You might also like

- 2024 20 2 17 18 07 Passbookstmt - 1708429687898Document7 pages2024 20 2 17 18 07 Passbookstmt - 1708429687898Saravanavel CNo ratings yet

- The Berenstain Bears Blessed Are The PeacemakersDocument10 pagesThe Berenstain Bears Blessed Are The PeacemakersZondervan45% (20)

- Nedbank Investment Statement - 28 Oct 2023Document2 pagesNedbank Investment Statement - 28 Oct 2023mabuyisizakeleNo ratings yet

- FNB Pay Slip Sep-1Document1 pageFNB Pay Slip Sep-1Arnoldz WaldemarNo ratings yet

- Statement NewDocument2 pagesStatement NewabhiramNo ratings yet

- Salman Khoirudin: Account SummaryDocument3 pagesSalman Khoirudin: Account SummarySalman KhoirudinNo ratings yet

- Philippines The Manila Electric Company Electricity CompanyDocument1 pagePhilippines The Manila Electric Company Electricity CompanyPiyushNo ratings yet

- Account StatementDocument3 pagesAccount StatementErmec AtachikovNo ratings yet

- Universal Principles of Biomedical EthicsDocument16 pagesUniversal Principles of Biomedical EthicsMEOW41100% (3)

- Jose Espinoza water bill detailsDocument1 pageJose Espinoza water bill detailsJose EspinozaNo ratings yet

- Checklist - Credentialing Initial DRAFTDocument3 pagesChecklist - Credentialing Initial DRAFTDebbie100% (1)

- 00004848-Ewa 7327693Document1 page00004848-Ewa 7327693radha jayaramanNo ratings yet

- January Postpay BillDocument4 pagesJanuary Postpay BillestrobetceoNo ratings yet

- Please PAY: TOTAL: $997.50 BY: 12-APR-2023Document1 pagePlease PAY: TOTAL: $997.50 BY: 12-APR-2023ICCNo ratings yet

- Wa0017.Document4 pagesWa0017.Fafa WarchatNo ratings yet

- Heng Tai Int'L Frright Co.,Ltd Bill of LandingDocument1 pageHeng Tai Int'L Frright Co.,Ltd Bill of LandingvijayNo ratings yet

- Electricity BillDocument1 pageElectricity BillARPIT TELECOMNo ratings yet

- Philippines The Manila Electric Company Electricity Company 1 95851Document1 pagePhilippines The Manila Electric Company Electricity Company 1 95851البرنس اليمنيNo ratings yet

- Í - (+È NAILSÂDOTÂGLOWÂPH ÂÂÂ Â Ç+&' 5+Î Nails Dot Glow Phils., IncDocument2 pagesÍ - (+È NAILSÂDOTÂGLOWÂPH ÂÂÂ Â Ç+&' 5+Î Nails Dot Glow Phils., IncRACELLE ACCOUNTINGNo ratings yet

- Bank of Kigali Investor Presentation Q1 & 3M 2012Document43 pagesBank of Kigali Investor Presentation Q1 & 3M 2012Bank of Kigali100% (1)

- View your account statement onlineDocument1 pageView your account statement onlineossamamhelmyNo ratings yet

- Meter Reading and Consumption ﺗ ﻔ ﺎ ﺻ ﻳ ﻝ ﺍﻟ ﻘ ﺭ ﺍ ء ﺓ ﻭ ﺍ ﻻ ﺳ ﺗ ﻬ ﻼ ﻙDocument1 pageMeter Reading and Consumption ﺗ ﻔ ﺎ ﺻ ﻳ ﻝ ﺍﻟ ﻘ ﺭ ﺍ ء ﺓ ﻭ ﺍ ﻻ ﺳ ﺗ ﻬ ﻼ ﻙKCNo ratings yet

- Bolivia ENDE Corporacion Electricity Wutility BillaDocument1 pageBolivia ENDE Corporacion Electricity Wutility Billamike fastNo ratings yet

- DBS Singapore Bank Statement PDFDocument13 pagesDBS Singapore Bank Statement PDFMuhammad OwaisNo ratings yet

- JTL WifiDocument1 pageJTL WifiRowlan NyagaNo ratings yet

- Bank of Kigali 2010 9M 2010 Results UpdateDocument59 pagesBank of Kigali 2010 9M 2010 Results UpdateBank of KigaliNo ratings yet

- Bank of Kigali 2010 9M 2010 Results UpdateDocument59 pagesBank of Kigali 2010 9M 2010 Results UpdateBank of KigaliNo ratings yet

