You might also like

- Auditing As An Aid To Accountability in The Public SectorDocument47 pagesAuditing As An Aid To Accountability in The Public SectorDaniel Obasi100% (2)

- Finance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersFrom EverandFinance for Nonfinancial Managers: A Guide to Finance and Accounting Principles for Nonfinancial ManagersNo ratings yet

- Chapter 1Document10 pagesChapter 1Салтанат МакажановаNo ratings yet

- Century Bank - I II IIIDocument33 pagesCentury Bank - I II IIIMADHU KHANALNo ratings yet

- Chapter 1 - AACA P1Document7 pagesChapter 1 - AACA P1Toni Rose Hernandez LualhatiNo ratings yet

- Essay On AuditingDocument9 pagesEssay On AuditingAtis Madri AmandaNo ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- Effects of Credit Management On The Profitability of Small and Medium Enterprices in KitaleDocument7 pagesEffects of Credit Management On The Profitability of Small and Medium Enterprices in KitaleElias NgeiywaNo ratings yet

- June 2016: BY: ZEWGE DANIAL R/2221/06 Advisor: Abdul Walli (Ba)Document30 pagesJune 2016: BY: ZEWGE DANIAL R/2221/06 Advisor: Abdul Walli (Ba)Reta TolesaNo ratings yet

- Axis Bank NPADocument101 pagesAxis Bank NPAArun SavukarNo ratings yet

- AbstractDocument13 pagesAbstractKhooshal Yadhav RamphulNo ratings yet

- Contemporary Issues in Finance - International Aspects of Corporate Finance - Jerralyn AlvaDocument5 pagesContemporary Issues in Finance - International Aspects of Corporate Finance - Jerralyn AlvaJERRALYN ALVANo ratings yet

- ALM Management in Icici BankDocument85 pagesALM Management in Icici BankSrikanth BheemsettiNo ratings yet

- The Effect of Client Appraisal On The Efficiency of Micro Finance BankDocument13 pagesThe Effect of Client Appraisal On The Efficiency of Micro Finance BankaijbmNo ratings yet

- Auditing I-Chapter 1 MLCDocument13 pagesAuditing I-Chapter 1 MLCHilew TSegayeNo ratings yet

- Assessment of Account Receivable Management (In Case of Moringa Soft Drinks) Riftvalley UniversityDocument24 pagesAssessment of Account Receivable Management (In Case of Moringa Soft Drinks) Riftvalley UniversityReta TolesaNo ratings yet

- Corporate Governance - An Introduction: Chapter-IDocument43 pagesCorporate Governance - An Introduction: Chapter-IFalakNo ratings yet

- Solution Manual For Financial Accounting in An Economic Context 10th Edition Pratt PetersDocument6 pagesSolution Manual For Financial Accounting in An Economic Context 10th Edition Pratt PetersEdna Steward100% (43)

- FSA Group AssDocument16 pagesFSA Group AssFirdows SuleymanNo ratings yet

- Bank Reconciliation Statements, Accountability and Profitability of Small Business OrganisationDocument10 pagesBank Reconciliation Statements, Accountability and Profitability of Small Business OrganisationSalla CheaclyNo ratings yet

- Non Performing Assets in Allahabad Bank MBA Banking ProjectsDocument68 pagesNon Performing Assets in Allahabad Bank MBA Banking Projectsmallikarjun nayak50% (2)

- Chapter One Accounting Principles and Professional PracticeDocument22 pagesChapter One Accounting Principles and Professional PracticeHussen Abdulkadir100% (1)

- Ethical issues in private banks of PakistanDocument5 pagesEthical issues in private banks of PakistanRajib RoyNo ratings yet

- Slide Presentasi Ketua KNKG - Kuliah Umum UMS (Juni 2023)Document41 pagesSlide Presentasi Ketua KNKG - Kuliah Umum UMS (Juni 2023)Wahyu Sekar WijayaningtyasNo ratings yet

- Audit and Review: Exam FocusDocument12 pagesAudit and Review: Exam FocusPhebieon MukwenhaNo ratings yet

- AAS CH1 2 1 - MergedDocument19 pagesAAS CH1 2 1 - MergedRoel PaisteNo ratings yet

- Non Performing Assets in Allahabad BankDocument69 pagesNon Performing Assets in Allahabad BankGotham RamNo ratings yet

- Credit Risk Management in Karnataka State Credit Risk Management in Karnataka StateDocument98 pagesCredit Risk Management in Karnataka State Credit Risk Management in Karnataka StatePrashanth PBNo ratings yet

