You might also like

- Principles of Islamic Finance: New Issues and Steps ForwardFrom EverandPrinciples of Islamic Finance: New Issues and Steps ForwardNo ratings yet

- New Microsoft Word DocumentDocument5 pagesNew Microsoft Word DocumentAmina AsimNo ratings yet

- Islamic BankingDocument11 pagesIslamic BankingAmara Ajmal100% (5)

- The Banking System in MalaysiaDocument6 pagesThe Banking System in MalaysiaHong Tat HengNo ratings yet

- Case Study IMU150 (Wakalah)Document16 pagesCase Study IMU150 (Wakalah)Adam BukhariNo ratings yet

- Al BarskhaDocument86 pagesAl BarskhaMian MohsinNo ratings yet

- Islamic Banking in Bangladesh Progress and PotentialsDocument25 pagesIslamic Banking in Bangladesh Progress and PotentialsRaihan MahmoodNo ratings yet

- Islamic Banking in Pakistan Cooperation With Central Bank and Conventioanl BanksDocument14 pagesIslamic Banking in Pakistan Cooperation With Central Bank and Conventioanl BanksM.Majid ShaikhNo ratings yet

- Tawkir Term PaperDocument18 pagesTawkir Term PaperSoniya ZamanNo ratings yet

- Bank ManagementDocument20 pagesBank Managementamirahhani najmaNo ratings yet

- Definition of Investment and Investment MechanismDocument12 pagesDefinition of Investment and Investment MechanismShaheen Mahmud50% (2)

- PGDIFP - Unit 3 Class 2Document93 pagesPGDIFP - Unit 3 Class 2Shadman ShakibNo ratings yet

- Chapter 1: Introduction: Shariah Principles and Avoid Prohibited Activities Such As Gharar (Excessive Uncertainty)Document76 pagesChapter 1: Introduction: Shariah Principles and Avoid Prohibited Activities Such As Gharar (Excessive Uncertainty)Vki BffNo ratings yet

- Chap 10Document2 pagesChap 10MuhammadWaseemNo ratings yet

- Project ReportDocument9 pagesProject ReportZameer AbbasiNo ratings yet

- Islamic Banking Vs Conventional BankingDocument17 pagesIslamic Banking Vs Conventional BankingFarrukh Ahmed Qureshi100% (19)

- Regulation and Performance of Islamic Banking in Bangladesh: Abu Umar Faruq Ahmad M. Kabir HassanDocument27 pagesRegulation and Performance of Islamic Banking in Bangladesh: Abu Umar Faruq Ahmad M. Kabir HassandurporbashiNo ratings yet

- Islamic BankingDocument25 pagesIslamic Bankingmojoo2003No ratings yet

- Final ReportDocument10 pagesFinal ReportMuhammad AliNo ratings yet

- Formate - IJHSS - Historical Background of Islamic Banking in NigeriaDocument8 pagesFormate - IJHSS - Historical Background of Islamic Banking in Nigeriaiaset123No ratings yet

- CandyDocument3 pagesCandyMuhammad Khuram ShahzadNo ratings yet

- Summary Chapter 3 - 237177 - BWFS3093Document2 pagesSummary Chapter 3 - 237177 - BWFS3093AbdiKarem JamalNo ratings yet

- Research MethodologyDocument14 pagesResearch MethodologySounds You WantNo ratings yet

- Principle of Islamic Business and FinanceDocument13 pagesPrinciple of Islamic Business and FinanceHaiderNo ratings yet

- Essentials of Islamic Finance ReportDocument22 pagesEssentials of Islamic Finance ReportFirdous SaeedNo ratings yet

- Islamic Banking in PakistanDocument72 pagesIslamic Banking in PakistanRida ZehraNo ratings yet

- General Banking Activities (CBS)Document15 pagesGeneral Banking Activities (CBS)Ifrat SnigdhaNo ratings yet

- Historical Background of IBBLDocument5 pagesHistorical Background of IBBLSISkobirNo ratings yet

- Islamic Banking PPT - 1Document25 pagesIslamic Banking PPT - 1Govinda ChhanganiNo ratings yet

- The Need For Regulatory ..Awwal Sarker Held On 20-02-2007Document6 pagesThe Need For Regulatory ..Awwal Sarker Held On 20-02-2007turjo987No ratings yet

- Islamic Banking in Bangladesh Progress and PotentialsDocument23 pagesIslamic Banking in Bangladesh Progress and Potentialssumaiya sumaNo ratings yet

