You might also like

- Motion For Approval of Settlement in Lerman v. AppleDocument29 pagesMotion For Approval of Settlement in Lerman v. AppleMacRumorsNo ratings yet

- Alfa Bank FilingDocument27 pagesAlfa Bank FilingChuck RossNo ratings yet

- InjunctionDocument45 pagesInjunctionMartin Austermuhle75% (4)

- United States Court of Appeals For The District of Columbia CircuitDocument33 pagesUnited States Court of Appeals For The District of Columbia CircuitChris100% (2)

- SEC Reply Hodges Apr 30Document35 pagesSEC Reply Hodges Apr 30glimmertwins100% (1)

- SEC Reply Hodges Apr 30Document35 pagesSEC Reply Hodges Apr 30glimmertwins100% (1)

- United States Court of Appeals For The Sixth Circuit: CASE NO. 22-3702Document72 pagesUnited States Court of Appeals For The Sixth Circuit: CASE NO. 22-3702ChrisNo ratings yet

- Opposition To Motion For InjunctionDocument29 pagesOpposition To Motion For InjunctionBasseemNo ratings yet

- Transport RoomDocument10 pagesTransport RoomglimmertwinsNo ratings yet

- Practice Situational Judgement Test: Answers and Candidate Guidance BookletDocument29 pagesPractice Situational Judgement Test: Answers and Candidate Guidance BookletAdnan Aziz80% (5)

- United States Court of Appeals For The Sixth Circuit: CASE NO. 22-3702Document35 pagesUnited States Court of Appeals For The Sixth Circuit: CASE NO. 22-3702Chris100% (1)

- Dvorak Opening BriefDocument45 pagesDvorak Opening Briefglimmertwins100% (2)

- Vasquez Response in Criminal TrialDocument10 pagesVasquez Response in Criminal TrialglimmertwinsNo ratings yet

- Transcript of Proceedings Day 1Document97 pagesTranscript of Proceedings Day 1glimmertwins100% (1)

- Plaintiffs' Response To Defendant's Objection To Magistrate Order "Deeming" Certain Facts Established and "Striking" Certain Affirmative DefensesDocument76 pagesPlaintiffs' Response To Defendant's Objection To Magistrate Order "Deeming" Certain Facts Established and "Striking" Certain Affirmative DefensesAnonymous XkawRUfNo ratings yet

- Brief in Opposition To Trademark Injunction RequestsDocument32 pagesBrief in Opposition To Trademark Injunction RequestsDaniel BallardNo ratings yet

- Syngenta Motion SummaryDocument43 pagesSyngenta Motion SummaryDaniel FisherNo ratings yet

- Response and Memorandum of LawDocument51 pagesResponse and Memorandum of LawForeclosure FraudNo ratings yet

- Arbitration Law and Practice in KenyaFrom EverandArbitration Law and Practice in KenyaRating: 2.5 out of 5 stars2.5/5 (4)

- From Conceptual To Executable BPMN Process ModelsDocument49 pagesFrom Conceptual To Executable BPMN Process ModelsAlbertiNo ratings yet

- Gene Pool v. Coastal Harvest - Brief ISO MTDDocument19 pagesGene Pool v. Coastal Harvest - Brief ISO MTDSarah BursteinNo ratings yet

- Dvorak Mar 23Document103 pagesDvorak Mar 23glimmertwins100% (1)

- 26 - Oppn Re PIDocument138 pages26 - Oppn Re PISarah BursteinNo ratings yet

- Chiquita Cross Motion To Disqualify Terry CollingsworthDocument16 pagesChiquita Cross Motion To Disqualify Terry CollingsworthPaulWolfNo ratings yet

- Tepper v. Temple-InlandDocument114 pagesTepper v. Temple-InlandDealBookNo ratings yet

- 67 - Petitioners' Opening Brief & Addendum PDFDocument184 pages67 - Petitioners' Opening Brief & Addendum PDFfreewildhorsesNo ratings yet

- CFTOD Motion To DismissDocument55 pagesCFTOD Motion To DismissChristie ZizoNo ratings yet

- DHS Memo Oct.Document32 pagesDHS Memo Oct.Law&CrimeNo ratings yet

- USA v. David Foley - Court of Appeals Docket 14-10055 Doc 22-1Document45 pagesUSA v. David Foley - Court of Appeals Docket 14-10055 Doc 22-1scion.scionNo ratings yet

