You might also like

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- India 3g Auctions Q&a 2010 25 10 MedianamaDocument98 pagesIndia 3g Auctions Q&a 2010 25 10 MedianamamixedbagNo ratings yet

- IAMAI - Pre Budget MemorandumDocument21 pagesIAMAI - Pre Budget MemorandummixedbagNo ratings yet

- India 3g Auctions Notice Inviting Applications 2010 25 10 MedianamaDocument113 pagesIndia 3g Auctions Notice Inviting Applications 2010 25 10 MedianamamixedbagNo ratings yet

- Q3 2009 UTV Software Communications Financials Uploaded by MediaNamaDocument1 pageQ3 2009 UTV Software Communications Financials Uploaded by MediaNamamixedbagNo ratings yet

- Doordarshan MobileTV Tender MediaNamaDocument39 pagesDoordarshan MobileTV Tender MediaNamamixedbag100% (5)

- GSM Monthly Oct08 Medianama - ComDocument9 pagesGSM Monthly Oct08 Medianama - Commixedbag100% (1)

- UTV Software Communications LimitedDocument13 pagesUTV Software Communications LimitedmixedbagNo ratings yet

- q209 - Airtel Published FinancialsDocument7 pagesq209 - Airtel Published Financialsmixedbag100% (2)

- q1 09 IOL Netcom ResultsDocument1 pageq1 09 IOL Netcom ResultsmixedbagNo ratings yet

- Tel No:-011-2321 7914 Fax: - 011-2321 1998 Email: - Skgupta@trai - Gov.in WebsiteDocument5 pagesTel No:-011-2321 7914 Fax: - 011-2321 1998 Email: - Skgupta@trai - Gov.in Websitemixedbag100% (1)

- Rbi-Guidelines - Prepaid-Payments-Medianama - ComDocument7 pagesRbi-Guidelines - Prepaid-Payments-Medianama - Commixedbag100% (2)

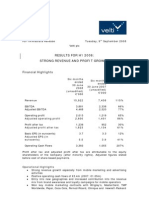

- Results For H1 2008: Strong Revenue and Profit Growth: Financial HighlightsDocument18 pagesResults For H1 2008: Strong Revenue and Profit Growth: Financial HighlightsmixedbagNo ratings yet

- Q109 Airtel FinancialsDocument45 pagesQ109 Airtel FinancialsmixedbagNo ratings yet

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Web18-Q2-2008-09 FinancialsDocument14 pagesWeb18-Q2-2008-09 Financialsmixedbag100% (1)

- Utv Earnings Release 2qfy2009Document9 pagesUtv Earnings Release 2qfy2009mixedbagNo ratings yet

- Annual Report - 2007-08 Info EdgeDocument121 pagesAnnual Report - 2007-08 Info EdgemixedbagNo ratings yet

- Nokia Conference Call Third Quarter 2008 Financial Results: October 16, 2008 15.00 Helsinki Time 8.00 New York TimeDocument19 pagesNokia Conference Call Third Quarter 2008 Financial Results: October 16, 2008 15.00 Helsinki Time 8.00 New York TimemixedbagNo ratings yet

- Annual Report - 2007-08 Info EdgeDocument121 pagesAnnual Report - 2007-08 Info EdgemixedbagNo ratings yet

- NDTV Q2-09 ResultsDocument8 pagesNDTV Q2-09 ResultsmixedbagNo ratings yet

- India - RBI Mobile Banking Guidelines - 20081010 Via Medianama - ComDocument7 pagesIndia - RBI Mobile Banking Guidelines - 20081010 Via Medianama - Commixedbag100% (3)

- Annual Report 2007 2008 AirtelDocument162 pagesAnnual Report 2007 2008 AirtelHarsh MaddyNo ratings yet

- Rbi - Operative Guidelines For Mobile BankingDocument7 pagesRbi - Operative Guidelines For Mobile Bankingmixedbag100% (2)

- Iproperty IPGA ProspectusDocument154 pagesIproperty IPGA ProspectusmixedbagNo ratings yet