- Pulana Martha Malatji - 2023 - 06 - 27Document2 pagesPulana Martha Malatji - 2023 - 06 - 27Vee-kay Vicky KatekaniNo ratings yet

- Nigeria Bank StatementDocument2 pagesNigeria Bank StatementДанила ФилатовNo ratings yet

- Sde Notes Lit and Vital Issues FinalDocument115 pagesSde Notes Lit and Vital Issues FinalShamsuddeen Nalakath100% (14)

- Savings Account Statement: Capitec B AnkDocument4 pagesSavings Account Statement: Capitec B AnkJon LwaziNo ratings yet

- Mr. Subramanian Alagappan bank account statementDocument1 pageMr. Subramanian Alagappan bank account statementmanianNo ratings yet

- Origin Standing Bill ExampleDocument2 pagesOrigin Standing Bill ExampleMasonNo ratings yet

- Screenshot 2022-12-11 at 18.17.13 PDFDocument1 pageScreenshot 2022-12-11 at 18.17.13 PDFLihle ShongweNo ratings yet

- Statement 600611 35853301 05 11 2019 05 12 2019Document2 pagesStatement 600611 35853301 05 11 2019 05 12 2019jeffwork1976No ratings yet

- Commerzbank Account StatementDocument7 pagesCommerzbank Account StatementОльга ШтроNo ratings yet

- Your E-Bill For September - 2020 Customer 489291 1442 - 02 - 18 - 11 - 42 - 2642 PDFDocument2 pagesYour E-Bill For September - 2020 Customer 489291 1442 - 02 - 18 - 11 - 42 - 2642 PDFSanu PhilipNo ratings yet

- Understanding Your Water Bill - SampleDocument3 pagesUnderstanding Your Water Bill - SampleBenny BerniceNo ratings yet

- CouncilTax DD FormDocument2 pagesCouncilTax DD Formutkarsh23No ratings yet

- STTTTDocument1 pageSTTTTRA OUFNo ratings yet

- X-000009-1603383942652-50963-BBE - Assignment 01Document66 pagesX-000009-1603383942652-50963-BBE - Assignment 01PeuJp75% (4)

- Electricity Bill Details for 63 kWh UsageDocument2 pagesElectricity Bill Details for 63 kWh Usagefulica13No ratings yet

- Titas Gas & Electricity Bill Payment June 2023Document4 pagesTitas Gas & Electricity Bill Payment June 2023YousufNo ratings yet

- Joubert 20 Caledon Statement 03 January 2022Document1 pageJoubert 20 Caledon Statement 03 January 2022Wynand van den BergNo ratings yet

- 2020 December StatementDocument2 pages2020 December Statementfatemeh mokhtariNo ratings yet

- SILASDocument1 pageSILASKaronyo JNo ratings yet

- Report 2021 Aug 15 145917Document9 pagesReport 2021 Aug 15 145917dina beniniNo ratings yet

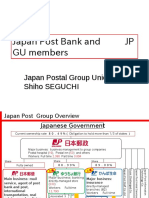

- 01 Japan Post Bank-EDocument10 pages01 Japan Post Bank-ELaxmi Narayana ChennaboinaNo ratings yet

- BillDocument2 pagesBillDamien DasteNo ratings yet

- Ap 6050003562019Document1 pageAp 6050003562019Vijayraj SriramNo ratings yet

- Binder1 PDFDocument2 pagesBinder1 PDFTARFRENo ratings yet

- SBI Statement July 2017-2018 PDFDocument2 pagesSBI Statement July 2017-2018 PDFSai SameerNo ratings yet

- Statement 2024 1Document1 pageStatement 2024 1xfzm99mr8rNo ratings yet

- Official Receipt: Date: 27 Sep 2021 Receipt No. LPL202100526-128Document1 pageOfficial Receipt: Date: 27 Sep 2021 Receipt No. LPL202100526-128SimonNo ratings yet

- Indraprastha Gas Limited bill details and customer care numbersDocument1 pageIndraprastha Gas Limited bill details and customer care numbersashishNo ratings yet

- Manas Water BilDocument1 pageManas Water BilJitesh SharmaNo ratings yet

- HDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Document2 pagesHDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971golu84No ratings yet

- Gasbill 8083511000 202003 20200402145346 PDFDocument1 pageGasbill 8083511000 202003 20200402145346 PDFimranmehfoozNo ratings yet

- Please PAY: TOTAL: $21,306.06 BY: 12-DEC-2022Document1 pagePlease PAY: TOTAL: $21,306.06 BY: 12-DEC-2022Joan davisNo ratings yet

- VozackaDocument2 pagesVozackaMiranGazda100% (1)

- Payslip 07%20-%20%202023Document1 pagePayslip 07%20-%20%202023aha34432No ratings yet

