You might also like

- Stephanie Bank StatementDocument14 pagesStephanie Bank StatementAnonymous SZFPoV100% (4)

- EP2EMV+Multi Custom+12 11 2009Document187 pagesEP2EMV+Multi Custom+12 11 2009MohitNo ratings yet

- Buyers Credit: NOTE-Nostro Account Is An Account of An Indian Bank With A Bank Outside India in Foreign CurrencyDocument14 pagesBuyers Credit: NOTE-Nostro Account Is An Account of An Indian Bank With A Bank Outside India in Foreign Currencyshubh92No ratings yet

- Int RemittanceDocument7 pagesInt Remittanceግሩም ሽ.No ratings yet

- Topic 5 - International Fund TransferDocument14 pagesTopic 5 - International Fund TransferdyingwithoutuNo ratings yet

- Study On Foreign Exchange Remittances & Interbank DealingsDocument95 pagesStudy On Foreign Exchange Remittances & Interbank DealingsSachin KajaveNo ratings yet

- DEFINITION of 'Savings Account': Deposit Interest RateDocument4 pagesDEFINITION of 'Savings Account': Deposit Interest Ratemuyi kunleNo ratings yet

- Letter of CreditDocument15 pagesLetter of CreditShahbaz ArtsNo ratings yet

- RemittanceDocument21 pagesRemittancemuhammad arifNo ratings yet

- Outward RemittanceDocument49 pagesOutward Remittancemanishjethva2009No ratings yet

- RTGSDocument14 pagesRTGSHarshUpadhyayNo ratings yet

- Schedule of ChargesDocument14 pagesSchedule of ChargeskrishmasethiNo ratings yet

- SCL I Letters of CreditDocument4 pagesSCL I Letters of CreditTerence Valdehueza100% (1)

- Demand Promissory Note PDFDocument1 pageDemand Promissory Note PDFDexter Chua100% (1)

- Macm-R000000001 Affidavit of Ucc1 Conns Home Plus - Synchrony Bank - Georgia CorporationsDocument5 pagesMacm-R000000001 Affidavit of Ucc1 Conns Home Plus - Synchrony Bank - Georgia CorporationsKing ElNo ratings yet

- Definition of 'Credit': Joana Rey P. Palabyab Credit and Collection BSBM - Fm3A Ms. Luisita MarzanDocument3 pagesDefinition of 'Credit': Joana Rey P. Palabyab Credit and Collection BSBM - Fm3A Ms. Luisita MarzanJoana Rey PalabyabNo ratings yet

- Revised PRA Remittance Instruction Form 1Document1 pageRevised PRA Remittance Instruction Form 1Menchie Ann Sabandal SalinasNo ratings yet

- Wire Transfer AgreementDocument9 pagesWire Transfer AgreementmeariclusNo ratings yet

- Modele Lettre enDocument8 pagesModele Lettre entamer abdelhady100% (1)

- Life After Debt - Debtless by 2012, The U.S and The World Without US Treasury Bonds (FOIA Document)Document43 pagesLife After Debt - Debtless by 2012, The U.S and The World Without US Treasury Bonds (FOIA Document)Ephraim DavisNo ratings yet

- Econ Notes 3Document13 pagesEcon Notes 3Engineers UniqueNo ratings yet

- Banking Products and ServicesDocument13 pagesBanking Products and ServicesDharmeshParikhNo ratings yet

- Banking MaterialDocument87 pagesBanking Materialmuttu&moonNo ratings yet

- Elements of Banking & InsuranceDocument77 pagesElements of Banking & InsuranceMADHULIKAANo ratings yet

- Policy Fund Withdrawal Form: FWP/FSC CodeDocument2 pagesPolicy Fund Withdrawal Form: FWP/FSC CodeEra gasperNo ratings yet

- Instruments For Financing Working CapitalDocument6 pagesInstruments For Financing Working CapitalPra SonNo ratings yet

- Promissory Note: Borrower: LenderDocument1 pagePromissory Note: Borrower: LenderAmis SteigerNo ratings yet

- Your Deposit Account Agreement: Effective May 11, 2020Document33 pagesYour Deposit Account Agreement: Effective May 11, 2020Steph BryattNo ratings yet

- Foreign Remittances - Inward and OutwardDocument54 pagesForeign Remittances - Inward and OutwardShehabziaNo ratings yet

