You might also like

- A Remembrance of Tommy SwansonDocument157 pagesA Remembrance of Tommy SwansonBrian DugganNo ratings yet

- A Remembrance of Tommy SwansonDocument157 pagesA Remembrance of Tommy SwansonBrian DugganNo ratings yet

- Journalism 107 Fall 2013 SyllabusDocument6 pagesJournalism 107 Fall 2013 SyllabusBrian DugganNo ratings yet

- Washoe Cty Rep CNTRL ComDocument2 pagesWashoe Cty Rep CNTRL ComBrian DugganNo ratings yet

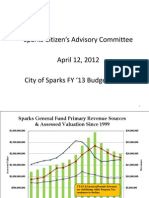

- Sparks Recommended FY13 BudgetDocument10 pagesSparks Recommended FY13 BudgetBrian DugganNo ratings yet

- 2012 05 31 Letter To O'MaraDocument2 pages2012 05 31 Letter To O'MaraBrian DugganNo ratings yet

- Petition For Declaratory ReliefDocument49 pagesPetition For Declaratory ReliefBrian DugganNo ratings yet

- The Art of The LeadDocument12 pagesThe Art of The LeadBrian DugganNo ratings yet

- Journalism 107 Syllabus Fall 2013Document6 pagesJournalism 107 Syllabus Fall 2013Brian DugganNo ratings yet

- SOS - WCRP Re Late Filed Report 5-25-12Document2 pagesSOS - WCRP Re Late Filed Report 5-25-12Brian DugganNo ratings yet

- Transitional Fire Department Proposal: Reno/TMFPD/SFPDDocument9 pagesTransitional Fire Department Proposal: Reno/TMFPD/SFPDBrian DugganNo ratings yet

- Attorney Letter On Behalf of Our Lady of The Snows SchoolDocument7 pagesAttorney Letter On Behalf of Our Lady of The Snows SchoolBrian DugganNo ratings yet

- First Nevada Report On STAR Bond District PreformanceDocument2 pagesFirst Nevada Report On STAR Bond District PreformanceBrian DugganNo ratings yet

- Legends DefaultDocument9 pagesLegends DefaultBrian DugganNo ratings yet

- Reno Police Department Cell PhoneDocument5 pagesReno Police Department Cell PhoneBrian DugganNo ratings yet

- Save Lander Street CoalitionDocument2 pagesSave Lander Street CoalitionBrian DugganNo ratings yet

- Reno Fireworks 1Document1 pageReno Fireworks 1Brian DugganNo ratings yet

- Wild Orchid Appeal - City Council 2012Document7 pagesWild Orchid Appeal - City Council 2012Brian DugganNo ratings yet

- Reno Fireworks 2Document1 pageReno Fireworks 2Brian DugganNo ratings yet

- J453 SyllabusDocument8 pagesJ453 SyllabusBrian DugganNo ratings yet

- J453 SyllabusDocument8 pagesJ453 SyllabusBrian DugganNo ratings yet

- J453 Sylb - 040311Document8 pagesJ453 Sylb - 040311Brian DugganNo ratings yet

- J453 SyllabusDocument8 pagesJ453 SyllabusBrian DugganNo ratings yet

- Journalists Without An Audience Are Just Diarists, Solitary Scribblers of Their Own Thoughts. - Ryan ThornburgDocument11 pagesJournalists Without An Audience Are Just Diarists, Solitary Scribblers of Their Own Thoughts. - Ryan ThornburgBrian DugganNo ratings yet

- J453 Lec01Document15 pagesJ453 Lec01Brian DugganNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5782)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (890)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (72)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Redington India A LTDDocument9 pagesRedington India A LTDNagarajan GNo ratings yet

- Macro EnvironmentDocument2 pagesMacro Environmentpoojasol100% (1)

- Macro Chapter 23Document7 pagesMacro Chapter 23farel a100% (1)

- PGPX Brochure 2019 - LiteDocument42 pagesPGPX Brochure 2019 - LitePiuNo ratings yet

- Instruction To Fill Form St3Document9 pagesInstruction To Fill Form St3Dhanush GokulNo ratings yet

- Top student scores OD strategiesDocument30 pagesTop student scores OD strategiesDeepak PhopaseNo ratings yet

- Fundamental Analysis EssentialsDocument41 pagesFundamental Analysis EssentialsRamana GNo ratings yet

- PDF Q1 Mod 2 Final EIM GRADE 9 10 EmA Final CheckedDocument19 pagesPDF Q1 Mod 2 Final EIM GRADE 9 10 EmA Final CheckedJOHN CARLO BAYBAYONNo ratings yet

- True/False: Chapter 13-Statement of Cash FlowsDocument10 pagesTrue/False: Chapter 13-Statement of Cash FlowsmilahrztaNo ratings yet

- Public Administration Planning ReportDocument35 pagesPublic Administration Planning ReportPrankur Sharma100% (1)

- A Project Report On FDI and Its Impact in IndiaDocument65 pagesA Project Report On FDI and Its Impact in IndiaNikhil Ranjan85% (102)

- Global Trade - Major ChallengesDocument4 pagesGlobal Trade - Major ChallengesrameshNo ratings yet

- Methods of CostingDocument21 pagesMethods of CostingsweetashusNo ratings yet

- POST TEST CHAPTER 1-3 - Enrichment Exercie For KB ManajemenDocument6 pagesPOST TEST CHAPTER 1-3 - Enrichment Exercie For KB ManajemenKiras SetyaNo ratings yet

- Globalisation is dead and we need to invent a new world orderDocument12 pagesGlobalisation is dead and we need to invent a new world orderJESSEAL SANTIAGONo ratings yet

- The New South Wales Energy Savings SchemeDocument12 pagesThe New South Wales Energy Savings SchemeAsia Clean Energy ForumNo ratings yet

- A Case Study On Starbucks - PpsDocument78 pagesA Case Study On Starbucks - PpsNiravNo ratings yet

- Compass Case Study SolutionDocument5 pagesCompass Case Study Solutionscheffls50% (4)

- Financial Accounting 4th Edition Spiceland Solutions Manual DownloadDocument45 pagesFinancial Accounting 4th Edition Spiceland Solutions Manual DownloadMark Arteaga100% (21)

- Pricing Strat LGDocument3 pagesPricing Strat LGVishnu v nathNo ratings yet

- China Strategy 2011Document178 pagesChina Strategy 2011Anees AisyahNo ratings yet

- Kebs 102Document31 pagesKebs 102snsmiddleschool2020No ratings yet

- Guna Fibres Case Study: Financial Forecasting and Debt ManagementDocument2 pagesGuna Fibres Case Study: Financial Forecasting and Debt ManagementvinitaNo ratings yet

- Soundscape. Silence, Noise and The Public DomainDocument40 pagesSoundscape. Silence, Noise and The Public DomainverasazeNo ratings yet

- Choosing The Right ESOP PlanDocument10 pagesChoosing The Right ESOP PlanSriram VeeramaniNo ratings yet

- Salary Account Opening FormDocument12 pagesSalary Account Opening FormVijay DhanarajNo ratings yet

- Agricultural Cooperatives History Theory ProblemsDocument30 pagesAgricultural Cooperatives History Theory ProblemsSamoon Khan AhmadzaiNo ratings yet

- Industrial Market SegmentationDocument23 pagesIndustrial Market SegmentationsuzandsilvaNo ratings yet

- Bangladesh Bank Report (Final)Document14 pagesBangladesh Bank Report (Final)chatterjee1987100% (4)

- Total Reward ManagementDocument50 pagesTotal Reward ManagementSeta A Wicaksana100% (1)