- CASA Statement 1606148149984Document2 pagesCASA Statement 1606148149984akundonlot filemNo ratings yet

- FATCA White Paper NormalDocument1 pageFATCA White Paper Normalsumairjawed8116No ratings yet

- Sman 1 Lumbis: NO Description AmountDocument4 pagesSman 1 Lumbis: NO Description AmounthaerilNo ratings yet

- Pesco Online BilllDocument1 pagePesco Online BilllQaiser Khan Jadoon100% (1)

- State Bank of IndiaDocument1 pageState Bank of IndiaAnjusha NairNo ratings yet

- Murad Engineering Services Statement SummaryDocument2 pagesMurad Engineering Services Statement SummarysajuNo ratings yet

- Bank of Kigali Receives The Best African Listing Award and Best Bank in Rwanda AwardDocument2 pagesBank of Kigali Receives The Best African Listing Award and Best Bank in Rwanda AwardBank of KigaliNo ratings yet

- Bank of Kigali Investor Presentation Full Year 2011Document42 pagesBank of Kigali Investor Presentation Full Year 2011Bank of KigaliNo ratings yet

- 2011 Annual ReportDocument96 pages2011 Annual ReportOsman SalihNo ratings yet

- Bank of Kigali Investor Presentation Q1 &3M 2012Document43 pagesBank of Kigali Investor Presentation Q1 &3M 2012Bank of KigaliNo ratings yet

- Bank of Kigali Credit Review 2011Document6 pagesBank of Kigali Credit Review 2011Bank of KigaliNo ratings yet

- Bank of Kigali Announces 1H 2012 & Q2 2012 Reviewed ResultsDocument9 pagesBank of Kigali Announces 1H 2012 & Q2 2012 Reviewed ResultsBank of KigaliNo ratings yet

- Bank of Kigali Investor Presentation 1H2012Document44 pagesBank of Kigali Investor Presentation 1H2012Bank of KigaliNo ratings yet

- Bank of Kigali Investor Presentation 1H2012Document44 pagesBank of Kigali Investor Presentation 1H2012Bank of KigaliNo ratings yet

- Bank of Kigali Announces Q1 2012 Reviewed ResultsDocument8 pagesBank of Kigali Announces Q1 2012 Reviewed ResultsBank of KigaliNo ratings yet

- Bank of Kigali Investor Day Presentation 27th April 2012Document43 pagesBank of Kigali Investor Day Presentation 27th April 2012Bank of KigaliNo ratings yet

- Bank of Kigali Receives Best East African BankDocument1 pageBank of Kigali Receives Best East African BankBank of KigaliNo ratings yet

- Bank of Kigali Limited: Financially Transforming LivesDocument3 pagesBank of Kigali Limited: Financially Transforming LivesBank of KigaliNo ratings yet

- Bank of Kigali Announces Full-Year 2011 and Q4 2011 IFRS Audited ResultsDocument9 pagesBank of Kigali Announces Full-Year 2011 and Q4 2011 IFRS Audited ResultsBank of KigaliNo ratings yet

- Bank of Kigali Annual Report 2009Document80 pagesBank of Kigali Annual Report 2009Bank of KigaliNo ratings yet

- National Bank of Rwanda Quarterly Bulletin Third Quarter 2011Document88 pagesNational Bank of Rwanda Quarterly Bulletin Third Quarter 2011Bank of KigaliNo ratings yet

- Bank of Kigali Annual Report 2010Document92 pagesBank of Kigali Annual Report 2010Bank of Kigali0% (3)

- National Bank of Rwanda Quarterly Bulletin Second Quarter 2011Document88 pagesNational Bank of Rwanda Quarterly Bulletin Second Quarter 2011Bank of KigaliNo ratings yet

- National Bank of Rwanda Quarterly Bulletin Fourth Quarter 2010Document102 pagesNational Bank of Rwanda Quarterly Bulletin Fourth Quarter 2010Bank of KigaliNo ratings yet

- Bank of Kigali Announces Q2 2011 & 1H 2011 ResultsDocument9 pagesBank of Kigali Announces Q2 2011 & 1H 2011 ResultsBank of KigaliNo ratings yet

- National Bank of Rwanda Quarterly Bulletin First Quarter 2011Document69 pagesNational Bank of Rwanda Quarterly Bulletin First Quarter 2011Bank of KigaliNo ratings yet

- Bank of Kigali 2010 Q4 2010 Results UpdateDocument66 pagesBank of Kigali 2010 Q4 2010 Results UpdateBank of KigaliNo ratings yet

