You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Types of FinancingDocument17 pagesTypes of FinancingHimadhar SaduNo ratings yet

- NCFM BeginnersDocument12 pagesNCFM BeginnersTrupti Mane100% (1)

- Implication of The Competition Act, 2002 On Cross Border Merger: An Indian PerspectiveDocument50 pagesImplication of The Competition Act, 2002 On Cross Border Merger: An Indian Perspectiveparul meenaNo ratings yet

- Depository Receipts in India: With A Special Reference To Indian Depository ReceiptsDocument18 pagesDepository Receipts in India: With A Special Reference To Indian Depository Receiptsnikhil rajpurohitNo ratings yet

- L5 Financial PlansDocument55 pagesL5 Financial Plansfairylucas708No ratings yet

- Report Petro ItauDocument11 pagesReport Petro ItauQuatroANo ratings yet

- AKTU Financial Market and Commercial Banking Unit IV NotesDocument50 pagesAKTU Financial Market and Commercial Banking Unit IV NotesGaurav SonkarNo ratings yet

- Santhosh CVDocument6 pagesSanthosh CVSanthosh ANo ratings yet

- Options Glossary 1Document171 pagesOptions Glossary 1Tomo KostajnsekNo ratings yet

- GDR & ADRsDocument4 pagesGDR & ADRsShub SidhuNo ratings yet

- The Multinational Finance FunctionDocument24 pagesThe Multinational Finance FunctionNishant100% (1)

- Astitva International Journal of Commerce Management and Social Sciences - April 2013Document91 pagesAstitva International Journal of Commerce Management and Social Sciences - April 2013astitvaconsultancyNo ratings yet

- Intro To Equities Hand OutDocument29 pagesIntro To Equities Hand OutHernandez Tejada AlexNo ratings yet

- FINA3020 Assignment3Document5 pagesFINA3020 Assignment3younes.louafiiizNo ratings yet

- 25 50 Full Board Meeting 20230227Document11 pages25 50 Full Board Meeting 20230227Contra Value BetsNo ratings yet

- DTCC SMART Search Report Listing ExternalDocument15 pagesDTCC SMART Search Report Listing ExternalIzraul HidashiNo ratings yet

- User Manual For Single Master Form-FirmsDocument103 pagesUser Manual For Single Master Form-FirmsUmaMaheshwariMohanNo ratings yet

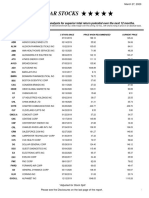

- Five Star StocksDocument5 pagesFive Star StocksJeff SturgeonNo ratings yet

- HTML Conversion Bug TextDocument136 pagesHTML Conversion Bug Textnew_guy_1997No ratings yet

- Hall of Shame - The Timothy PlanDocument2 pagesHall of Shame - The Timothy PlanJulieRoys50% (2)

- ADR and GDRDocument21 pagesADR and GDRAbhijeet BendkhaleNo ratings yet

- Introduction To HEINEKEN PDFDocument20 pagesIntroduction To HEINEKEN PDFEmilian IonutNo ratings yet

- Introduction To HEINEKENDocument20 pagesIntroduction To HEINEKENTuwshoo GanbatNo ratings yet

- Private Equity and Debt in Real EstateDocument86 pagesPrivate Equity and Debt in Real EstateashokmoryaNo ratings yet

- FED Master Direction No.15-2015-16Document41 pagesFED Master Direction No.15-2015-16sudhir.kochhar3530No ratings yet

- AGENDA: International Finance Instruments, Case Study - Infosys ADRDocument71 pagesAGENDA: International Finance Instruments, Case Study - Infosys ADR24_anuNo ratings yet

- WNSHoldings May2013 Form 20 FDocument446 pagesWNSHoldings May2013 Form 20 FsusegaadNo ratings yet

- American Depository ReceiptDocument2 pagesAmerican Depository ReceiptKrishna Prasad GaddeNo ratings yet

- HWCH 10Document2 pagesHWCH 10Hamis Rabiam MagundaNo ratings yet

- International Finance - Short Notes (Theory)Document20 pagesInternational Finance - Short Notes (Theory)Amit SinghNo ratings yet