- BC PreExploration Oct09Document48 pagesBC PreExploration Oct09Prashant KhadeNo ratings yet

- 15 - Chapter 6 PDFDocument30 pages15 - Chapter 6 PDFRukminiNo ratings yet

- 214-Kotak Bank-Non Performing Assets at Kotak Mahindra BankDocument70 pages214-Kotak Bank-Non Performing Assets at Kotak Mahindra BankPeacock Live ProjectsNo ratings yet

- Meaning of Islamic AccountingDocument19 pagesMeaning of Islamic Accountingturk66650% (2)

- A Study On Financial Performance Analysis For Sri Murugan CreditsDocument59 pagesA Study On Financial Performance Analysis For Sri Murugan CreditsJayaprabhu PrabhuNo ratings yet

- CHAPTER 1 (Under Revision Wahahaha) The Problem and Its BackgroundDocument6 pagesCHAPTER 1 (Under Revision Wahahaha) The Problem and Its BackgroundAira TantoyNo ratings yet

- Icici Bank ProjectDocument82 pagesIcici Bank ProjectiamdarshandNo ratings yet

- Financial Statement Analysis of Madhucon ProjectsDocument8 pagesFinancial Statement Analysis of Madhucon Projectsmohammed khayyumNo ratings yet

- Final Financial Assessment - 2023Document9 pagesFinal Financial Assessment - 2023Weldu GebruNo ratings yet

- Tabarsum NON PERFORMING ASSETS AXIS BANKDocument73 pagesTabarsum NON PERFORMING ASSETS AXIS BANKSagar Paul'g100% (4)

- Reaction Paper On Ethical Issues in AccountingDocument4 pagesReaction Paper On Ethical Issues in AccountingJessica Rabo100% (1)

- Irma Kasri Dan N. LukviarmanDocument29 pagesIrma Kasri Dan N. Lukviarmanjaharuddin.hannoverNo ratings yet

- Importanct of Audit in Corporate FirmsDocument32 pagesImportanct of Audit in Corporate FirmssmartlordartNo ratings yet

- A Study On The Effectiveness of Remedies AvailableDocument35 pagesA Study On The Effectiveness of Remedies AvailableMitali ChaureNo ratings yet

- CreditDocument37 pagesCreditpetalingstreetNo ratings yet

- Critical Financial Review: Understanding Corporate Financial InformationFrom EverandCritical Financial Review: Understanding Corporate Financial InformationNo ratings yet

- Chapter One: 1.1. Back Ground of The StudyDocument46 pagesChapter One: 1.1. Back Ground of The StudyBobasa S AhmedNo ratings yet

- Rabin Dissertation 2019Document57 pagesRabin Dissertation 2019Rabindra paridaNo ratings yet

- Chapter - 01: Intern Report On Evaluation of Job Satisfication of Social Islami Bank LimitedDocument73 pagesChapter - 01: Intern Report On Evaluation of Job Satisfication of Social Islami Bank LimitedRedwan FerdousNo ratings yet

- Limitations of Balance SheetDocument6 pagesLimitations of Balance Sheetshoms_007No ratings yet

- Isbf - Research Paper - 2021Document22 pagesIsbf - Research Paper - 2021Hurmat Ayub SardarNo ratings yet

- Effect of NPAs on profitability of public sector banksDocument12 pagesEffect of NPAs on profitability of public sector banksVishesh SharmaNo ratings yet

- 13 - Summary Findings and ConclusionDocument9 pages13 - Summary Findings and ConclusionUtkarsh BajpaiNo ratings yet

- 4.inter Journal Macro - Micro-Factors-Affecting-the-Bad-Debt-of-Commercial-Banks-in-Ho-Chi-Minh-City-dikonversiDocument27 pages4.inter Journal Macro - Micro-Factors-Affecting-the-Bad-Debt-of-Commercial-Banks-in-Ho-Chi-Minh-City-dikonversilisa amaliaNo ratings yet

- Chapter 1 AuditDocument13 pagesChapter 1 AuditMisshtaC100% (1)

- Solutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsDocument26 pagesSolutions For Chapter 1 Auditing: Integral To The Economy: Review QuestionsStefany Mie MosendeNo ratings yet

- Uti BankDocument86 pagesUti BankMohit kolliNo ratings yet

- General Questions 4.0Document8 pagesGeneral Questions 4.0Benzon Agojo OndovillaNo ratings yet

