You might also like

- 1648 Taft Avenue Corner Pedro Gil Street Malate, City of Manila, PhilippinesDocument11 pages1648 Taft Avenue Corner Pedro Gil Street Malate, City of Manila, PhilippinesBenNo ratings yet

- Test Bank Bank For Strategic Marketing 9 E by CravensDocument13 pagesTest Bank Bank For Strategic Marketing 9 E by CravensRizwan100% (1)

- Pantene Case StudyDocument21 pagesPantene Case StudyMuhammad AreebNo ratings yet

- Background of The StudyDocument26 pagesBackground of The StudyNoel Bitancor100% (1)

- Projecting Cash FlowsDocument25 pagesProjecting Cash FlowsOana TrutaNo ratings yet

- FINANCIAL MARKETS AND INSTITUTIONS (AutoRecovered)Document8 pagesFINANCIAL MARKETS AND INSTITUTIONS (AutoRecovered)dickens omondiNo ratings yet

- SecondDocument49 pagesSecondGAURAV SHARMANo ratings yet

- Financial Management Chapter 10.2Document30 pagesFinancial Management Chapter 10.2CA Uma KrishnaNo ratings yet

- 10.7 Treasury Management: MeaningDocument30 pages10.7 Treasury Management: MeaningGAURAV KHERANo ratings yet

- Cash ManagementDocument32 pagesCash ManagementVijeshNo ratings yet

- Management of Funds Entire SubjectDocument85 pagesManagement of Funds Entire SubjectMir Wajahat Ali100% (1)

- ShrikantDocument12 pagesShrikantShri KaraleNo ratings yet

- Return To Table of Contents: Accountability Modules Management Objective (S) BackgroundDocument30 pagesReturn To Table of Contents: Accountability Modules Management Objective (S) BackgrounddkokkeNo ratings yet

- Management of CashDocument6 pagesManagement of CashVIVEKNo ratings yet

- A Study On Cash Mangement at Dabur India PVT LTDDocument25 pagesA Study On Cash Mangement at Dabur India PVT LTDSanthu SaravananNo ratings yet

- Hema Project Cash FlowDocument6 pagesHema Project Cash Flowkannan VenkatNo ratings yet

- Sheba University College Faculy of Business and Economics Department of AccountingDocument26 pagesSheba University College Faculy of Business and Economics Department of Accountingeyob negashNo ratings yet

- 1648 Taft Avenue Corner Pedro Gil Street Malate, City of Manila, PhilippinesDocument11 pages1648 Taft Avenue Corner Pedro Gil Street Malate, City of Manila, PhilippinesBenNo ratings yet

- Cash ManagementDocument30 pagesCash ManagementankitaNo ratings yet

- 08 - Chapter 2Document63 pages08 - Chapter 2haikalNo ratings yet

- Marketable SecuritiesDocument23 pagesMarketable SecuritiesSunitha KarthikNo ratings yet

- Chapter One: Investments and Capital Allocation Framework 1.1. The Investment Environment-An IntroductionDocument10 pagesChapter One: Investments and Capital Allocation Framework 1.1. The Investment Environment-An IntroductiontemedebereNo ratings yet

- 04 Chapter 1Document29 pages04 Chapter 1Prashank SaxenaNo ratings yet

- Financial Management FinalDocument198 pagesFinancial Management Finallovebassi100% (1)

- AccountingDocument19 pagesAccountingsemonNo ratings yet

- Financial Management ReviewDocument8 pagesFinancial Management Reviewkooruu22No ratings yet

- Running Head: Financial Management 1Document7 pagesRunning Head: Financial Management 1Walter WhiteNo ratings yet

- Solved Paper FSD-2010Document11 pagesSolved Paper FSD-2010Kiran SoniNo ratings yet

- Basics of Cash Management: For Financial Management and ReportingDocument42 pagesBasics of Cash Management: For Financial Management and ReportingCanMelah EmmyNo ratings yet

- The Role of Managerial Accounting: Managerial Finance Is The Branch of Finance That Concerns Itself With The ManagerialDocument5 pagesThe Role of Managerial Accounting: Managerial Finance Is The Branch of Finance That Concerns Itself With The ManagerialKhozem Kach'sNo ratings yet

