You might also like

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Payment Information Summary of Account ActivityDocument8 pagesPayment Information Summary of Account ActivityElizabeth Marie MendelsohnNo ratings yet

- Introduction - Lending Operations & Risk Management-Lecture-1Document111 pagesIntroduction - Lending Operations & Risk Management-Lecture-1nawazjiskani100% (2)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Tax 2 - Midterm ExamDocument2 pagesTax 2 - Midterm ExamMichelle MatubisNo ratings yet

- TCC Midc Company ListDocument4 pagesTCC Midc Company ListAbhishek SinghNo ratings yet

- Indian Automotive Industry Overview and MG Motors PerformanceDocument51 pagesIndian Automotive Industry Overview and MG Motors PerformanceYatharth Sharma0% (1)

- Key FiguresDocument25 pagesKey Figureschallenger906No ratings yet

- SM-External Assessment (3) 20071 - 22 & 20072 - 5Document48 pagesSM-External Assessment (3) 20071 - 22 & 20072 - 5challenger906No ratings yet

- Amegy Bank TMOverviewDocument32 pagesAmegy Bank TMOverviewsajesh_wNo ratings yet

- Perfect Substitutes and Perfect ComplementsDocument2 pagesPerfect Substitutes and Perfect ComplementsVijayalaxmi DhakaNo ratings yet

- Forex - Nnet Vs RegDocument6 pagesForex - Nnet Vs RegAnshik BansalNo ratings yet

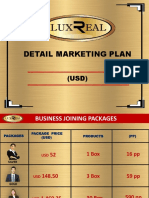

- Luxreal Detail Marketing Plan (2019) UsdDocument32 pagesLuxreal Detail Marketing Plan (2019) UsdTawanda Tirivangani100% (2)

- Infosys Aptitude Questions and Answers With ExplanationDocument5 pagesInfosys Aptitude Questions and Answers With ExplanationVirrru NarendraNo ratings yet

- PDFDocument16 pagesPDFAnil KhadkaNo ratings yet

- Mishkin Econ13e PPT 17Document25 pagesMishkin Econ13e PPT 17Huyền Nhi QuảnNo ratings yet

- PUMBA - DSE A - 506 - LDIM - 1.1 - Nature and Scope of International Trade Law - NotesDocument4 pagesPUMBA - DSE A - 506 - LDIM - 1.1 - Nature and Scope of International Trade Law - NotesTô Mì HakkaNo ratings yet

- En 1567Document8 pagesEn 1567tuyen.nguyenNo ratings yet

- Macroeconomic Analysis of USA: GDP, Inflation & UnemploymentDocument2 pagesMacroeconomic Analysis of USA: GDP, Inflation & UnemploymentVISHAL GOYALNo ratings yet

- Option To PurchaseDocument3 pagesOption To PurchaseAlberta Real EstateNo ratings yet

- Solutions: ECO 100Y Introduction To Economics Midterm Test # 2Document15 pagesSolutions: ECO 100Y Introduction To Economics Midterm Test # 2examkillerNo ratings yet

- Reading: Time Allowed: 90 Minutes Maximum Marks: 40 General InstructionsDocument5 pagesReading: Time Allowed: 90 Minutes Maximum Marks: 40 General InstructionssayedNo ratings yet

- GST Assignment1.1lDocument3 pagesGST Assignment1.1lHamza AliNo ratings yet

- LANDON LTDDocument2 pagesLANDON LTDStephanie ChristianNo ratings yet

- Ethio-Views Online News PaperDocument1 pageEthio-Views Online News PaperBelayneh zelelewNo ratings yet

- K&N Case Group - 3Document41 pagesK&N Case Group - 3priya_pritika6561100% (1)

- Fremantle Line: Looking For More Information?Document12 pagesFremantle Line: Looking For More Information?lerplataNo ratings yet

- Saguibin QADocument1 pageSaguibin QAJack-jack Romaquin100% (1)

- 10th March: by Dr. Gaurav GargDocument2 pages10th March: by Dr. Gaurav GarganupamNo ratings yet

- Pengaruh Kualitas Bahan Baku Dan ProsesDocument11 pagesPengaruh Kualitas Bahan Baku Dan Proses039 Trio SukmonoNo ratings yet

- Training Manual PPDocument26 pagesTraining Manual PPKingsmond EhimareNo ratings yet

- Sales and Purchases 2021-22Document15 pagesSales and Purchases 2021-22Vamsi ShettyNo ratings yet

- Local Business EnvironmentDocument3 pagesLocal Business EnvironmentJayMoralesNo ratings yet

- AG R2 E PrintDocument308 pagesAG R2 E PrintPrem KumarNo ratings yet

- Edp Imp QuestionsDocument3 pagesEdp Imp QuestionsAshutosh SinghNo ratings yet

- List of Maharashtra Pharrma CompaniesDocument6 pagesList of Maharashtra Pharrma CompaniesrajnayakpawarNo ratings yet