- BOK Investor Presentation Year To September 2011Document29 pagesBOK Investor Presentation Year To September 2011Bank of KigaliNo ratings yet

- Bank of Kigali Announces Q1 2011 ResultsDocument8 pagesBank of Kigali Announces Q1 2011 ResultsBank of KigaliNo ratings yet

- Bank of Kigali Announces Q1 2010 ResultsDocument7 pagesBank of Kigali Announces Q1 2010 ResultsBank of KigaliNo ratings yet

- Bank of Kigali Announces Q3 2011 and 9M 2011 Reviewed ResultsDocument9 pagesBank of Kigali Announces Q3 2011 and 9M 2011 Reviewed ResultsBank of KigaliNo ratings yet

- Safety data sheet for TL 011 lubricantDocument8 pagesSafety data sheet for TL 011 lubricantXavierNo ratings yet

- NaMo Case StudyDocument4 pagesNaMo Case StudyManish ShawNo ratings yet

- Ds Tata Power Solar Systems Limited 1: Outline AgreementDocument8 pagesDs Tata Power Solar Systems Limited 1: Outline AgreementM Q ASLAMNo ratings yet

- Prince SmartFit CPVC Piping System Price ListDocument1 pagePrince SmartFit CPVC Piping System Price ListPrince Raja38% (8)

- DBBL Online Banking AssignmentDocument11 pagesDBBL Online Banking AssignmentzonayetgaziNo ratings yet

- Brief History of PhilippinesDocument6 pagesBrief History of PhilippinesIts Me MGNo ratings yet

- LKO DEL: Paney / Rajat MRDocument2 pagesLKO DEL: Paney / Rajat MRMeghaNo ratings yet

- LPB Vs DAR-DigestDocument2 pagesLPB Vs DAR-DigestremoveignoranceNo ratings yet

- Labor Cases Just Cause Loss of Confidence PDFDocument177 pagesLabor Cases Just Cause Loss of Confidence PDFRj MendozaNo ratings yet

- AsfsadfasdDocument22 pagesAsfsadfasdJonathan BautistaNo ratings yet

- CH7 Lecture SlidesDocument30 pagesCH7 Lecture SlidesRomeo BalingaoNo ratings yet

- NAS1832 Thru NAS1836, Inserts: Genuine Aircraft Hardware CoDocument3 pagesNAS1832 Thru NAS1836, Inserts: Genuine Aircraft Hardware CoSon NguyenNo ratings yet

- Innovation & Entrepreneursh IP: The $100 Startup Book Review Presented by Naveen RajDocument19 pagesInnovation & Entrepreneursh IP: The $100 Startup Book Review Presented by Naveen RajNaveen RajNo ratings yet

- Our Native Hero: The Rizal Retraction and Other CasesDocument7 pagesOur Native Hero: The Rizal Retraction and Other CasesKrichelle Anne Escarilla IINo ratings yet

- Module 2 - Part III - UpdatedDocument38 pagesModule 2 - Part III - UpdatedDhriti NayyarNo ratings yet

- Ra Construction and Development Corp.Document3 pagesRa Construction and Development Corp.janus jarderNo ratings yet

- Dr. Annasaheb G.D. Bendale Memorial 9th National Moot Court CompetitionDocument4 pagesDr. Annasaheb G.D. Bendale Memorial 9th National Moot Court CompetitionvyasdesaiNo ratings yet

- 14th Finance CommissionDocument4 pages14th Finance CommissionMayuresh SrivastavaNo ratings yet

- Guingona v. Gonzales G.R. No. 106971 March 1, 1993Document1 pageGuingona v. Gonzales G.R. No. 106971 March 1, 1993Bernadette SandovalNo ratings yet

- Godisnjak PFSA 2018 Za WebDocument390 pagesGodisnjak PFSA 2018 Za WebAida HamidovicNo ratings yet

- NELSON MANDELA Worksheet Video BIsDocument3 pagesNELSON MANDELA Worksheet Video BIsAngel Angeleri-priftis.No ratings yet

- Format For Computation of Income Under Income Tax ActDocument3 pagesFormat For Computation of Income Under Income Tax ActAakash67% (3)

- Dhananjay Shanker Shetty Vs State of Maharashtra - 102616Document9 pagesDhananjay Shanker Shetty Vs State of Maharashtra - 102616Rachana GhoshtekarNo ratings yet

- Impact of Pop Culture On PoliticsDocument3 pagesImpact of Pop Culture On PoliticsPradip luitelNo ratings yet

- Bwff1013 Foundations of Finance Quiz #3Document8 pagesBwff1013 Foundations of Finance Quiz #3tivaashiniNo ratings yet