You might also like

- Micro Finance - Keys & Challenges:-A Review Mohit RewariDocument13 pagesMicro Finance - Keys & Challenges:-A Review Mohit Rewarisonia khuranaNo ratings yet

- The Role of Micro Finance in SHGDocument12 pagesThe Role of Micro Finance in SHGijgarph100% (1)

- Amity UniversityDocument7 pagesAmity Universityrsrpk27No ratings yet

- Microfinance in India Scopes and LimitationsDocument41 pagesMicrofinance in India Scopes and Limitationsspy67% (3)

- Topic of The Week For Discussion: 12 To 18 March: Topic: Microfinance Sector in IndiaDocument2 pagesTopic of The Week For Discussion: 12 To 18 March: Topic: Microfinance Sector in Indiarockstar104No ratings yet

- Status of Microfinance and Its Delivery Models in IndiaDocument13 pagesStatus of Microfinance and Its Delivery Models in IndiaSiva Sankari100% (1)

- Micro Finance: Emerging Challenges and Opening Vistas: Dr. Anupama Sharma, Ms. Sumita Kukreja, DR - Anjana SharmaDocument9 pagesMicro Finance: Emerging Challenges and Opening Vistas: Dr. Anupama Sharma, Ms. Sumita Kukreja, DR - Anjana SharmaInternational Organization of Scientific Research (IOSR)No ratings yet

- Micro-Finance in The India: The Changing Face of Micro-Credit SchemesDocument11 pagesMicro-Finance in The India: The Changing Face of Micro-Credit SchemesMahesh ChavanNo ratings yet

- Picturing Micro Finance: S. Arun Kumar Dhanamjaya Bhupathi E.Mohanraj - PresentDocument23 pagesPicturing Micro Finance: S. Arun Kumar Dhanamjaya Bhupathi E.Mohanraj - PresentjeyaselwynNo ratings yet

- Banking India: Accepting Deposits for the Purpose of LendingFrom EverandBanking India: Accepting Deposits for the Purpose of LendingNo ratings yet

- Journal - Nikita 2jul14mrrDocument7 pagesJournal - Nikita 2jul14mrrRohit KumarNo ratings yet

- Customer Satisfaction and Microfinance in UnaccoDocument21 pagesCustomer Satisfaction and Microfinance in UnaccoOmita ChanuNo ratings yet

- Microfinance in India and Porters Five Forces AnalysisDocument19 pagesMicrofinance in India and Porters Five Forces AnalysisCharismagicNo ratings yet

- Current Market Size of Rs27 BillionDocument5 pagesCurrent Market Size of Rs27 BillionSiddhartha BothraNo ratings yet

- Microfinance and NgosDocument8 pagesMicrofinance and NgosFarhana MishuNo ratings yet

- IciciDocument3 pagesIciciOm PrakashNo ratings yet

- MFS PPT FinalDocument18 pagesMFS PPT FinalvijaybharvadNo ratings yet

- Outreach of Microfinance Services in India: By: Rajni KumariDocument5 pagesOutreach of Microfinance Services in India: By: Rajni Kumarihoney802301No ratings yet

- Rural Banking and Micro Finance: Unit: IVDocument17 pagesRural Banking and Micro Finance: Unit: IVkimberly0jonesNo ratings yet

- Inroduction: Microfinance Is A Category of Financial ServicesDocument23 pagesInroduction: Microfinance Is A Category of Financial ServicesNikilNo ratings yet

- Chapter 4 Rural Banking and Micro Financing 1Document16 pagesChapter 4 Rural Banking and Micro Financing 1saloniNo ratings yet

- Building Sustainable Microfinance Institutions in IndiaDocument18 pagesBuilding Sustainable Microfinance Institutions in IndiaAlok BhandariNo ratings yet

- Swot Analysis of Mfs HG Sin IndiaDocument13 pagesSwot Analysis of Mfs HG Sin IndiaHarsh KumarNo ratings yet

- Session 1 - Grameen BankDocument5 pagesSession 1 - Grameen BankagyeyaNo ratings yet

