You might also like

- Too Much Luck: The Mining Boom and Australia’s FutureFrom EverandToo Much Luck: The Mining Boom and Australia’s FutureRating: 3 out of 5 stars3/5 (1)

- Topic 2 - Australia's Place in The Global EconomyDocument11 pagesTopic 2 - Australia's Place in The Global EconomyedufocusedglobalNo ratings yet

- Economist Insights 10 December2Document2 pagesEconomist Insights 10 December2buyanalystlondonNo ratings yet

- Citic Draft Final Draft 10 Jan 2014Document14 pagesCitic Draft Final Draft 10 Jan 2014Ashwin ShrivastavaNo ratings yet

- Clase 7 - ActividadesDocument3 pagesClase 7 - ActividadesjuanpablofisicaroNo ratings yet

- Business in Canada ComsatsDocument17 pagesBusiness in Canada Comsatsfarhan harcho100% (1)

- PESTLE Analysis Example of AustraliaDocument12 pagesPESTLE Analysis Example of AustraliaNikita DakiNo ratings yet

- The Impact of Globalisation On The Australian EconomyDocument8 pagesThe Impact of Globalisation On The Australian EconomyEngr AtiqNo ratings yet

- Australia Commodities and Competitiveness - CaseStudyDocument2 pagesAustralia Commodities and Competitiveness - CaseStudyvishnuvrnNo ratings yet

- Deflation: Causes of InflationDocument4 pagesDeflation: Causes of InflationUpasana AroraNo ratings yet

- Weekly OverviewDocument3 pagesWeekly Overviewapi-150779697No ratings yet

- Deloitte - The East Eyes The West CoastDocument22 pagesDeloitte - The East Eyes The West CoastThe Vancouver SunNo ratings yet

- Position PaperDocument2 pagesPosition PaperMus'ab UsmanNo ratings yet

- Finnacial CrisiDocument5 pagesFinnacial Crisikarima salemNo ratings yet

- ASJ #2 May 2012Document60 pagesASJ #2 May 2012Alex SellNo ratings yet

- Terms of Reference: Sr. No Name Roll No. 1 2 3 4 5 6Document9 pagesTerms of Reference: Sr. No Name Roll No. 1 2 3 4 5 6wolverine987No ratings yet

- Australia's Trade and Financial FlowsDocument7 pagesAustralia's Trade and Financial Flowsatiggy05No ratings yet

- Australia To Benefit From China Ties For Some Time Yet: Economic Research NoteDocument2 pagesAustralia To Benefit From China Ties For Some Time Yet: Economic Research Notealan_s1No ratings yet

- Australian Securitisation Journal: TailorDocument60 pagesAustralian Securitisation Journal: TailorAlex SellNo ratings yet

- Margin - The Journal of Applied Economic Research-2010-Vines-157-75Document19 pagesMargin - The Journal of Applied Economic Research-2010-Vines-157-7525526No ratings yet

- Australia's Trade and Balance of PaymentsDocument34 pagesAustralia's Trade and Balance of PaymentsJackson BlackNo ratings yet

- Weekly OverviewDocument4 pagesWeekly Overviewapi-150779697No ratings yet

- Strategy Radar - 2012 - 1012 XX Potential Housing BubbleDocument2 pagesStrategy Radar - 2012 - 1012 XX Potential Housing BubbleStrategicInnovationNo ratings yet

- Sol-0298commerce AnswersDocument18 pagesSol-0298commerce AnswersicewallowhaNo ratings yet

- Gold Ex Plainer September 19 2010Document6 pagesGold Ex Plainer September 19 2010Radu LucaNo ratings yet

- Property Report MelbourneDocument0 pagesProperty Report MelbourneMichael JordanNo ratings yet

- Spring NewsletterDocument8 pagesSpring NewsletterWealthcare Financial SolutionsNo ratings yet

- China and Super: Big Changes Afoot by Robert Gottliebsen.Document4 pagesChina and Super: Big Changes Afoot by Robert Gottliebsen.AKFinancialPlanningNo ratings yet

- Economic Analysis Current Global Economy Scenario - Similar To Market Crash of 1929Document32 pagesEconomic Analysis Current Global Economy Scenario - Similar To Market Crash of 1929Jariwala BhaveshNo ratings yet

- 8-15-11 Steady As She GoesDocument3 pages8-15-11 Steady As She GoesThe Gold SpeculatorNo ratings yet

- Weekly CommentaryDocument4 pagesWeekly Commentaryapi-150779697No ratings yet

- 1-23-12 More QE On The WayDocument3 pages1-23-12 More QE On The WayThe Gold SpeculatorNo ratings yet