- Financial Statement AnalysisDocument96 pagesFinancial Statement AnalysisArun Kumar100% (1)

- Mse 6203 - Corporate FinanceDocument18 pagesMse 6203 - Corporate FinanceSri VarriNo ratings yet

- Unit-5 MaterialDocument36 pagesUnit-5 Material19-R-0503 ManogjnaNo ratings yet

- IJCRT2107588Document7 pagesIJCRT2107588Janiel TiapesNo ratings yet

- A STUDY ON FINANCIAL PERFORMANCE OF HCL ProDocument26 pagesA STUDY ON FINANCIAL PERFORMANCE OF HCL Proshirley100% (1)

- A Framework For The Analysis of Financial FlexibilityDocument9 pagesA Framework For The Analysis of Financial FlexibilityEdwin GunawanNo ratings yet

- Introduction To FinanceDocument7 pagesIntroduction To FinanceজহিরুলইসলামশোভনNo ratings yet

- Chapter Ii - Theoretical BackgroundDocument17 pagesChapter Ii - Theoretical Backgroundpatil0055No ratings yet

- FinanceDocument117 pagesFinancenarendraidealNo ratings yet

- Analysis of Fund Flow StatementDocument85 pagesAnalysis of Fund Flow StatementBharath GowdaNo ratings yet

- Mcom 202Document26 pagesMcom 202vikasNo ratings yet

- Sanjana Project PDFDocument15 pagesSanjana Project PDFRahul KamathNo ratings yet

- Word Doc of CashDocument17 pagesWord Doc of CashHema SayamNo ratings yet

- Chapter 1 Working Capital Mangemnt (Repaired)Document20 pagesChapter 1 Working Capital Mangemnt (Repaired)rtNo ratings yet

- @final Thesis@Document305 pages@final Thesis@vvpatelNo ratings yet

- Management of CashDocument14 pagesManagement of Cashfrw dm100% (1)

- Introduction To Venture Capital:: 1.1 ConceptDocument53 pagesIntroduction To Venture Capital:: 1.1 ConceptKaran ChavanNo ratings yet

- Cash Flow Statement On KMBDocument86 pagesCash Flow Statement On KMBVeeresh PeddipathiNo ratings yet

- ICF Group 3 Working CapitalDocument130 pagesICF Group 3 Working CapitalAnkit KalraNo ratings yet

- Assessment One - Financial ManagementDocument10 pagesAssessment One - Financial Managementifras1343No ratings yet

- FM MbaDocument77 pagesFM Mbakamalyadav5907No ratings yet

- Accounting Research Topics and TitlesDocument4 pagesAccounting Research Topics and TitlesMitch Tokong MinglanaNo ratings yet

- On The Topic: Fund Flow Statement C.R.T-1Document7 pagesOn The Topic: Fund Flow Statement C.R.T-1Vinay Kumar TanguduNo ratings yet

- Fund Flow UppclDocument73 pagesFund Flow UppclTahir HussainNo ratings yet

- Chapter 6 Short Term FinancingDocument19 pagesChapter 6 Short Term FinancingInes MiladiNo ratings yet

- Features of The Financial System of DevelpoedDocument35 pagesFeatures of The Financial System of DevelpoedChahat PartapNo ratings yet

- Corporate FinanceDocument140 pagesCorporate FinanceGerald NjugunaNo ratings yet

- Financial Management Term PaperDocument28 pagesFinancial Management Term PaperBhavya NawalakhaNo ratings yet

- A Summer Training Project Report ON "Cash Flow Management of BSNL"Document51 pagesA Summer Training Project Report ON "Cash Flow Management of BSNL"Neha VidhaniNo ratings yet

- The Finace Master: What you Need to Know to Achieve Lasting Financial FreedomFrom EverandThe Finace Master: What you Need to Know to Achieve Lasting Financial FreedomNo ratings yet

- Discounted Cash Flow Budgeting: Simplified Your Path to Financial ExcellenceFrom EverandDiscounted Cash Flow Budgeting: Simplified Your Path to Financial ExcellenceNo ratings yet

