You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

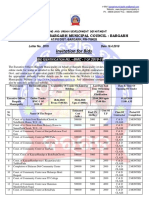

- Invitation For Bids: Office of The Bargarh Municipal Council: BargarhDocument3 pagesInvitation For Bids: Office of The Bargarh Municipal Council: BargarhANJANI KUMAR SRIWASNo ratings yet

- Test Series: August, 2018 Mock Test Paper - 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws & International TaxationDocument6 pagesTest Series: August, 2018 Mock Test Paper - 1 Final (New) Course: Group - Ii Paper - 7: Direct Tax Laws & International TaxationRobinxyNo ratings yet

- Cta Ifc RBDocument172 pagesCta Ifc RBMaria VelascoNo ratings yet

- Bank Letter For Fixed Deposit - SampleDocument1 pageBank Letter For Fixed Deposit - Sampletvaprasad75% (4)

- Cash Management SystemDocument65 pagesCash Management SystemmsdNo ratings yet

- Your Accounts at A Glance: Your Balances On 22 Feb 2022Document4 pagesYour Accounts at A Glance: Your Balances On 22 Feb 2022mohamed elmakhzniNo ratings yet

- UCO BankDocument128 pagesUCO BankRitesh TyagiNo ratings yet

- Case Study On Bear StearnsDocument13 pagesCase Study On Bear StearnsBrayanJosueReyesHerreraNo ratings yet

- Vcnotes 05 09 2017Document72 pagesVcnotes 05 09 2017MohammadRahemanNo ratings yet

- Section 14 Unab Rid Dged Written VersionDocument17 pagesSection 14 Unab Rid Dged Written VersionPrashant TrivediNo ratings yet

- Account No. Account Name Account TypeDocument2 pagesAccount No. Account Name Account Typesc9296No ratings yet

- 75 - Industrial All RiskDocument28 pages75 - Industrial All RiskAMIT GUPTANo ratings yet

- Memorandum of UnderstandingDocument2 pagesMemorandum of UnderstandingFantania BerryNo ratings yet

- Deposist AccountDocument6 pagesDeposist AccountwaheedarifNo ratings yet

- Saura Import and Export Co. vs. DBP, 27 April 1972Document3 pagesSaura Import and Export Co. vs. DBP, 27 April 1972Anjela ChingNo ratings yet

- LIC-IRDA Exam-1Document10 pagesLIC-IRDA Exam-1umesh50% (2)

- P 1Document8 pagesP 1aneilrosethNo ratings yet

- Finding A Bank For The BrennansDocument4 pagesFinding A Bank For The Brennansrichard100% (1)

- Questions and AnswersDocument20 pagesQuestions and AnswersJi YuNo ratings yet

- Account Closure Request Form Yes BankDocument1 pageAccount Closure Request Form Yes BankRadheShyam0% (1)

- Probability of RuinDocument84 pagesProbability of RuinDaniel QuinnNo ratings yet

- Credit Insurance PPT BasicDocument8 pagesCredit Insurance PPT Basicshikha82No ratings yet

- Financial Statements and NotesDocument118 pagesFinancial Statements and NotesAlezNgNo ratings yet

- Gafta 49Document4 pagesGafta 49tinhcoonlineNo ratings yet

- Clinton Iraq EmailDocument4 pagesClinton Iraq EmailandrewperezdcNo ratings yet

- Intp LK TW Iv 2019Document141 pagesIntp LK TW Iv 2019Davila RANo ratings yet

- 8int 2005 Jun QDocument4 pages8int 2005 Jun Qapi-19836745No ratings yet

- Mba Employment Statistics PDFDocument52 pagesMba Employment Statistics PDFDwarakanath MuraliNo ratings yet

- An Internship Report On Foreign Exchange Operations of Mercantile Bank LimitedDocument96 pagesAn Internship Report On Foreign Exchange Operations of Mercantile Bank Limitednaimenim100% (2)

- MicroLead - PHB - TK4 - Own Agent Network - BM - ENG PDFDocument55 pagesMicroLead - PHB - TK4 - Own Agent Network - BM - ENG PDFNambasa JoyceNo ratings yet