You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Basic Financial Econometrics PDFDocument167 pagesBasic Financial Econometrics PDFdanookyereNo ratings yet

- Newtech Advant Business Plan9 PDFDocument38 pagesNewtech Advant Business Plan9 PDFdanookyereNo ratings yet

- BoA CFE-CMStatistics 2017 PDFDocument272 pagesBoA CFE-CMStatistics 2017 PDFdanookyereNo ratings yet

- Customer Satisfaction Theories PDFDocument34 pagesCustomer Satisfaction Theories PDFdanookyereNo ratings yet

- Joshua 1:9: Bible Quotations For The Bible Reading MarathonDocument5 pagesJoshua 1:9: Bible Quotations For The Bible Reading MarathondanookyereNo ratings yet

- Consumer Buying DecisionsDocument2 pagesConsumer Buying DecisionsdanookyereNo ratings yet

- The Role of Communication in Contemporary MarketingDocument4 pagesThe Role of Communication in Contemporary MarketingdanookyereNo ratings yet

- Importance of A Trial BalanceDocument1 pageImportance of A Trial Balancedanookyere100% (3)

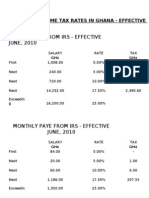

- Personal Income Tax Rates in GhanaDocument2 pagesPersonal Income Tax Rates in GhanadanookyereNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Practice Skills Assessment Type ADocument13 pagesPractice Skills Assessment Type Asybell8No ratings yet

- Ghaziabad - 7503448221 - Call Girls in Noida Sector 62Document1 pageGhaziabad - 7503448221 - Call Girls in Noida Sector 62Rahul SharmaNo ratings yet

- Theory and Practice in Language StudiesDocument170 pagesTheory and Practice in Language StudiesHossam Abd-ElghafarNo ratings yet

- E-Goverment Opportunities and ChallengesDocument24 pagesE-Goverment Opportunities and ChallengesMikaye WrightNo ratings yet

- Century Plan BrochureDocument28 pagesCentury Plan Brochuresandeepgiri71No ratings yet

- Tendernotice - 1 (4) 638043623175233354Document5 pagesTendernotice - 1 (4) 638043623175233354Ar Shubham KumarNo ratings yet

- Community Participation in Development ProjectsDocument52 pagesCommunity Participation in Development ProjectsRuby GarciaNo ratings yet

- IBT Sample Paper Grade 6 EnglishDocument7 pagesIBT Sample Paper Grade 6 Englishppats50% (10)

- Etoken Anywhere 8.1 Admin Guide Rev ADocument101 pagesEtoken Anywhere 8.1 Admin Guide Rev Atall27100% (1)

- Nicomachean Ethics AristotleDocument14 pagesNicomachean Ethics AristotleNathaniel BaldevinoNo ratings yet

- (Routledge Research in Higher Education) Jenny L. Small - Critical Religious Pluralism in Higher Education - A Social Justice Framework To Support Religious Diversity-Routledge (2020)Document105 pages(Routledge Research in Higher Education) Jenny L. Small - Critical Religious Pluralism in Higher Education - A Social Justice Framework To Support Religious Diversity-Routledge (2020)yakadimaya43No ratings yet

- Wasilah DoaDocument1 pageWasilah DoaFiqhiFajarNo ratings yet

- Mif M3Document32 pagesMif M3MorvinNo ratings yet

- RF 4cs of 432nd TRWDocument25 pagesRF 4cs of 432nd TRWpepepatosNo ratings yet

- Lis Rhodes - Whose HistoryDocument4 pagesLis Rhodes - Whose HistoryevaNo ratings yet

- G.R. No. 122058. May 5, 1999 Ignacio R. Bunye Vs SandiganbayanDocument2 pagesG.R. No. 122058. May 5, 1999 Ignacio R. Bunye Vs SandiganbayanDrimtec TradingNo ratings yet

- Computer Forensics - An: Jau-Hwang Wang Central Police University Tao-Yuan, TaiwanDocument27 pagesComputer Forensics - An: Jau-Hwang Wang Central Police University Tao-Yuan, TaiwanDESTROYERNo ratings yet

- "Successful Gigging and Freelancing": by Dr. Adrian DalyDocument12 pages"Successful Gigging and Freelancing": by Dr. Adrian DalyKevinPaceNo ratings yet

- Medieval MusicDocument25 pagesMedieval MusicMis Gloria83% (6)

- Tampuhan PaintingDocument2 pagesTampuhan PaintingtstbobbyvincentbentulanNo ratings yet

- LESSON 1 - Geographic Linguistic and Ethnic Dimensions of Philippine Literary History From Pre Colonial To The ContemporaryDocument86 pagesLESSON 1 - Geographic Linguistic and Ethnic Dimensions of Philippine Literary History From Pre Colonial To The ContemporaryJuryz PinedaNo ratings yet

- HR Audit ChecklistDocument4 pagesHR Audit Checklistpielzapa50% (2)

- GladiatorDocument1 pageGladiatorRohith KumarNo ratings yet

- Members Group: Indah Rahmadini M.Isra Nurcahya Koncoro Marsyandha WidyanurrahmahDocument11 pagesMembers Group: Indah Rahmadini M.Isra Nurcahya Koncoro Marsyandha WidyanurrahmahkeringNo ratings yet

- Tugas KevinDocument3 pagesTugas KevinSherlyta AlexandraNo ratings yet

- ResearchDocument8 pagesResearchMitchele Piamonte MamalesNo ratings yet

- Narmada Bachao AndolanDocument12 pagesNarmada Bachao AndolanAryan SinghNo ratings yet

- Therapeutic Relationship - 2Document45 pagesTherapeutic Relationship - 2Zaraki yami100% (1)

- Life Cycle Assessment of Electricity Generation in Mauritius - SIMAPRO PDFDocument11 pagesLife Cycle Assessment of Electricity Generation in Mauritius - SIMAPRO PDFLeonardo Caldas100% (1)

- Ajahn Brahm Ups and Downs in LifeDocument16 pagesAjahn Brahm Ups and Downs in LifeTomas GenevičiusNo ratings yet