You might also like

- Elements of A Sound Industrial RelationsDocument43 pagesElements of A Sound Industrial RelationsAjith Venugopal100% (1)

- 4.1 Wages, Types & TheoriesDocument3 pages4.1 Wages, Types & TheoriesM. DuttaNo ratings yet

- Trends Within Od and Their Impact On Od'S Future Traditional:-The First Trend Has To Do With Increasing Calls For ADocument5 pagesTrends Within Od and Their Impact On Od'S Future Traditional:-The First Trend Has To Do With Increasing Calls For ABijay PoudelNo ratings yet

- Industrial Relations - Definitions and Main Aspects Pri Sem IIDocument16 pagesIndustrial Relations - Definitions and Main Aspects Pri Sem IIyadav poonamNo ratings yet

- Industrial Relations-Defination and Main AspectsDocument18 pagesIndustrial Relations-Defination and Main AspectsShivani Nileshbhai PatelNo ratings yet

- Meaning and Definition of Industrial RelationDocument10 pagesMeaning and Definition of Industrial RelationSuhas SalianNo ratings yet

- MBA08166 CCTMWordDocumentDocument3 pagesMBA08166 CCTMWordDocumentSaksham AnandNo ratings yet

- WAGESDocument9 pagesWAGESBrajesh SwainNo ratings yet

- HR-02 (Employee Relations & Labour Law)Document69 pagesHR-02 (Employee Relations & Labour Law)Vishal RanjanNo ratings yet

- Wage Policy in IndiaDocument10 pagesWage Policy in IndiaDouble A CreationNo ratings yet

- Coaching & Mentoring - IGNOU MaterialDocument17 pagesCoaching & Mentoring - IGNOU MaterialsapnanibNo ratings yet

- Importance of Industrial RelationsDocument2 pagesImportance of Industrial RelationsshashimvijayNo ratings yet

- WAGESDocument59 pagesWAGESUdai DhivyaNo ratings yet

- The Labour Market Demand and SupplyDocument29 pagesThe Labour Market Demand and SupplyNafis SiddiquiNo ratings yet

- Collective Bargaining - Doc G2Document2 pagesCollective Bargaining - Doc G2Ankit Sinai TalaulikarNo ratings yet

- Industrial Relations in Mba HRDocument9 pagesIndustrial Relations in Mba HRNitinNo ratings yet

- Industrial Relations - Unit - 1Document7 pagesIndustrial Relations - Unit - 1ravideva84No ratings yet

- Industrial RelationDocument44 pagesIndustrial RelationDr. Khem ChandNo ratings yet

- Unit 1 Introduction Concept: Industrial RelationsDocument60 pagesUnit 1 Introduction Concept: Industrial RelationsShaila AkterNo ratings yet

- Government in A Market EconomyDocument4 pagesGovernment in A Market EconomymrzeettsNo ratings yet

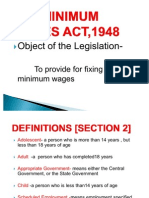

- Minimum Wages Act, 1948Document20 pagesMinimum Wages Act, 1948Manish KumarNo ratings yet

- Employee - Employer Relationship Agro Bio TechDocument114 pagesEmployee - Employer Relationship Agro Bio TechSathish SsathishNo ratings yet

- An Introduction To Labour Relations November 2020Document64 pagesAn Introduction To Labour Relations November 2020Shante MorganNo ratings yet

- Human Resource PlanningDocument5 pagesHuman Resource Planningtariq usmanNo ratings yet

- 4.5 Wage Determination Under Collective BargainingDocument4 pages4.5 Wage Determination Under Collective BargainingFoisal Mahmud Rownak100% (1)

- Industrial DisputesDocument8 pagesIndustrial DisputesSadhvi ThakurNo ratings yet

- NFM7e IM Part1Document117 pagesNFM7e IM Part1Angela Uytengsu0% (1)

- Trade UnionDocument19 pagesTrade UnionAmit MittalNo ratings yet

- 10 Stakeholder Theory 1 PDFDocument39 pages10 Stakeholder Theory 1 PDFzikrullahNo ratings yet

- Theories and Concepts Used To Analyse Industrial RelationsDocument13 pagesTheories and Concepts Used To Analyse Industrial RelationsAnup KumarNo ratings yet