- Demat AccountDocument8 pagesDemat Account29.Kritika SinghNo ratings yet

- Ais FormsDocument2 pagesAis FormsChris LampleyNo ratings yet

- Overview of The Federal DebtDocument27 pagesOverview of The Federal DebtChuck AchbergerNo ratings yet

- Overview-US Payment Systems 5122019 313PMDocument16 pagesOverview-US Payment Systems 5122019 313PMMartin HardingNo ratings yet

- Discount Window: Rate, or Rate, and Is Separate and Distinct From TheDocument4 pagesDiscount Window: Rate, or Rate, and Is Separate and Distinct From TheDisgruntled BorrowerNo ratings yet

- Sample Sa: Escrow AgreementDocument4 pagesSample Sa: Escrow AgreementEins BalagtasNo ratings yet

- VN 04 Credit Cards FaqDocument5 pagesVN 04 Credit Cards FaqdhakaeurekaNo ratings yet

- Important Banking GK PDFDocument26 pagesImportant Banking GK PDFPriya BanothNo ratings yet

- ICE CDS White PaperDocument21 pagesICE CDS White PaperRajat SharmaNo ratings yet

- Letters of CreditDocument24 pagesLetters of CreditRounaq DharNo ratings yet

- CompendiumDocument18 pagesCompendiumpranithroyNo ratings yet

- Remittances - DD, Pay Order, Mail Transfer, SWIFT, Travelers ChequesDocument20 pagesRemittances - DD, Pay Order, Mail Transfer, SWIFT, Travelers Chequeskaramdeep26No ratings yet

- Foreign Exchange Business of Sonali BankDocument51 pagesForeign Exchange Business of Sonali BankHimadri HimuNo ratings yet

- CH 1 - Scope of International FinanceDocument7 pagesCH 1 - Scope of International Financepritesh_baidya269100% (3)

- (Insert Your Firm's Name Here) : Guide FromDocument5 pages(Insert Your Firm's Name Here) : Guide FromHussein SeetalNo ratings yet

- Form of Bailee Letter (Warehouse Bank) Exhibit III-35 (Cash Purchase) FORM OF BAILEE LETTER (Warehouse Bank) (Cash Purchase)Document3 pagesForm of Bailee Letter (Warehouse Bank) Exhibit III-35 (Cash Purchase) FORM OF BAILEE LETTER (Warehouse Bank) (Cash Purchase)Valerie Lopez100% (1)

- Dimensions of Cash Flow Management: Prof. N. C. KarDocument74 pagesDimensions of Cash Flow Management: Prof. N. C. KarAshokNo ratings yet

- Foreign Remittance of DBBLDocument57 pagesForeign Remittance of DBBLtariqul21100% (1)

- International Banking SystemDocument24 pagesInternational Banking SystemSukumar Nandi100% (9)

- Am L Sample PolicyDocument9 pagesAm L Sample PolicywilliamhancharekNo ratings yet

- Nmims Sec A Test No 1Document6 pagesNmims Sec A Test No 1ROHAN DESAI100% (1)

- Assignment ON Bills DiscountingDocument9 pagesAssignment ON Bills DiscountingparuljainibmrNo ratings yet

- Assignment Retail BankingDocument3 pagesAssignment Retail BankingSNEHA MARIYAM VARGHESE SIM 16-18No ratings yet

- About Rtgs & NeftDocument5 pagesAbout Rtgs & NeftAbdulhussain JariwalaNo ratings yet

- Chapter 05 Power PointDocument31 pagesChapter 05 Power PointmuluNo ratings yet

- What Is An RFC Savings Account? Why Choose An RFC Savings Account?Document6 pagesWhat Is An RFC Savings Account? Why Choose An RFC Savings Account?Prachikarambelkar100% (1)

- Reinstatement FormDocument2 pagesReinstatement FormNikken, Inc.No ratings yet

- Typesofletterofcreditson11092012 150108023810 Conversion Gate01Document126 pagesTypesofletterofcreditson11092012 150108023810 Conversion Gate01bushra umerNo ratings yet

- Standing Order FormDocument3 pagesStanding Order FormMaissa Hassan100% (1)

- Features of Credit CardDocument11 pagesFeatures of Credit CardBipin ThakorNo ratings yet

- Presentation On Financial InstrumentsDocument20 pagesPresentation On Financial InstrumentsMehak BhallaNo ratings yet

- Constitution of the State of Minnesota — 1876 VersionFrom EverandConstitution of the State of Minnesota — 1876 VersionNo ratings yet