- Banks Reports-Aug2008Document5 pagesBanks Reports-Aug2008mixedbagNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Electrocomponents - RS Group - Investor - Event - 2022 - Presentation - 30.03.2022Document105 pagesElectrocomponents - RS Group - Investor - Event - 2022 - Presentation - 30.03.2022sydubh72No ratings yet

- Chapter 12 - Macroeconomic and Industry AnalysisDocument8 pagesChapter 12 - Macroeconomic and Industry AnalysisMarwa HassanNo ratings yet

- Ey Cafta Case Championship 2022 Chapter 2Document17 pagesEy Cafta Case Championship 2022 Chapter 2Wavare YashNo ratings yet

- Notice To Terminate - 16 June 2023Document2 pagesNotice To Terminate - 16 June 2023Mary Nove PatanganNo ratings yet

- Daniel F. Spulber - Global Competitive Strategy-Cambridge University Press (2007)Document306 pagesDaniel F. Spulber - Global Competitive Strategy-Cambridge University Press (2007)沈化文No ratings yet

- BA TecniquesDocument55 pagesBA Tecniquesloveykhurana5980100% (2)

- FNFIndia OverviewDocument2 pagesFNFIndia OverviewyejamiNo ratings yet

- Canara BankDocument2 pagesCanara Banklinsonjohny34No ratings yet

- Introduction To International Human Resource ManagementDocument16 pagesIntroduction To International Human Resource Managementashishapp88% (8)

- A Guide To Preparing For Sales and TradiDocument4 pagesA Guide To Preparing For Sales and TradiBrenda WijayaNo ratings yet

- Customer Service ExampleDocument27 pagesCustomer Service ExampleSha EemNo ratings yet

- FinalpdndDocument32 pagesFinalpdndPulkit Garg100% (1)

- Project ReportDocument52 pagesProject ReportAkanksha SinhaNo ratings yet

- Hepm 3102 Project Leadership and CommunicationDocument11 pagesHepm 3102 Project Leadership and CommunicationestherNo ratings yet

- Customer Journey MappingDocument1 pageCustomer Journey MappingPriyanka RaniNo ratings yet

- Ebook Essentials of Investments 12E Ise PDF Full Chapter PDFDocument67 pagesEbook Essentials of Investments 12E Ise PDF Full Chapter PDFjanet.cochran431100% (22)

- Six Sigma vs. Quality CircleDocument6 pagesSix Sigma vs. Quality CircleBhavin GandhiNo ratings yet

- Raw Fury ContractDocument14 pagesRaw Fury ContractMichael Futter100% (1)

- Up To Date CVDocument4 pagesUp To Date CViqbal1439988No ratings yet

- Ferrari Case StudyDocument2 pagesFerrari Case StudyjamesngNo ratings yet

- Case Study of Satyam ScamDocument21 pagesCase Study of Satyam ScamSyed Sammar Abbas KazmiNo ratings yet

- Chapter Five Practice: Cost Behavior: Analysis and UseDocument6 pagesChapter Five Practice: Cost Behavior: Analysis and UseKhaled Abo YousefNo ratings yet

- Stack Company Overview - Sept 2021Document12 pagesStack Company Overview - Sept 2021Srinivas AnnamarajuNo ratings yet

- The Role of Non-Executive Directors in Corporate Governance: An EvaluationDocument34 pagesThe Role of Non-Executive Directors in Corporate Governance: An Evaluationsharonlow88No ratings yet

- Models of InternationaisationDocument8 pagesModels of InternationaisationShreyas RautNo ratings yet

- Electronic Business SystemsDocument44 pagesElectronic Business Systemsmotz100% (4)

- Robinhood Case StudyDocument3 pagesRobinhood Case StudyXnort G. XwestNo ratings yet

- Case Study (Solved)Document10 pagesCase Study (Solved)Aditya DsNo ratings yet

- Swiggy Refine - AswathyUdhayDocument6 pagesSwiggy Refine - AswathyUdhayAswathy UdhayakumarNo ratings yet

- Workshop On Training Needs AssessmentDocument113 pagesWorkshop On Training Needs AssessmentMike PattersonNo ratings yet