You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- List of The Top 10 Leather Manufacturers in BangladeshDocument4 pagesList of The Top 10 Leather Manufacturers in BangladeshNasim HasanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Presentation - Sacli 2018Document10 pagesPresentation - Sacli 2018Marius OosthuizenNo ratings yet

- Paris Climate Agreement SummaryDocument3 pagesParis Climate Agreement SummaryDorian Grey100% (1)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- BES4-Assignment 3Document2 pagesBES4-Assignment 3look porrNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- WEG India Staff Contact Numbers PDFDocument10 pagesWEG India Staff Contact Numbers PDFM.DINESH KUMARNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- La Part 3 PDFDocument23 pagesLa Part 3 PDFShubhaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- PPSAS 28 - Financial Instruments - Presentation 3-18-2013Document3 pagesPPSAS 28 - Financial Instruments - Presentation 3-18-2013Christian Ian LimNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Airport Design WIRATMAN ARCHITECTURE. Imelda Akmal Architecture Writer Studio Wiratman - Revisi CP II - Indd 3 10 - 5 - 16 10 - 21 AMDocument9 pagesAirport Design WIRATMAN ARCHITECTURE. Imelda Akmal Architecture Writer Studio Wiratman - Revisi CP II - Indd 3 10 - 5 - 16 10 - 21 AMRasyidashariNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Indias Defence BudgetDocument1 pageIndias Defence BudgetNishkamyaNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Birth Certificate: Rehabilitative Services" (HRS) - Each STATE Is Required To Supply The UNITED STATES WithDocument4 pagesThe Birth Certificate: Rehabilitative Services" (HRS) - Each STATE Is Required To Supply The UNITED STATES Withpandabearkt50% (2)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- CET Analysis of SamsungDocument9 pagesCET Analysis of SamsungMj PayalNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Syllabus DUDocument67 pagesSyllabus DUMohit GoyalNo ratings yet

- The Affluent SocietyDocument189 pagesThe Affluent SocietyOtter1zNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Manual AdeptDocument196 pagesManual AdeptGonzalo MontanoNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Indirect Impact of GST On Income TaxDocument14 pagesIndirect Impact of GST On Income TaxNAMAN KANSALNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Indraneel N M.com SBKDocument3 pagesIndraneel N M.com SBKJared MartinNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Project ProposalDocument7 pagesProject Proposalrehmaniaaa100% (3)

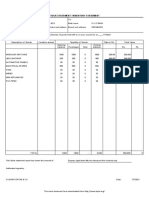

- Stock Statement Format For Bank LoanDocument1 pageStock Statement Format For Bank Loanpsycho Neha40% (5)

- Paul Buchanan - Traffic in Towns and Transport in CitiesDocument20 pagesPaul Buchanan - Traffic in Towns and Transport in CitiesRaffaeleNo ratings yet

- Vinod Rai Not Just An Accountant PDFDocument285 pagesVinod Rai Not Just An Accountant PDFVenkat AdithyaNo ratings yet

- M&A Module 1Document56 pagesM&A Module 1avinashj8100% (1)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

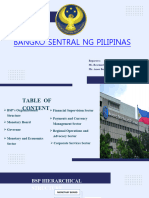

- BSP ReportDocument20 pagesBSP ReportRosemarie CabahugNo ratings yet

- L 1Document5 pagesL 1Elizabeth Espinosa ManilagNo ratings yet

- Final Paper (Assignment of Globalization Problems) - TFR 1.1KDocument1 pageFinal Paper (Assignment of Globalization Problems) - TFR 1.1KJayboy SARTORIONo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Buyer Questionnaire: General QuestionsDocument3 pagesBuyer Questionnaire: General Questionsshweta meshramNo ratings yet

- Chapter 6 MoodleDocument36 pagesChapter 6 MoodleMichael TheodricNo ratings yet

- Case Study 18 PresentationDocument11 pagesCase Study 18 PresentationZara KhanNo ratings yet

- Proposal Project AyamDocument14 pagesProposal Project AyamIrvan PamungkasNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Steeple AnalysisDocument2 pagesSteeple AnalysisSamrahNo ratings yet

- Accounting EquationDocument2 pagesAccounting Equationmeenagoyal9956No ratings yet

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)