- AUSTRALIA - Porters 5 ForcesDocument14 pagesAUSTRALIA - Porters 5 ForcesSai Vasudevan100% (1)

- Australia Towards Globalization 2Document6 pagesAustralia Towards Globalization 2Arjay YsaacNo ratings yet

- Balance of Payments EssayDocument2 pagesBalance of Payments EssayKevin Nguyen100% (1)

- Investing in CommoditiesDocument2 pagesInvesting in CommoditiesAsim QaiserNo ratings yet

- QBAMCO - It's Time PDFDocument6 pagesQBAMCO - It's Time PDFplato363No ratings yet

- Topic: Financial Services - Banking Sector Industry/sector BackgroundDocument4 pagesTopic: Financial Services - Banking Sector Industry/sector Backgroundkanika agrawalNo ratings yet

- Who Owns Australia: Exposing The MultinationalsDocument24 pagesWho Owns Australia: Exposing The MultinationalsCSNo ratings yet

- Effects of A High CAD EssayDocument2 pagesEffects of A High CAD EssayfahoutNo ratings yet

- Economic AnalysisDocument10 pagesEconomic AnalysiswanderwithaishNo ratings yet

- Daily Reckoning Looming Aussie Recession PDFDocument11 pagesDaily Reckoning Looming Aussie Recession PDFMino Zo SydneyNo ratings yet

- ANZ China in FocusDocument31 pagesANZ China in FocusrguyNo ratings yet

- Strategy Radar 2012 0323 XX Mining BoomDocument3 pagesStrategy Radar 2012 0323 XX Mining BoomStrategicInnovationNo ratings yet

- Aus Japan Report FinalDocument32 pagesAus Japan Report FinalMasudRanaNo ratings yet

- Structure: Lewis: Chapter 1 - An Overview of The Australian EconomyDocument7 pagesStructure: Lewis: Chapter 1 - An Overview of The Australian Economydesidoll_92No ratings yet

- Economic Downturns and Business EnvironmentDocument5 pagesEconomic Downturns and Business EnvironmentJohn Michael MagpantayNo ratings yet

- Fin CrisesDocument4 pagesFin CriseshelperforeuNo ratings yet

- NYU Presentation 11 17 10 v3 - 0Document48 pagesNYU Presentation 11 17 10 v3 - 0Kevin CreaseyNo ratings yet

- Outlook 2011: Three Dominant Factors Will Impact Gold, Silver and Platinum in 2011Document16 pagesOutlook 2011: Three Dominant Factors Will Impact Gold, Silver and Platinum in 2011Khalid S. AlyahmadiNo ratings yet

- Economic Insight Report-24 Sept 15Document3 pagesEconomic Insight Report-24 Sept 15Anonymous hPUlIF6No ratings yet

- Presidential CaseDocument9 pagesPresidential CaseVilgia Delarhoza0% (1)

- Demand and Supply of Certain Resources in Australia and Factors Other Than Price Which Affect Demand and SupplyDocument6 pagesDemand and Supply of Certain Resources in Australia and Factors Other Than Price Which Affect Demand and Supplyfatemah zahidNo ratings yet

- AFR - Scott Powers InterviewDocument2 pagesAFR - Scott Powers Interviewkaren_cooper412No ratings yet

- Inside Australia: How Economic Reforms and Structure Affect BOPDocument2 pagesInside Australia: How Economic Reforms and Structure Affect BOPxxsunflowerxxNo ratings yet

- A Period of Consequence - How Abraaj Sees The World & Outlook, Dec 2008Document66 pagesA Period of Consequence - How Abraaj Sees The World & Outlook, Dec 2008Shirjeel NaseemNo ratings yet

- Watchdog April 1992Document68 pagesWatchdog April 1992Lynda BoydNo ratings yet

- 5 Reasons Why Gold Will RiseDocument1 page5 Reasons Why Gold Will RisejogalbhushanNo ratings yet

- Australia's R-Word - Rebalancing Not Recession PDFDocument24 pagesAustralia's R-Word - Rebalancing Not Recession PDFJames WoodsNo ratings yet

- CAD and External StabilityDocument4 pagesCAD and External Stabilityjonno100% (1)

- UntitledDocument2 pagesUntitledapi-90504428No ratings yet

- Media Release: The Hon Christopher Pyne MPDocument2 pagesMedia Release: The Hon Christopher Pyne MPapi-90504428No ratings yet