- Microfinance in India - Growth and Present StatusDocument16 pagesMicrofinance in India - Growth and Present StatusIJOPAAR JOURNALNo ratings yet

- Micro Finance Sector in India ModelDocument9 pagesMicro Finance Sector in India Modelswati singhNo ratings yet

- Term Paper of Banking & Insurance: Topic: Micro Finance Development Overview and ChallengesDocument18 pagesTerm Paper of Banking & Insurance: Topic: Micro Finance Development Overview and ChallengesSumit SinghNo ratings yet

- Microfinance in India - A Tool For Poverty ReductionDocument20 pagesMicrofinance in India - A Tool For Poverty ReductionVijay KumarNo ratings yet

- AMFPL Credit Appraisal PolicyDocument16 pagesAMFPL Credit Appraisal PolicyPranav GuptaNo ratings yet

- Sustainability of MFI's in India After Y.H.Malegam CommitteeDocument18 pagesSustainability of MFI's in India After Y.H.Malegam CommitteeAnup BmNo ratings yet

- Micro Finance in IndiaDocument59 pagesMicro Finance in IndiaApurva Bangera100% (1)

- Social Banking Under NationalisationDocument8 pagesSocial Banking Under NationalisationLiya ShajanNo ratings yet

- Rajni Sinha PDFDocument23 pagesRajni Sinha PDFshivani mishraNo ratings yet

- 7.P Syamala DeviDocument4 pages7.P Syamala DeviSachin SahooNo ratings yet

- Pillars of Financial Inclusion Remittances - Micro Insurance and Micro SavingsDocument27 pagesPillars of Financial Inclusion Remittances - Micro Insurance and Micro SavingsDhara PatelNo ratings yet

- Role of Microfinance in Women EmpowermentDocument25 pagesRole of Microfinance in Women EmpowermentDevansh MoyalNo ratings yet

- Banking and Microfinance - IIDocument24 pagesBanking and Microfinance - IIKoyelNo ratings yet

- Project On Rural Banking in India 15-01-2023Document74 pagesProject On Rural Banking in India 15-01-2023Praveen ChaudharyNo ratings yet

- 2014-VII-1&2 NilimaDocument13 pages2014-VII-1&2 NilimaAPOORVA GUPTANo ratings yet

- Micro Finance The Paradigm ShiftDocument24 pagesMicro Finance The Paradigm ShiftPrateek Goel100% (1)

- Mfi Obj.1Document13 pagesMfi Obj.1Anjum MehtabNo ratings yet

- Micro Finance (BankingDocument35 pagesMicro Finance (BankingAsim Waghu100% (1)

- Micro Finance Need of The HourDocument11 pagesMicro Finance Need of The HouramarsxcranNo ratings yet

- Microfinance 140113043356 Phpapp01Document40 pagesMicrofinance 140113043356 Phpapp01karanjangid17No ratings yet

- MICRPFINANCE IN INDIA WordDocument14 pagesMICRPFINANCE IN INDIA WordA08 Ratika KambleNo ratings yet

- A Critical Analysis of Micro Finance in IndiaDocument54 pagesA Critical Analysis of Micro Finance in IndiaArchana MehraNo ratings yet

- Micro FinanceDocument5 pagesMicro FinancePayal SharmaNo ratings yet

- Awareness of MicrofinanceDocument34 pagesAwareness of MicrofinanceDisha Tiwari100% (1)

- Micro FinanceDocument17 pagesMicro FinanceAbhineet DhaliwalNo ratings yet

- Notes Micro FinanceDocument9 pagesNotes Micro Financesofty1980No ratings yet

- Microfinance 140113043356 Phpapp01Document40 pagesMicrofinance 140113043356 Phpapp01Manjula guptaNo ratings yet

- Micro Finance in IndiaDocument1 pageMicro Finance in IndiapethalammuNo ratings yet

- Micro CreditDocument9 pagesMicro Creditpalash dashNo ratings yet

- Growth of Micro Finance in India A Descriptive StudyDocument12 pagesGrowth of Micro Finance in India A Descriptive StudyBobby ShrivastavaNo ratings yet