- Industrial RelationDocument18 pagesIndustrial RelationRojalin NayakNo ratings yet

- Wage Board Structure Scope FunctionDocument22 pagesWage Board Structure Scope Functionsplit5244100% (2)

- Approaches To Industrial RelationsDocument39 pagesApproaches To Industrial Relationslovebassi86% (14)

- Typical Problems in Business EthicsDocument43 pagesTypical Problems in Business Ethicsrak_sai1591% (11)

- Human Resource Development and The Future Challenges PDFDocument11 pagesHuman Resource Development and The Future Challenges PDFrahulravi4uNo ratings yet

- Development of A Multinational Personnel Selection System Case AnalysisDocument6 pagesDevelopment of A Multinational Personnel Selection System Case AnalysisAngelina F. NipalesNo ratings yet

- PMS Assignment PDFDocument12 pagesPMS Assignment PDFNeel PrasantNo ratings yet

- Chapter 2serdtfyguhipDocument30 pagesChapter 2serdtfyguhipMuchtar ZarkasyiNo ratings yet

- Contemporary Issues in HRM - FinalDocument23 pagesContemporary Issues in HRM - FinalbshubhodeepNo ratings yet

- Establishing Strategic Pay Plan Ppt11Document34 pagesEstablishing Strategic Pay Plan Ppt11Ahmed YousufzaiNo ratings yet

- Components of CompensationDocument6 pagesComponents of Compensationsimply_cooolNo ratings yet

- Concept of Industrial RelationsDocument17 pagesConcept of Industrial Relationsyogendra ojhaNo ratings yet

- Chapter 1: Introduction: 1.1 Statement of The Research ProblemDocument22 pagesChapter 1: Introduction: 1.1 Statement of The Research Problembbakum100% (1)

- Contract Labour Regulation and Abolition Act 1970Document14 pagesContract Labour Regulation and Abolition Act 1970Anmol JainNo ratings yet

- Case StudyDocument3 pagesCase Studyruchita1989No ratings yet

- Management of Industrial RelationsDocument29 pagesManagement of Industrial RelationsDeshidi Manasa ReddyNo ratings yet

- MBA NotesDocument13 pagesMBA NotesRanjeet Verma LucknowNo ratings yet

- GRIEVANCE PROCEDURE and Collective BargainingDocument18 pagesGRIEVANCE PROCEDURE and Collective BargainingShalu PalNo ratings yet

- Lecture # 18-19 Handbook Working Condition and Employee RightsDocument6 pagesLecture # 18-19 Handbook Working Condition and Employee Rightskuashask2No ratings yet

- Attrition ManagementDocument31 pagesAttrition ManagementkirandcacNo ratings yet

- Internal and External Factors Affects HR, Job Desription ND SpecializationDocument28 pagesInternal and External Factors Affects HR, Job Desription ND SpecializationSaad ImranNo ratings yet

- Different Approaches To Industrial RelationsDocument8 pagesDifferent Approaches To Industrial RelationsAnkit Vira100% (1)

- A Brief Check List of Labour Laws: Composed by P.B.S. KumarDocument17 pagesA Brief Check List of Labour Laws: Composed by P.B.S. KumarJananee RajagopalanNo ratings yet

- Future of Organization Development (OD)Document14 pagesFuture of Organization Development (OD)DkdarpreetNo ratings yet

- Karl MarxDocument3 pagesKarl MarxHiezll Wynn R. RiveraNo ratings yet

- Classical Theories of WagesDocument2 pagesClassical Theories of WagesRoselle San BuenaventuraNo ratings yet

- Karl Marx's Wage Labor and Capital' - by The Dangerous Maybe - MediumDocument10 pagesKarl Marx's Wage Labor and Capital' - by The Dangerous Maybe - MediumGabriel DavidsonNo ratings yet

- G12-ABM 2 Supply and DemandDocument15 pagesG12-ABM 2 Supply and Demandkenneth coronelNo ratings yet

- Ta35 Ta40 Operations SafetyDocument150 pagesTa35 Ta40 Operations Safetyjuan100% (2)

- SOAL UTS Poetry Genap 2020Document5 pagesSOAL UTS Poetry Genap 2020Zara AzkiyahNo ratings yet