- Naked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsFrom EverandNaked Guide to Bonds: What You Need to Know -- Stripped Down to the Bare EssentialsNo ratings yet

- Q"fffi: "Rfu CRRLFL Q$FTDocument5 pagesQ"fffi: "Rfu CRRLFL Q$FTHumayun KabirNo ratings yet

- Math JokesDocument21 pagesMath Jokesakther_aisNo ratings yet

- Basics of DepreciationDocument4 pagesBasics of Depreciationakther_aisNo ratings yet

- GK 20.03Document2 pagesGK 20.03akther_aisNo ratings yet

- For Payment From July 2005 OnwardsDocument1 pageFor Payment From July 2005 Onwardsvijay123*75% (4)

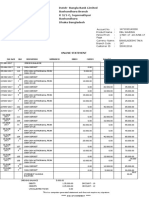

- Dutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshDocument2 pagesDutch-Bangla Bank Limited Bashundhara Branch K 3/1-C, Jogonnathpur Bashundhara Dhaka BangladeshNur NobiNo ratings yet

- Note 500 RsDocument2 pagesNote 500 Rsranjit_more22683No ratings yet

- Chapter 16Document25 pagesChapter 16Saima IkramNo ratings yet

- ICICI 7P'sDocument15 pagesICICI 7P'sdheeraj422No ratings yet

- 3rd Jan - 2nd FebDocument4 pages3rd Jan - 2nd FebPrajakta JoshiNo ratings yet

- Presentation 1 - Introduction To Money, Credit, and BankingDocument28 pagesPresentation 1 - Introduction To Money, Credit, and BankingNigel N. SilvestreNo ratings yet

- Khel Maharan Teacher NameDocument6 pagesKhel Maharan Teacher NameZalorthang ZateNo ratings yet

- WTC2014 NRL80%HSBCLondonDocument11 pagesWTC2014 NRL80%HSBCLondonMarcus StevensNo ratings yet

- Business TranslationDocument154 pagesBusiness TranslationBdour AlfalahNo ratings yet

- India Case StudyDocument4 pagesIndia Case StudyMakame Mahmud DiptaNo ratings yet

- FNB Aspire AccountDocument44 pagesFNB Aspire Accountjessicaheyns5No ratings yet

- Bank CRG ScoreSheetDocument3 pagesBank CRG ScoreSheetMd. Zubaer100% (1)

- Export Finance (Case Study Need To Be Added)Document62 pagesExport Finance (Case Study Need To Be Added)rupalNo ratings yet

- Account Statement From 1 May 2021 To 16 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument10 pagesAccount Statement From 1 May 2021 To 16 Aug 2021: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceLoan LoanNo ratings yet

- CMDocument84 pagesCMMuhammad NiazNo ratings yet

- Nepal Bank Limited: Summer Training Project Report ON "Deposit Schemes of Nepal Bank"Document61 pagesNepal Bank Limited: Summer Training Project Report ON "Deposit Schemes of Nepal Bank"Aditya VermaNo ratings yet

- Using Technology To Generate An Amortization Table: InquireDocument5 pagesUsing Technology To Generate An Amortization Table: InquireAdam MikitzelNo ratings yet

- FAQsDocument20 pagesFAQsThobib OtaiNo ratings yet

- ST Aloysius College (Autonomous) Mangaluru I Internal Exam - July 2019 B.B.A. - Semester I Financial Accounting - IDocument3 pagesST Aloysius College (Autonomous) Mangaluru I Internal Exam - July 2019 B.B.A. - Semester I Financial Accounting - IAnanth RohithNo ratings yet

- Negotiable Instrument NotesDocument5 pagesNegotiable Instrument NotesJoshua UmaliNo ratings yet

- Additional Legal Opinion of Nafeesa PDFDocument6 pagesAdditional Legal Opinion of Nafeesa PDFRaghavendra Prabhu100% (1)

- Sample Answer & Affirmative Defenses Against Fannie MaeDocument6 pagesSample Answer & Affirmative Defenses Against Fannie MaeChristine HecklerNo ratings yet

- World BankDocument13 pagesWorld BankSanskar YadavNo ratings yet

- Shri BasaveshwarDocument2 pagesShri Basaveshwarvikatit solutionsNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument3 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceRithvik MallikarjunaNo ratings yet

- Comprehensive Illustrative ProblemDocument2 pagesComprehensive Illustrative ProblemLyssa Marie Avenido GuelosNo ratings yet

- N SpecDocument61 pagesN SpecJonathan GalorioNo ratings yet