- Growth of Micro Finance in India: A Descriptive StudyDocument12 pagesGrowth of Micro Finance in India: A Descriptive StudyAkhil Naik BanothNo ratings yet

- Project On Micro FinanceDocument68 pagesProject On Micro FinanceKapil RaoNo ratings yet

- A Study of The Performance of Microfinance Institutions in India in Present Era - A Tool For Poverty AlleviationDocument10 pagesA Study of The Performance of Microfinance Institutions in India in Present Era - A Tool For Poverty AlleviationjyotivermaNo ratings yet

- Microfinace Reading PDFDocument9 pagesMicrofinace Reading PDFCharles GarrettNo ratings yet

- Microfinance in India: A Critique by Rajarshi GhoshDocument9 pagesMicrofinance in India: A Critique by Rajarshi Ghoshpraveen_jha_9No ratings yet

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)From EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)No ratings yet

- CMAT Application FormDocument2 pagesCMAT Application FormPrashant Upashi SonuNo ratings yet

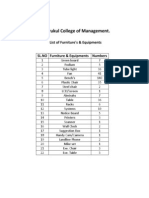

- Gurukul College of Management.: List of Furniture's & EquipmentsDocument1 pageGurukul College of Management.: List of Furniture's & EquipmentsPrashant Upashi SonuNo ratings yet

- AL Shjaray School (1) GJGJHDocument3 pagesAL Shjaray School (1) GJGJHPrashant Upashi SonuNo ratings yet

- Characterstics of Good Programming: Requires Less Space: The Program Must Consume Less Space in The MemoryDocument7 pagesCharacterstics of Good Programming: Requires Less Space: The Program Must Consume Less Space in The MemoryPrashant Upashi SonuNo ratings yet

- Grammar Through Tips (MBA) A4 (Booklet) 2011-12Document50 pagesGrammar Through Tips (MBA) A4 (Booklet) 2011-12Prashant Upashi SonuNo ratings yet

- Bus PassDocument1 pageBus PassPrashant Upashi SonuNo ratings yet

- Aryabhatta TutorialsDocument3 pagesAryabhatta TutorialsPrashant Upashi SonuNo ratings yet

- Product and Product MixDocument28 pagesProduct and Product MixPrashant Upashi SonuNo ratings yet

- Weekend Time Table For 1apr-2012Document2 pagesWeekend Time Table For 1apr-2012Prashant Upashi SonuNo ratings yet

- Addmen Campus AutomationDocument3 pagesAddmen Campus AutomationPrashant Upashi SonuNo ratings yet

- UiicDocument7 pagesUiicPrashant Upashi SonuNo ratings yet

- Advt PHD 201415Document4 pagesAdvt PHD 201415sashankchappidigmailNo ratings yet

- Bank Loan NewDocument1 pageBank Loan NewPrashant Upashi SonuNo ratings yet

- 5darDocument2 pages5darPrashant Upashi SonuNo ratings yet

- AcknowledgementDocument3 pagesAcknowledgementPrashant Upashi SonuNo ratings yet

- Sensation of Wizardly DreamDocument3 pagesSensation of Wizardly DreamPrashant Upashi SonuNo ratings yet

- Latihan Soal Bab 9 - Kelompok 2Document17 pagesLatihan Soal Bab 9 - Kelompok 2Penduduk MarsNo ratings yet

- 1569974603267g4SdkiBXnw22cLKZ PDFDocument4 pages1569974603267g4SdkiBXnw22cLKZ PDFSelvarathnam MuniratnamNo ratings yet

- C CCCCCCC CCCCC CC CCC CCCCCC C CC CC!"C CCCCCC C# C CCCC$!C CCCC%C C& C CC!C C' (CC$CC C) C C+ (CCC!Document6 pagesC CCCCCCC CCCCC CC CCC CCCCCC C CC CC!"C CCCCCC C# C CCCC$!C CCCC%C C& C CC!C C' (CC$CC C) C C+ (CCC!Jitesh TolaniNo ratings yet