- Compilation ReportDocument4 pagesCompilation ReportFlorivee EreseNo ratings yet

- Firms cannot use deceased partners' namesDocument2 pagesFirms cannot use deceased partners' namesSharon G. BalingitNo ratings yet

- RRB Exam Previous Year ModelDocument3 pagesRRB Exam Previous Year ModelShijumon XavierNo ratings yet

- Companies ListDocument83 pagesCompanies ListVamsi Hashmi0% (1)

- Kap 4 Parimet EkontabilitetitDocument18 pagesKap 4 Parimet EkontabilitetitEdmond KeraNo ratings yet

- Subic Bay Trading Company ProfileDocument4 pagesSubic Bay Trading Company ProfileNaomi Gimenez BisnarNo ratings yet

- GM - OEM Quick Reference Guide - Dec2016 1 PDFDocument2 pagesGM - OEM Quick Reference Guide - Dec2016 1 PDFSelvaraj Simiyon0% (1)

- NO Company NameDocument26 pagesNO Company Namepravinpatil4643No ratings yet

- G.R. No. L-22493 - Island Sales, Inc. VDocument4 pagesG.R. No. L-22493 - Island Sales, Inc. Vabc defNo ratings yet

- 73ac4horizontal & Vertical IntegrationDocument5 pages73ac4horizontal & Vertical IntegrationOjasvee KhannaNo ratings yet

- Venture Capital Firms, Finance Companies, and Financial Conglomerates ExplainedDocument8 pagesVenture Capital Firms, Finance Companies, and Financial Conglomerates ExplainedShuvro Rahman75% (12)

- Gravita Corporate Presentation - 2017 PDFDocument32 pagesGravita Corporate Presentation - 2017 PDFPALRAJ100% (1)

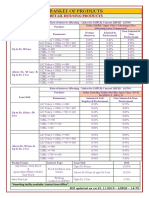

- BASKET OF RETAIL PRODUCTS RATESDocument3 pagesBASKET OF RETAIL PRODUCTS RATESVirendra K VermaNo ratings yet

- Thirdpartyrep Brand Guide 052314Document39 pagesThirdpartyrep Brand Guide 052314Tasfin HabibNo ratings yet

- Tvs Motor Company LimitedDocument4 pagesTvs Motor Company LimitedSiddu KambleNo ratings yet

- Production Cost Management & MIS FormulationDocument23 pagesProduction Cost Management & MIS FormulationSrikanth Kumar KonduriNo ratings yet

- CadburyDocument11 pagesCadburyAnkita RajNo ratings yet

- Audit Procedures For CashDocument24 pagesAudit Procedures For CashGizel Baccay100% (1)

- Class 12 Cbse Accountancy Sample Paper 2012 Model 2Document20 pagesClass 12 Cbse Accountancy Sample Paper 2012 Model 2Sunaina RawatNo ratings yet

- Intermediate Accounting I IntroductionDocument6 pagesIntermediate Accounting I IntroductionJoovs JoovhoNo ratings yet

- Financial DocsDocument6 pagesFinancial DocsMaryroseNo ratings yet

- Tutorial 1 Q ADocument5 pagesTutorial 1 Q AKelvin LeongNo ratings yet

- HANSSON CASE Individual AssignmentDocument2 pagesHANSSON CASE Individual AssignmentWawerudasNo ratings yet

- Moschino - Hermes - Comparative Positioning and Consumer Analysis - Dorothy Arhin - AcademiaDocument18 pagesMoschino - Hermes - Comparative Positioning and Consumer Analysis - Dorothy Arhin - AcademiaEnt Qa NepalNo ratings yet

- Fake Nigerian Offer For Petrol IPCCDocument16 pagesFake Nigerian Offer For Petrol IPCCDani NIANGNo ratings yet

- Request For Quotation (RFQ) : Form-ADocument5 pagesRequest For Quotation (RFQ) : Form-ADayanandSonawaneNo ratings yet

- Finance and the Multinational Firm: The New Role of Firms AbroadDocument13 pagesFinance and the Multinational Firm: The New Role of Firms AbroadFatin AfifaNo ratings yet

- Investment Banking Project ReportDocument84 pagesInvestment Banking Project ReportSohail Shaikh64% (14)

- Atlas Copco and Sandvik Shank Adapter GuideDocument11 pagesAtlas Copco and Sandvik Shank Adapter GuideSubhash KediaNo ratings yet

- Saln 2012 Blank FormDocument3 pagesSaln 2012 Blank FormGel KorlanNo ratings yet