- Valuation of SharesDocument10 pagesValuation of SharesAmira JNo ratings yet

- Jollibee Foods Corporation Timeline CaDocument10 pagesJollibee Foods Corporation Timeline CaBaylon RachelNo ratings yet

- Second Division G.R. No. 212860, March 14, 2018 Republic of The Philippines, Petitioner, V. Florie Grace M. Cote, Respondent. Decision REYES, JR., J.Document6 pagesSecond Division G.R. No. 212860, March 14, 2018 Republic of The Philippines, Petitioner, V. Florie Grace M. Cote, Respondent. Decision REYES, JR., J.cnfhdxNo ratings yet

- Fight The Bad Feeling (Boys Over Flowers) Lyrics - T-MaxDocument7 pagesFight The Bad Feeling (Boys Over Flowers) Lyrics - T-MaxOwenNo ratings yet

- How To Use The Fishbone Tool For Root Cause AnalysisDocument3 pagesHow To Use The Fishbone Tool For Root Cause AnalysisMuhammad Tahir NawazNo ratings yet

- Generacion de Modelos de NegocioDocument285 pagesGeneracion de Modelos de NegocioMilca Aguirre100% (2)

- Mohave PlacersDocument8 pagesMohave PlacersChris GravesNo ratings yet

- Six Steps of Accounting Transaction AnalysisDocument2 pagesSix Steps of Accounting Transaction AnalysisJane ConstantinoNo ratings yet

- Business-Plan 9213535 PowerpointDocument22 pagesBusiness-Plan 9213535 PowerpointSadi AminNo ratings yet

- Emñìr (Ûvr'Df© - 2018: A (ZDM'© (DF'MDocument54 pagesEmñìr (Ûvr'Df© - 2018: A (ZDM'© (DF'MKarmicSmokeNo ratings yet

- Kasra Azar TP2 Lesson PlanDocument6 pagesKasra Azar TP2 Lesson Planکسری آذرNo ratings yet

- Inesco Amc 2106735164Document3 pagesInesco Amc 2106735164spahujNo ratings yet

- Development of External Combustion Engine: August 2013Document6 pagesDevelopment of External Combustion Engine: August 2013Alexsander JacobNo ratings yet

- Sea Doo MY21 Spec Sheet DPS GTX Limited EN NADocument1 pageSea Doo MY21 Spec Sheet DPS GTX Limited EN NADragan StanojevicNo ratings yet

- Mid-Term Test Part 1: Listening: Time Allowance: 90 MinsDocument4 pagesMid-Term Test Part 1: Listening: Time Allowance: 90 MinsThu Lan HàNo ratings yet

- Vice President Human Resources in Louisville KY Resume Christopher LitrasDocument3 pagesVice President Human Resources in Louisville KY Resume Christopher LitrasChristopher LitrasNo ratings yet

- Gremlins 3Document12 pagesGremlins 3Kenny TadrzynskiNo ratings yet

- Full Download Financial Accounting 17th Edition Williams Test BankDocument35 pagesFull Download Financial Accounting 17th Edition Williams Test Bankmcalljenaevippro100% (43)

- Press 150149661Document704 pagesPress 150149661Saurabh SumanNo ratings yet

- Als Assessment Form 1 Individual Learning Agreement: Department of EducationDocument9 pagesAls Assessment Form 1 Individual Learning Agreement: Department of EducationRitchie ModestoNo ratings yet

- ZONE A - Walled City ReportDocument49 pagesZONE A - Walled City ReportAr Vishnu Prakash0% (1)

- Young and BeautifulDocument8 pagesYoung and BeautifulDiana AdrianaNo ratings yet

- The Syn Alia Series On Animal TrainingDocument101 pagesThe Syn Alia Series On Animal Trainingben100% (1)

- International Shoe Size ChartDocument2 pagesInternational Shoe Size Chartlivelife01100% (1)

- Green Technology & Green BondDocument12 pagesGreen Technology & Green BondSIDDHARTH DASHNo ratings yet

- Coconut IndustryDocument2 pagesCoconut Industryka bayani100% (1)

- LEGAL AND JUDICIAL ETHICS - Final Report On The Financial Audit in The MCTC - AdoraDocument6 pagesLEGAL AND JUDICIAL ETHICS - Final Report On The Financial Audit in The MCTC - AdoraGabriel AdoraNo ratings yet