- 23Document2 pages23Heaven HeartNo ratings yet

- Investing Tips: Lesson 18: Student Activity Sheet 1Document3 pagesInvesting Tips: Lesson 18: Student Activity Sheet 1GONZALO JIMENEZ MORALESNo ratings yet

- CH 03Document60 pagesCH 03Hiền AnhNo ratings yet

- 2.maks Energy Solutions - GIDDocument40 pages2.maks Energy Solutions - GIDLaxmikant RathiNo ratings yet

- Capital and Revenue Income and ExpenditureDocument31 pagesCapital and Revenue Income and ExpenditureMahesh Chandra Sharma100% (2)

- Creative Accounting, Ethics and Professional DevelomentDocument21 pagesCreative Accounting, Ethics and Professional DevelomentFaiz FaisalNo ratings yet

- Institutions and Corporate Capital Structure in The MENA RegionDocument32 pagesInstitutions and Corporate Capital Structure in The MENA RegionMissaoui IbtissemNo ratings yet

- Group-Assignment ACC101Document5 pagesGroup-Assignment ACC101Nguyen Duc Minh K17 HLNo ratings yet

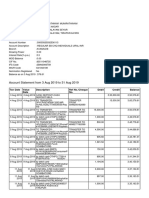

- Account Statement PDFDocument12 pagesAccount Statement PDFSudip MukherjeeNo ratings yet

- FM TestDocument5 pagesFM TestSamir JainNo ratings yet

- Ncert Solution Class 11 Accountancy Chapter 10Document68 pagesNcert Solution Class 11 Accountancy Chapter 10Prakal 444No ratings yet

- MIBE - Transcript - Credits by Area 2Document6 pagesMIBE - Transcript - Credits by Area 2Sohad ElnagarNo ratings yet

- Medida vs. CADocument1 pageMedida vs. CANiñoMaurinNo ratings yet

- Consolidated Statement: DepositsDocument6 pagesConsolidated Statement: DepositsVivekNo ratings yet

- Credit ActivityDocument2 pagesCredit Activityamo53No ratings yet

- Study Questions 12 Risk and Return SolutionsDocument4 pagesStudy Questions 12 Risk and Return SolutionsAlif SultanliNo ratings yet

- Paymore Products Places Orders For Goods Equal To 75 ofDocument1 pagePaymore Products Places Orders For Goods Equal To 75 ofAmit PandeyNo ratings yet

- T-Bills: Abhishek Sinha (CSM 1001) Anand Sachdeva (CSM 1002) Pramod Singh (CSM 1013) Saurabh Shukla (CSM 1019)Document14 pagesT-Bills: Abhishek Sinha (CSM 1001) Anand Sachdeva (CSM 1002) Pramod Singh (CSM 1013) Saurabh Shukla (CSM 1019)anandsachsNo ratings yet

- MODULE 7 BudgetingDocument6 pagesMODULE 7 BudgetingKatrina Peralta FabianNo ratings yet

- Horizontal & Vertical AnalysisDocument7 pagesHorizontal & Vertical AnalysisMisha SaeedNo ratings yet

- Account Statement For The Period01/05/2022to07/07/2022: Account Number Branch AddressDocument12 pagesAccount Statement For The Period01/05/2022to07/07/2022: Account Number Branch AddressMantuNo ratings yet

- Finance Module 1 Definition of Finance and Identifying The Roles in A Corporate OrganizationDocument31 pagesFinance Module 1 Definition of Finance and Identifying The Roles in A Corporate OrganizationCjNo ratings yet

- Foreign Currency HedgingDocument4 pagesForeign Currency HedgingBianca Iyiyi100% (4)

- Mers RulesDocument43 pagesMers RulessnrdadNo ratings yet

- IO Reading ListDocument3 pagesIO Reading ListDat NguyenNo ratings yet

- 1st Activity in ACCA104Document11 pages1st Activity in ACCA104John Rey BonitNo ratings yet

- SolutionsDocument5 pagesSolutionsSahil NandaNo ratings yet