- For Immediate Release Statement From Jason Akermanis - Thursday 22 March 2012Document1 pageFor Immediate Release Statement From Jason Akermanis - Thursday 22 March 2012api-90504428No ratings yet

- Jimmy Barnes Announcement: Back On Deck in A Few Weeks Time."Document1 pageJimmy Barnes Announcement: Back On Deck in A Few Weeks Time."api-90504428No ratings yet

- CDR Sample For EADocument32 pagesCDR Sample For EARonald Shaikat HalderNo ratings yet

- Ausimm Register Members 102012Document287 pagesAusimm Register Members 102012Randy CavaleraNo ratings yet

- Victorian Rail Industry Operators' Group Standards (VRIOGS)Document1 pageVictorian Rail Industry Operators' Group Standards (VRIOGS)44934640% (1)

- Economy of AustraliaDocument4 pagesEconomy of AustraliaVarun KumarNo ratings yet

- ACAC Report 0810 - SMDocument84 pagesACAC Report 0810 - SMharshil84No ratings yet

- AUSTRALIA - Porters 5 ForcesDocument14 pagesAUSTRALIA - Porters 5 ForcesSai Vasudevan100% (1)

- Faculty of Business Manamgent & Globalization: International Economics Group AssignmentDocument6 pagesFaculty of Business Manamgent & Globalization: International Economics Group AssignmentDibya sahaNo ratings yet

- Jessica Bank StatementDocument8 pagesJessica Bank StatementJohn ReidNo ratings yet

- Week 12 Presentation Case ABC Learning PDFDocument12 pagesWeek 12 Presentation Case ABC Learning PDFNishat NabilaNo ratings yet

- Career FAQs - Accounting PDFDocument150 pagesCareer FAQs - Accounting PDFmaustroNo ratings yet

- 179.N.G.T. Travel Pty LTD ASICDocument1 page179.N.G.T. Travel Pty LTD ASICFlinders TrusteesNo ratings yet

- ON Report - 061114 - FNL PDFDocument84 pagesON Report - 061114 - FNL PDFFredNo ratings yet

- Financial of Apply Principle Task 1 ChangedDocument6 pagesFinancial of Apply Principle Task 1 ChangedHumayun KhanNo ratings yet

- Dy AustraliaDocument2 pagesDy AustraliaANDREA LOUISE ELCANONo ratings yet

- 002.LEVINE A: ASIC Personal Name ExtractDocument42 pages002.LEVINE A: ASIC Personal Name ExtractFlinders TrusteesNo ratings yet

- Week 10 - Tutorial QuestionsDocument7 pagesWeek 10 - Tutorial QuestionsLizNo ratings yet

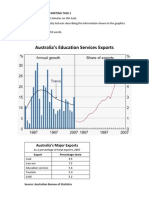

- IELTS Writing Task 1 Australian Education Exports With Sample EssayDocument2 pagesIELTS Writing Task 1 Australian Education Exports With Sample EssayJohn SalterNo ratings yet

- MWV Web ServicesDocument48 pagesMWV Web ServicesRathna SubbuNo ratings yet

- 1800 AU Public Companies - TRANSFER AGENT - 1800 MarieDocument72 pages1800 AU Public Companies - TRANSFER AGENT - 1800 MarieMarie Santos - Raymundo100% (1)

- TransactionSummary NovDocument6 pagesTransactionSummary NovCarlos SanabriaNo ratings yet

- Country Link NetworkDocument1 pageCountry Link NetworkAmit JoshiNo ratings yet

- Scoping Report - The Future Movement GroupDocument24 pagesScoping Report - The Future Movement Groupapi-524390944100% (1)

- Wiiklic Pty LTDDocument1 pageWiiklic Pty LTDapi-278870838No ratings yet

- CAD EssayDocument4 pagesCAD Essayshelterman14No ratings yet

- Statements 20230714Document6 pagesStatements 20230714Sima KadirNo ratings yet

- Foreign Investment and Australian AgricultureDocument60 pagesForeign Investment and Australian AgricultureABC News OnlineNo ratings yet

- VOIP New Call Rates PDFDocument285 pagesVOIP New Call Rates PDFMalvin RitoNo ratings yet

- 12-Month NBN Rollout PlanDocument2 pages12-Month NBN Rollout PlanJames HutchinsonNo ratings yet

- Ws Num LCM HCF 01QA PWDocument2 pagesWs Num LCM HCF 01QA PWdeyaa1000000No ratings yet

- EQ Holdings 09Document48 pagesEQ Holdings 09Frode HaukenesNo ratings yet