- ConsolationDocument2 pagesConsolationRavi S. VaidyanathanNo ratings yet

- Slow Burn: The Hidden Costs of a Warming WorldFrom EverandSlow Burn: The Hidden Costs of a Warming WorldRating: 1 out of 5 stars1/5 (1)

- A History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationFrom EverandA History of the United States in Five Crashes: Stock Market Meltdowns That Defined a NationRating: 4 out of 5 stars4/5 (11)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassFrom EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassNo ratings yet

- The Technology Trap: Capital, Labor, and Power in the Age of AutomationFrom EverandThe Technology Trap: Capital, Labor, and Power in the Age of AutomationRating: 4.5 out of 5 stars4.5/5 (46)

- The War Below: Lithium, Copper, and the Global Battle to Power Our LivesFrom EverandThe War Below: Lithium, Copper, and the Global Battle to Power Our LivesRating: 4.5 out of 5 stars4.5/5 (9)

- The Meth Lunches: Food and Longing in an American CityFrom EverandThe Meth Lunches: Food and Longing in an American CityRating: 5 out of 5 stars5/5 (5)

- Narrative Economics: How Stories Go Viral and Drive Major Economic EventsFrom EverandNarrative Economics: How Stories Go Viral and Drive Major Economic EventsRating: 4.5 out of 5 stars4.5/5 (94)

- Economics 101: How the World WorksFrom EverandEconomics 101: How the World WorksRating: 4.5 out of 5 stars4.5/5 (34)

- Second Class: How the Elites Betrayed America's Working Men and WomenFrom EverandSecond Class: How the Elites Betrayed America's Working Men and WomenNo ratings yet

- This Changes Everything: Capitalism vs. The ClimateFrom EverandThis Changes Everything: Capitalism vs. The ClimateRating: 4 out of 5 stars4/5 (349)

- The Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaFrom EverandThe Trillion-Dollar Conspiracy: How the New World Order, Man-Made Diseases, and Zombie Banks Are Destroying AmericaNo ratings yet

- University of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingFrom EverandUniversity of Berkshire Hathaway: 30 Years of Lessons Learned from Warren Buffett & Charlie Munger at the Annual Shareholders MeetingRating: 4.5 out of 5 stars4.5/5 (98)

- Economics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsFrom EverandEconomics 101: From Consumer Behavior to Competitive Markets—Everything You Need to Know About EconomicsRating: 5 out of 5 stars5/5 (3)

- Principles for Dealing with the Changing World Order: Why Nations Succeed or FailFrom EverandPrinciples for Dealing with the Changing World Order: Why Nations Succeed or FailRating: 4.5 out of 5 stars4.5/5 (239)

- The Profit Paradox: How Thriving Firms Threaten the Future of WorkFrom EverandThe Profit Paradox: How Thriving Firms Threaten the Future of WorkRating: 4.5 out of 5 stars4.5/5 (13)

- Deaths of Despair and the Future of CapitalismFrom EverandDeaths of Despair and the Future of CapitalismRating: 4.5 out of 5 stars4.5/5 (30)

- Chip War: The Quest to Dominate the World's Most Critical TechnologyFrom EverandChip War: The Quest to Dominate the World's Most Critical TechnologyRating: 4.5 out of 5 stars4.5/5 (230)

- Bad Samaritans: The Myth of Free Trade and the Secret History of CapitalismFrom EverandBad Samaritans: The Myth of Free Trade and the Secret History of CapitalismRating: 4 out of 5 stars4/5 (158)

- Land of Promise: An Economic History of the United StatesFrom EverandLand of Promise: An Economic History of the United StatesRating: 3.5 out of 5 stars3.5/5 (11)

- Look Again: The Power of Noticing What Was Always ThereFrom EverandLook Again: The Power of Noticing What Was Always ThereRating: 5 out of 5 stars5/5 (3)

- The Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetFrom EverandThe Myth of the Rational Market: A History of Risk, Reward, and Delusion on Wall StreetNo ratings yet

- The Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumFrom EverandThe Infinite Machine: How an Army of Crypto-Hackers Is Building the Next Internet with EthereumRating: 3 out of 5 stars3/5 (12)