- Golda Barton and Michael Cameron v. Officer Michael Farillas, Chief Mike Brown, and Salt Lake City CorporationDocument31 pagesGolda Barton and Michael Cameron v. Officer Michael Farillas, Chief Mike Brown, and Salt Lake City CorporationMacKenzie RyanNo ratings yet

- SAF Files For Summary Judgement in Challenge To N.Y. Gun BanDocument23 pagesSAF Files For Summary Judgement in Challenge To N.Y. Gun BanAmmoLand Shooting Sports NewsNo ratings yet

- Deutsche Bank V FDIC Chase JP Morgan WAMUDocument51 pagesDeutsche Bank V FDIC Chase JP Morgan WAMUdrattyNo ratings yet

- THOMAS MORE LAW CENTER, Et Al. V OBAMA, Et Al. - 12 - Defendants' Response - Gov - Uscourts.mied.247295.12.0Document46 pagesTHOMAS MORE LAW CENTER, Et Al. V OBAMA, Et Al. - 12 - Defendants' Response - Gov - Uscourts.mied.247295.12.0Jack RyanNo ratings yet

- VanDellen Motion For Judgment On The PleadingsDocument30 pagesVanDellen Motion For Judgment On The PleadingsMike Fant100% (1)

- Plaintiff Opposition To Application For TRODocument25 pagesPlaintiff Opposition To Application For TROCNET NewsNo ratings yet

- JPMorgan Vs MullaughDocument54 pagesJPMorgan Vs MullaughZerohedgeNo ratings yet

- Chiquita Motion For Summary Judgment On Negligence Per SeDocument25 pagesChiquita Motion For Summary Judgment On Negligence Per SePaulWolfNo ratings yet

- Brief in Support of Rambus Inc.'S Proposed Findings of Fact and Conclusions of LawDocument36 pagesBrief in Support of Rambus Inc.'S Proposed Findings of Fact and Conclusions of Lawsabatino123No ratings yet

- WALPIN V CNCS - 17 - Reply in Support of Motion To Dismiss Gov - Uscourts.dcd.137649.17.0Document30 pagesWALPIN V CNCS - 17 - Reply in Support of Motion To Dismiss Gov - Uscourts.dcd.137649.17.0Jack RyanNo ratings yet

- 2013-08 Alphayankee-Vowell 9cir FtcansweringbriefDocument65 pages2013-08 Alphayankee-Vowell 9cir FtcansweringbriefAntsatiana Mu RamarokotoNo ratings yet

- Plaintiff's Memorandum in Opposition To State of Hawaii's Motion For Summary Judgment, Bridge Aina Lea, LLC v. State Land Use Comm'n, No. 11-00414 SOM-BMK (D. Haw. Filed Jan. 19, 2016)Document47 pagesPlaintiff's Memorandum in Opposition To State of Hawaii's Motion For Summary Judgment, Bridge Aina Lea, LLC v. State Land Use Comm'n, No. 11-00414 SOM-BMK (D. Haw. Filed Jan. 19, 2016)RHTNo ratings yet

- Megaupload MTD MemoDocument39 pagesMegaupload MTD MemoEriq GardnerNo ratings yet

- Eric Inselberg Motion To RemandDocument20 pagesEric Inselberg Motion To RemandAnthony J. PerezNo ratings yet

- Greene V Paramount MSJDocument33 pagesGreene V Paramount MSJTHROnlineNo ratings yet

- Counsel For Lead Plaintiff Bradley Sostack: Plaintiff'S Opposition To Motion To Dismiss Consolidated ComplaintDocument34 pagesCounsel For Lead Plaintiff Bradley Sostack: Plaintiff'S Opposition To Motion To Dismiss Consolidated ComplaintForkLogNo ratings yet

- Attorneys For Petitioner State of WyomingDocument65 pagesAttorneys For Petitioner State of Wyomingnate_raymondNo ratings yet

- HBO Responce 11.5.19Document15 pagesHBO Responce 11.5.19Rasheed MNo ratings yet

- Local TV Advertising Antitrust Litigation Motion For Preliminary Approval of SettlementDocument37 pagesLocal TV Advertising Antitrust Litigation Motion For Preliminary Approval of SettlementTHROnlineNo ratings yet

- Dapper Labs' Motion To DismissDocument38 pagesDapper Labs' Motion To DismissDarius C. GambinoNo ratings yet