- Ambit Strategy Thematic TenBaggers5 05jan2016 PDFDocument28 pagesAmbit Strategy Thematic TenBaggers5 05jan2016 PDFVikas TiwariNo ratings yet

- CV Ana GereaDocument3 pagesCV Ana GereaAnaNo ratings yet

- What Professional Service Firms Must Do To ThriveDocument19 pagesWhat Professional Service Firms Must Do To ThriveCaio LemosNo ratings yet

- Chapter 9 SolutionsDocument41 pagesChapter 9 SolutionsRodNo ratings yet

- Benefits of EDocument4 pagesBenefits of EMeenakshiParasharNo ratings yet

- Strategic Management Theory and Cases An Integrated Approach 12th Edition Hill Solutions ManualDocument51 pagesStrategic Management Theory and Cases An Integrated Approach 12th Edition Hill Solutions ManualDomingo Mckinney100% (31)

- Presentation On Traditional Marketing and Value Retention MarketingDocument18 pagesPresentation On Traditional Marketing and Value Retention Marketingscorpionking14No ratings yet

- Syllabus & Sap MM5003 - : Marketing ManagementDocument19 pagesSyllabus & Sap MM5003 - : Marketing ManagementTumpal SimatupangNo ratings yet

- Project 4 - Forecasting Financial StatementsDocument56 pagesProject 4 - Forecasting Financial StatementsTulasi ReddyNo ratings yet

- CF2 - Chapter 1 Cost of Capital - SVDocument58 pagesCF2 - Chapter 1 Cost of Capital - SVleducNo ratings yet

- The Study of Cash Flow Statement of Axis Bank For Period 2017-21Document11 pagesThe Study of Cash Flow Statement of Axis Bank For Period 2017-21Dnyandeep ManwarNo ratings yet

- Pricing Decision: Basic ConceptsDocument47 pagesPricing Decision: Basic ConceptssulukaNo ratings yet

- Jusco To Rebrand Itself As AEONDocument1 pageJusco To Rebrand Itself As AEONIsk TornadoNo ratings yet

- Material Requirements Planning (MRP)Document11 pagesMaterial Requirements Planning (MRP)ajeng.saraswatiNo ratings yet

- PM2 - The Marketing ProcessDocument41 pagesPM2 - The Marketing ProcessRHam VariasNo ratings yet

- Algorithmic Trading Directory 2010Document100 pagesAlgorithmic Trading Directory 201017524100% (4)

- CAPE Accounting 2014 U1 P2-2Document8 pagesCAPE Accounting 2014 U1 P2-2Shakita SamuelNo ratings yet

- 5 30 2022 6:15:45 PM PDFDocument3 pages5 30 2022 6:15:45 PM PDFThy TanaNo ratings yet

- Income Statement 1Document4 pagesIncome Statement 1Mhaye Aguinaldo0% (1)

- International Product PlanningDocument38 pagesInternational Product Planningsamrulezzz100% (16)

- Assignment 1 Eco-Asyiq, Azzim, Aqil, Aikal, FaizDocument10 pagesAssignment 1 Eco-Asyiq, Azzim, Aqil, Aikal, FaizAikal ZaharozeeNo ratings yet

- Report On Financial Analysis of National Buildings Construction Corporation Ltd. (NBCC) .Document19 pagesReport On Financial Analysis of National Buildings Construction Corporation Ltd. (NBCC) .arnabgogoiNo ratings yet

- Exploitation of New BusinessDocument2 pagesExploitation of New BusinessRai AhmedNo ratings yet

- Relative Valuation SESSION2Document57 pagesRelative Valuation SESSION2Heena AggarwalNo ratings yet

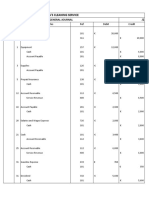

- Anya's Cleaning ServiceDocument22 pagesAnya's Cleaning ServiceArya HerdiansyahNo ratings yet

- Decision Analysis ch3Document2 pagesDecision Analysis ch3Mohan BishtNo ratings yet

- HorsefieldDocument2 pagesHorsefieldMarie Xavier - FelixNo ratings yet