingshanur begulaji0% (1)

- Out PDFDocument211 pagesOut PDFAbraham RojasNo ratings yet

- Mechanical Production Engineer Samphhhhhle ResumeDocument2 pagesMechanical Production Engineer Samphhhhhle ResumeAnirban MazumdarNo ratings yet

- 40 People vs. Rafanan, Jr.Document10 pages40 People vs. Rafanan, Jr.Simeon TutaanNo ratings yet

- The Influence of Irish Monks On Merovingian Diocesan Organization-Robbins BittermannDocument15 pagesThe Influence of Irish Monks On Merovingian Diocesan Organization-Robbins BittermanngeorgiescuNo ratings yet

- Baseline Scheduling Basics - Part-1Document48 pagesBaseline Scheduling Basics - Part-1Perwaiz100% (1)

- In Flight Fuel Management and Declaring MINIMUM MAYDAY FUEL-1.0Document21 pagesIn Flight Fuel Management and Declaring MINIMUM MAYDAY FUEL-1.0dahiya1988No ratings yet

- EqualLogic Release and Support Policy v25Document7 pagesEqualLogic Release and Support Policy v25du2efsNo ratings yet

- Physics Education Thesis TopicsDocument4 pagesPhysics Education Thesis TopicsPaperWriterServicesCanada100% (2)

- ML Ass 2Document6 pagesML Ass 2Santhosh Kumar PNo ratings yet

- Deep Hole Drilling Tools: BotekDocument32 pagesDeep Hole Drilling Tools: BotekDANIEL MANRIQUEZ FAVILANo ratings yet

- Book 1518450482Document14 pagesBook 1518450482rajer13No ratings yet

- Cambridge IGCSE™: Information and Communication Technology 0417/13 May/June 2022Document15 pagesCambridge IGCSE™: Information and Communication Technology 0417/13 May/June 2022ilovefettuccineNo ratings yet

- Design of Combinational Circuit For Code ConversionDocument5 pagesDesign of Combinational Circuit For Code ConversionMani BharathiNo ratings yet