- DUBAIISLAMICBANKDocument31 pagesDUBAIISLAMICBANKMubashir Hassan KhanNo ratings yet

- Executive Summary: The Caring BankDocument85 pagesExecutive Summary: The Caring BankKashif AwanNo ratings yet

- AIBL Background of The CompanyDocument6 pagesAIBL Background of The CompanySISkobir100% (1)

- Islamic Money MarketDocument3 pagesIslamic Money MarketALINo ratings yet

- Write A Report On Islamic Banking and Their Profit Sharing Methods Critically Analyzing-2Document18 pagesWrite A Report On Islamic Banking and Their Profit Sharing Methods Critically Analyzing-2Ellis AdaNo ratings yet

- Impact of Traditional Economic On Banking SectorDocument4 pagesImpact of Traditional Economic On Banking SectorKASHMALAFAROOQNo ratings yet

- Assignment of Islamic BankingDocument6 pagesAssignment of Islamic BankingFarjad AliNo ratings yet

- First Security Islami Bank Internship ReportDocument65 pagesFirst Security Islami Bank Internship ReportDurantoDx100% (2)

- Introduction To Islamic BankingDocument3 pagesIntroduction To Islamic BankingEhsan QadirNo ratings yet

- Askari Islamic (Hamza)Document16 pagesAskari Islamic (Hamza)HaiderNo ratings yet

- An Internship Report Final On Shahjalal Islami Bank Limited. BangladeshDocument42 pagesAn Internship Report Final On Shahjalal Islami Bank Limited. BangladeshSanjanMahmood75% (4)

- Investment Performance of Al-Arafah Islami BankDocument64 pagesInvestment Performance of Al-Arafah Islami BankSharifMahmud100% (2)

- Islamic Banking OverviewDocument21 pagesIslamic Banking OverviewmudasirNo ratings yet

- In Partial Fulfilment of The Requirements For: "Islamic Banking"Document50 pagesIn Partial Fulfilment of The Requirements For: "Islamic Banking"rk1510No ratings yet

- Types of Banks: Central BankDocument12 pagesTypes of Banks: Central BankRohit PanjwaniNo ratings yet

- Islamic Banking: Malaysia'S PerspectiveDocument15 pagesIslamic Banking: Malaysia'S PerspectivejawadNo ratings yet

- Internship Report On Bank Islami by Owais ShafiqueDocument300 pagesInternship Report On Bank Islami by Owais ShafiqueOwais ShafiqueNo ratings yet

- Fixe ReportDocument50 pagesFixe Reportrehan mughalNo ratings yet

- 3-Regulation of Islamic Banking in Bangladesh, Role of Bangadesh Bank (Abdul Awwal Sarker)Document5 pages3-Regulation of Islamic Banking in Bangladesh, Role of Bangadesh Bank (Abdul Awwal Sarker)ikutmilisNo ratings yet

- Islamic Treasury IMALDocument11 pagesIslamic Treasury IMALPrashant VishwakarmaNo ratings yet

- Assignment On of Islamic BankingDocument14 pagesAssignment On of Islamic BankingSanjani80% (5)

- Basics of Islamic BankingDocument6 pagesBasics of Islamic BankingMnk BhkNo ratings yet

- Musharakah Securitization Ijarah Securitization Sukuk Types of SukukDocument10 pagesMusharakah Securitization Ijarah Securitization Sukuk Types of Sukukabubakar70No ratings yet

- Ibbl PDFDocument3 pagesIbbl PDFKanij FatemaNo ratings yet

- Law of Banking and Security: Dr. Zulkifli HasanDocument25 pagesLaw of Banking and Security: Dr. Zulkifli HasanQuofi SeliNo ratings yet

- Why Study Islamic Banking and Finance?Document28 pagesWhy Study Islamic Banking and Finance?Princess IntanNo ratings yet

- Business CommunicationDocument56 pagesBusiness CommunicationDipayan_luNo ratings yet

- FX Theory QestionDocument5 pagesFX Theory QestionDipayan_luNo ratings yet

- MKT NewDocument14 pagesMKT NewDipayan_luNo ratings yet

- Central Banking-1Document15 pagesCentral Banking-1Dipayan_luNo ratings yet

- CENTRAL BANKING & MONETARY POLICY Short NoteDocument11 pagesCENTRAL BANKING & MONETARY POLICY Short NoteDipayan_luNo ratings yet

- Fin 219Document3 pagesFin 219Dipayan_luNo ratings yet

- Six Point FormulaDocument2 pagesSix Point FormulaDipayan_luNo ratings yet

- A Case Study On Final)Document1 pageA Case Study On Final)Dipayan_luNo ratings yet

