You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Chapter2 Exercise and TestDocument22 pagesChapter2 Exercise and TestMichelle LamNo ratings yet

- Dealer ManualDocument85 pagesDealer ManualLakelands CyclesNo ratings yet

- Economy Questions in Upsc Prelims 2022 88Document6 pagesEconomy Questions in Upsc Prelims 2022 88RamdulariNo ratings yet

- CH 1 Cost Volume Profit Analysis Absorption CostingDocument21 pagesCH 1 Cost Volume Profit Analysis Absorption CostingNigussie BerhanuNo ratings yet

- Tanzania Budget Highlights 2021-22Document35 pagesTanzania Budget Highlights 2021-22Arden Muhumuza KitomariNo ratings yet

- 7096 w13 Ms 22Document8 pages7096 w13 Ms 22mstudy123456No ratings yet

- Quantitative ProblemsDocument8 pagesQuantitative ProblemsrahimNo ratings yet

- Chapter-2 Concept of DerivativesDocument50 pagesChapter-2 Concept of Derivativesamrin banuNo ratings yet

- Sale of City of Watertown Owned Properties March 2022Document2 pagesSale of City of Watertown Owned Properties March 2022NewzjunkyNo ratings yet

- SkodaDocument29 pagesSkodaPratik Bhuptani75% (4)

- IAS 16 SummaryDocument5 pagesIAS 16 SummarythenikkitrNo ratings yet

- Chapter 11Document24 pagesChapter 11Julien KerroucheNo ratings yet

- Unilever Case Study - HandoutDocument12 pagesUnilever Case Study - HandoutjagaveeraNo ratings yet

- TOEIC - English Reading PracticeDocument6 pagesTOEIC - English Reading PracticekhuelvNo ratings yet

- Chapter IV: The Heckscher-Ohlin Model: L K L KDocument5 pagesChapter IV: The Heckscher-Ohlin Model: L K L KNguyễn ThươngNo ratings yet

- Itc WaccDocument185 pagesItc WaccvATSALANo ratings yet

- Barringer E3 PPT 13Document26 pagesBarringer E3 PPT 13Aamir BalochNo ratings yet

- Week 1 Introduction To Economics NotesDocument3 pagesWeek 1 Introduction To Economics Notessuruthi.uthayakumarNo ratings yet

- A Gas-1-5-2-4-2-1-2-1-1-1-3-1-1Document1 pageA Gas-1-5-2-4-2-1-2-1-1-1-3-1-1Daia SorinNo ratings yet

- Test Bank For Business Its Legal Ethical and Global Environment 9th Edition JenningsDocument19 pagesTest Bank For Business Its Legal Ethical and Global Environment 9th Edition Jenningsa549795291No ratings yet

- Cost Acctg - Chapter 2 & 3Document4 pagesCost Acctg - Chapter 2 & 3Hamoudy DianalanNo ratings yet

- Water Level IndicatorDocument10 pagesWater Level IndicatorKodati KasiNo ratings yet

- Macro Tut 2 With Ans 3Document7 pagesMacro Tut 2 With Ans 3Van Anh LeNo ratings yet

- Cost Concepts & Its AnalysisDocument19 pagesCost Concepts & Its AnalysisKenen Bhandhavi100% (1)

- Economics For Managers Global Edition 3rd Edition Farnham Solutions ManualDocument16 pagesEconomics For Managers Global Edition 3rd Edition Farnham Solutions Manualchristinetayloraegynjcxdf100% (11)

- Forex Currency Trading ExplainedDocument11 pagesForex Currency Trading ExplainedDemi Sanya100% (1)

- Hero Hond: Marketing and Human Resource ManagementDocument70 pagesHero Hond: Marketing and Human Resource Managementdhiraj022No ratings yet

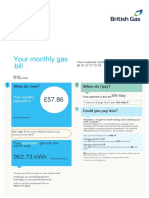

- Get PDF For Bill ViewDocument4 pagesGet PDF For Bill ViewKrishna8765No ratings yet

- Integrated Reporting: Communicating Value Transparently/TITLEDocument228 pagesIntegrated Reporting: Communicating Value Transparently/TITLEjsmnjasminesNo ratings yet

- B124 - Book 7 Part 2: Standard Costing and Variance AnalysisDocument40 pagesB124 - Book 7 Part 2: Standard Costing and Variance AnalysisNabil Al hajjNo ratings yet