- 2010-04 Homeassureii 11cir FtcbriefDocument38 pages2010-04 Homeassureii 11cir FtcbriefAntsatiana Mu RamarokotoNo ratings yet

- Stormy Daniels v. Trump, Cohen Motion For ReconsiderationDocument25 pagesStormy Daniels v. Trump, Cohen Motion For Reconsiderationmary engNo ratings yet

- USA V Francis Raia, Et Al. Omnibus Motion Filed 2-19-2019Document36 pagesUSA V Francis Raia, Et Al. Omnibus Motion Filed 2-19-2019GrafixAvengerNo ratings yet

- 2021-07-07 32 Brief of Appellants (Updated)Document76 pages2021-07-07 32 Brief of Appellants (Updated)Live 5 NewsNo ratings yet

- In Re Nordstrom Petition Writ of MandamusDocument39 pagesIn Re Nordstrom Petition Writ of MandamusFindLawNo ratings yet

- NACDL Amicus Brief FlynnDocument25 pagesNACDL Amicus Brief FlynnDavid Oscar Markus100% (2)

- Hindes Jacobs Appeals Brief 17 3794 0016Document92 pagesHindes Jacobs Appeals Brief 17 3794 0016Schrodinger StateofwarNo ratings yet

- KMPG Memo On Motion For Summary JudgementDocument48 pagesKMPG Memo On Motion For Summary Judgementny1davidNo ratings yet

- Hannibal Reply BriefDocument75 pagesHannibal Reply BriefWhite-FangNo ratings yet

- Brief For Petitioner, Sheetz v. County of El Dorado, No. 22-1074 (U.S. Nov. 13, 2023)Document57 pagesBrief For Petitioner, Sheetz v. County of El Dorado, No. 22-1074 (U.S. Nov. 13, 2023)RHTNo ratings yet

- News Corp HackingDocument58 pagesNews Corp HackingApril PetersenNo ratings yet

- Doster 1 As Filed Appellee BriefDocument73 pagesDoster 1 As Filed Appellee BriefChrisNo ratings yet

- In The Supreme Court of The United States: O W C S C CDocument42 pagesIn The Supreme Court of The United States: O W C S C CBengt HörbergNo ratings yet

- JPMorgan Opposition To Motion To Disqualify WilmerHaleDocument24 pagesJPMorgan Opposition To Motion To Disqualify WilmerHaleChefs Best Statements - NewsNo ratings yet

- Postmortal succession on the example of Polish law in a comparative perspective: Between inheritance law and nonprobate transfersFrom EverandPostmortal succession on the example of Polish law in a comparative perspective: Between inheritance law and nonprobate transfersNo ratings yet

- Helen Bagley BriefDocument24 pagesHelen Bagley BriefglimmertwinsNo ratings yet

- Final Judgement Against MarcoDocument5 pagesFinal Judgement Against Marcoglimmertwins100% (1)

- SEC Glisson Case ExhibitsDocument94 pagesSEC Glisson Case ExhibitsglimmertwinsNo ratings yet

- Consent To Final JudgementDocument5 pagesConsent To Final Judgementglimmertwins100% (1)

- Marco Continuance MotionDocument18 pagesMarco Continuance MotionglimmertwinsNo ratings yet

- Post 2007Document11 pagesPost 2007glimmertwinsNo ratings yet

- Glissons Finding of FactDocument12 pagesGlissons Finding of FactglimmertwinsNo ratings yet

- Marco Judges OrderDocument2 pagesMarco Judges OrderglimmertwinsNo ratings yet

- Marco Mar 19 98-MainDocument69 pagesMarco Mar 19 98-Mainglimmertwins100% (1)

- SEC Findings of FactDocument37 pagesSEC Findings of FactglimmertwinsNo ratings yet

- Gewerter March 6Document8 pagesGewerter March 6glimmertwinsNo ratings yet

- Fryars Final ReportDocument11 pagesFryars Final ReportglimmertwinsNo ratings yet

- SEC On Bank RecordsDocument2 pagesSEC On Bank RecordsglimmertwinsNo ratings yet

- Bagley Dec 2011 Transport RoomDocument45 pagesBagley Dec 2011 Transport RoomglimmertwinsNo ratings yet

- Glisson Motion in LimineDocument5 pagesGlisson Motion in Limineglimmertwins100% (1)

- StayDocument12 pagesStayglimmertwinsNo ratings yet

- SEC Certain WitnessesDocument3 pagesSEC Certain WitnessesglimmertwinsNo ratings yet