- RBI GUIDELINES ON Working CapitalDocument57 pagesRBI GUIDELINES ON Working Capitalashwini.krs80No ratings yet

- Perfomance BTW NBC and CRDB 2010Document7 pagesPerfomance BTW NBC and CRDB 2010Moud KhalfaniNo ratings yet

- Important: Compound Interest QuestionsDocument12 pagesImportant: Compound Interest QuestionsShraiya ManhasNo ratings yet

- ITC Corporate ValuationDocument6 pagesITC Corporate ValuationSakshi Jain Jaipuria JaipurNo ratings yet

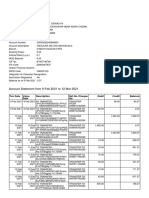

- Account Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument5 pagesAccount Statement From 9 Feb 2021 To 12 Mar 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceABHINAV DEWALIYANo ratings yet

- FABM2 12 Quarter1 Week7Document10 pagesFABM2 12 Quarter1 Week7Princess DuquezaNo ratings yet

- BFI 220 CAT AnswersDocument2 pagesBFI 220 CAT Answerssamkimari5No ratings yet

- Types of Insurance Essentials PowerPointDocument27 pagesTypes of Insurance Essentials PowerPointVinodKumarMNo ratings yet

- 0 - Accounting For Income Tax SummaryDocument7 pages0 - Accounting For Income Tax SummaryJaneNo ratings yet

- Final Report KasbDocument70 pagesFinal Report KasbtrueliarerNo ratings yet

- UNSW FINS1612 Chapter01 - TestBankDocument24 pagesUNSW FINS1612 Chapter01 - TestBankelkieNo ratings yet

- Hedge Fund BackersDocument6 pagesHedge Fund Backers1c796e65b8a4c8No ratings yet

- Act130: Accounting For Special Transactions Prelim Exam S.Y 2020-2021Document15 pagesAct130: Accounting For Special Transactions Prelim Exam S.Y 2020-2021Nhel AlvaroNo ratings yet

- Brand Finance Banking 500 2022 PreviewDocument48 pagesBrand Finance Banking 500 2022 Previewstart-up.ro100% (1)

- A Summer Training Report On HDFC LifeDocument30 pagesA Summer Training Report On HDFC LifeOwais LatiefNo ratings yet

- Account PayableDocument6 pagesAccount PayablenaysarNo ratings yet

- Suncoast Bank StatementDocument3 pagesSuncoast Bank StatementolaNo ratings yet

- Comparative Study Between Two BanksDocument26 pagesComparative Study Between Two BanksAnupam SinghNo ratings yet

- DR Manfred Knof: Curriculum VitaeDocument2 pagesDR Manfred Knof: Curriculum VitaeFernandoNo ratings yet

- Disbursement Voucher: Department of EducationDocument3 pagesDisbursement Voucher: Department of EducationMaria Kristel L PascualNo ratings yet

- Foundations of Financial Management 15Th Edition Block Test Bank Full Chapter PDFDocument67 pagesFoundations of Financial Management 15Th Edition Block Test Bank Full Chapter PDFjavierwarrenqswgiefjyn100% (7)

- 5.3 Income StatementDocument4 pages5.3 Income StatementHiNo ratings yet

- 中英文对照版财务报表及专业名词Document6 pages中英文对照版财务报表及专业名词sandywhgNo ratings yet

- Peer-Review Assessment Course 1aDocument5 pagesPeer-Review Assessment Course 1aSamael LightbringerNo ratings yet

- Westpac Feb4Document2 pagesWestpac Feb4რაქსშ საჰა100% (1)

- Mbaf 605 Lecture Week 10Document71 pagesMbaf 605 Lecture Week 10Gen AbulkhairNo ratings yet

- Sanulac Nutricion Colombia S.A.S. (Colombia) : SourceDocument2 pagesSanulac Nutricion Colombia S.A.S. (Colombia) : SourceCatalina Echeverry AldanaNo ratings yet

- Compound IntrestDocument5 pagesCompound Intrestvenkata sureshNo ratings yet

- Student Information: Check Centre Lot S.NO. Student NameDocument232 pagesStudent Information: Check Centre Lot S.NO. Student NameVijayant GautamNo ratings yet

- Adjusting Accounts and Preparing Financial Statements: We Have Learned - .Document23 pagesAdjusting Accounts and Preparing Financial Statements: We Have Learned - .Đàm Quang Thanh TúNo ratings yet