- BifurcateDocument10 pagesBifurcateglimmertwinsNo ratings yet

- 76 MainDocument27 pages76 MainglimmertwinsNo ratings yet

- Gutierrez Response DiscoveryDocument4 pagesGutierrez Response DiscoveryglimmertwinsNo ratings yet

- SEC Motion in LimineDocument15 pagesSEC Motion in LimineglimmertwinsNo ratings yet

- 76 1Document3 pages76 1glimmertwins100% (1)

- Ubaf 1Document6 pagesUbaf 1ivecita27No ratings yet

- EY Global Fraud SurveyDocument28 pagesEY Global Fraud SurveyannnooonnyyyymmousssNo ratings yet

- What You Should Know About The Cap RateDocument4 pagesWhat You Should Know About The Cap RateJacob YangNo ratings yet

- Product, Branding, and Packaging ConceptsDocument30 pagesProduct, Branding, and Packaging ConceptsUjjwal BhattaNo ratings yet

- Completing The Audit: ©2006 Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/ElderDocument41 pagesCompleting The Audit: ©2006 Prentice Hall Business Publishing, Auditing 11/e, Arens/Beasley/ElderJohn BryanNo ratings yet

- QuizBee Final Questions PDFDocument111 pagesQuizBee Final Questions PDFJenny LariosaNo ratings yet

- 3 - Book of Prime EntryDocument69 pages3 - Book of Prime Entrynurzbiet8587No ratings yet

- Collaboration Business Plan TemplateDocument18 pagesCollaboration Business Plan TemplateThu A. PhamNo ratings yet

- Auditing and Investigation Acc 412Document7 pagesAuditing and Investigation Acc 412saidsulaiman2095No ratings yet

- Curriculum - Rice MillingDocument32 pagesCurriculum - Rice MillingRiya PanjwaniNo ratings yet

- PM 5-6Document7 pagesPM 5-6Nguyễn UyênNo ratings yet

- Alliecovello ResumeDocument2 pagesAlliecovello Resumeapi-310731929No ratings yet

- Economic Environment of Business Mini ProjectDocument19 pagesEconomic Environment of Business Mini Projectpankajkapse67% (3)

- Contract of Sale of GoodsDocument18 pagesContract of Sale of GoodsManoj KumarNo ratings yet

- Entry Strategies: Exporting Contractual Entry Modes Foreign Direct Investment (Document10 pagesEntry Strategies: Exporting Contractual Entry Modes Foreign Direct Investment (DianaProEraNo ratings yet

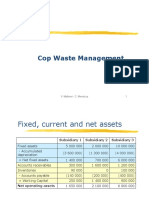

- Cop Waste Management SolutionDocument5 pagesCop Waste Management SolutionPaul GhanimehNo ratings yet

- Smart Notes On Contract DraftingDocument32 pagesSmart Notes On Contract DraftingGourav RathodNo ratings yet

- w27 UpdatesDocument9 pagesw27 UpdatesRafayNo ratings yet

- 5 House Property PDFDocument23 pages5 House Property PDFDamodar SejpalNo ratings yet

- ch1 12e TB Chapter1 12th Edition of Business Ethics Test BankDocument27 pagesch1 12e TB Chapter1 12th Edition of Business Ethics Test BankKhánh Linh LêNo ratings yet

- June 2015 QP - Paper 1 Edexcel Economics IGCSEDocument24 pagesJune 2015 QP - Paper 1 Edexcel Economics IGCSEShibraj DebNo ratings yet

- Outsourcing Security Case StudyDocument13 pagesOutsourcing Security Case StudyismakieNo ratings yet

- Chapter 4 - Part 1Document14 pagesChapter 4 - Part 1billtanNo ratings yet

- Service MarketingDocument21 pagesService MarketingKunwar AdityaNo ratings yet

- Rapport Annuel Awb - Vangl PDFDocument86 pagesRapport Annuel Awb - Vangl PDFcasaNo ratings yet

- Chapter 6 ReceivablesDocument8 pagesChapter 6 ReceivablesHaileluel WondimnehNo ratings yet

- Feature Article: Value Analysis/Value Engineering: The Forgotten Lean TechniqueDocument37 pagesFeature Article: Value Analysis/Value Engineering: The Forgotten Lean Techniquekish007rdNo ratings yet

- RFP Template Government ModelDocument19 pagesRFP Template Government ModellgdkulclsubucvhgdjNo ratings yet