You might also like

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- 2019 Graduate Outcome SurveyDocument50 pages2019 Graduate Outcome SurveypnrahmanNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Oriental Influence On ThoreauDocument18 pagesOriental Influence On ThoreaupnrahmanNo ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Beal Delpachitra 2005 PVDocument14 pagesBeal Delpachitra 2005 PVpnrahmanNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- Buybacks Around The WorldDocument65 pagesBuybacks Around The WorldpnrahmanNo ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Business School School of Banking & FinanceDocument14 pagesBusiness School School of Banking & FinancepnrahmanNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- 2020 SRG Annual ReportDocument75 pages2020 SRG Annual ReportpnrahmanNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Doing Business in Australia - Business StructuresDocument13 pagesDoing Business in Australia - Business StructurespnrahmanNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Gilbert Tobin 2021 Takeovers and Schemes ReviewDocument72 pagesGilbert Tobin 2021 Takeovers and Schemes ReviewpnrahmanNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- ASIC Crackdown On Related Party Transactions and Experts' Reports - Knowledge - Clayton UtzDocument5 pagesASIC Crackdown On Related Party Transactions and Experts' Reports - Knowledge - Clayton UtzpnrahmanNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Data Analytics Financial ServicesDocument4 pagesData Analytics Financial ServiceskasfurNo ratings yet

- 2020 Canadian Merger Notification Threshold Updates - Lexology - Practical Know-HowDocument3 pages2020 Canadian Merger Notification Threshold Updates - Lexology - Practical Know-HowpnrahmanNo ratings yet

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Applied Corporate Finance: The Fed and The Financial SystemDocument14 pagesApplied Corporate Finance: The Fed and The Financial SystempnrahmanNo ratings yet

- A Guide To MAC Clauses in M&A Transactions - Lexology - Practical Know-HowDocument4 pagesA Guide To MAC Clauses in M&A Transactions - Lexology - Practical Know-HowpnrahmanNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Impactofmerger Jof1982 PDFDocument21 pagesImpactofmerger Jof1982 PDFpnrahmanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- UK Takeover Rules Among Most Stringent Financial TimesDocument2 pagesUK Takeover Rules Among Most Stringent Financial TimespnrahmanNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- NIB 27 10 2008 Rejects ProposalDocument1 pageNIB 27 10 2008 Rejects ProposalpnrahmanNo ratings yet

- Wot SB 2010Document336 pagesWot SB 2010pnrahmanNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Oak TSDocument130 pagesOak TSpnrahmanNo ratings yet

- Review of 2011 Amendment: The Takeover PanelDocument20 pagesReview of 2011 Amendment: The Takeover PanelpnrahmanNo ratings yet

- Oak TSDocument130 pagesOak TSpnrahmanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Media Release: ASX Update - No Formal Proposal ReceivedDocument1 pageMedia Release: ASX Update - No Formal Proposal ReceivedpnrahmanNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- EY - Tax Watch Edition 4, June 2017 - EY - New ZealandDocument2 pagesEY - Tax Watch Edition 4, June 2017 - EY - New ZealandpnrahmanNo ratings yet

- 2006 Webcentral NetRegistryDocument5 pages2006 Webcentral NetRegistrypnrahmanNo ratings yet

- How Does Culture Influence Corporate Risk-TakingDocument22 pagesHow Does Culture Influence Corporate Risk-TakingpnrahmanNo ratings yet

- The Consequences of REIT Index Membership For Return PatternsDocument43 pagesThe Consequences of REIT Index Membership For Return PatternspnrahmanNo ratings yet

- Shroff Et Al - 16.03.2020 (5973)Document20 pagesShroff Et Al - 16.03.2020 (5973)pnrahmanNo ratings yet

- Guide To UK Takeover RegimeDocument44 pagesGuide To UK Takeover RegimepnrahmanNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Super Retail Buys Rebel SportDocument1 pageSuper Retail Buys Rebel SportpnrahmanNo ratings yet

- Dividend Crash Risk PDFDocument61 pagesDividend Crash Risk PDFpnrahmanNo ratings yet

- M&A Sample SlidesDocument10 pagesM&A Sample SlidespnrahmanNo ratings yet

- Deloitte On Business PlanDocument34 pagesDeloitte On Business PlanFaizan Ahmad100% (1)

- 56 - 2001 WinterDocument61 pages56 - 2001 Winterc_mc2100% (1)

- Basel IV Crypto enDocument8 pagesBasel IV Crypto enMorgane FournelNo ratings yet

- Balance Sheet Horizontal Analysis TemplateDocument2 pagesBalance Sheet Horizontal Analysis TemplateArif RahmanNo ratings yet

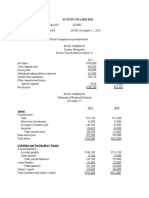

- ACTY04 s.2020 2021Document3 pagesACTY04 s.2020 2021Gelay MagatNo ratings yet

- 2013-10-28 School Board Meeting PDFDocument122 pages2013-10-28 School Board Meeting PDFPress And JournalNo ratings yet

- Summary of Disciplinary Action For Mercer Hicks IIIDocument35 pagesSummary of Disciplinary Action For Mercer Hicks IIIJaymie BaxleyNo ratings yet

- FIN1FOF Assignment - Final 2Document9 pagesFIN1FOF Assignment - Final 21DBA-38 Nguyễn Thị Thanh Tâm100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Investment&Portfolio 260214Document285 pagesInvestment&Portfolio 260214Yonas Tsegaye HaileNo ratings yet

- Algo Trading Intro 2013 Steinki Session 3 PDFDocument15 pagesAlgo Trading Intro 2013 Steinki Session 3 PDFMichael ARKNo ratings yet

- Engro FertilizerDocument9 pagesEngro FertilizerAbdullah Sohail100% (1)

- Baglamukhi Masala Fs 2076-77Document44 pagesBaglamukhi Masala Fs 2076-77sudhakar ShakyaNo ratings yet

- Apple FinancialsDocument214 pagesApple FinancialsAli HafeezNo ratings yet

- ALCHEMY HG Select - Oct-19Document2 pagesALCHEMY HG Select - Oct-19Motilal Oswal Financial ServicesNo ratings yet

- CM&SLDocument554 pagesCM&SLeducational797No ratings yet

- Offer Letter For CPS ConversionDocument3 pagesOffer Letter For CPS ConversionShah QayyumNo ratings yet

- 121000008-890223086161x - Product Disclosure Sheet FinalDocument9 pages121000008-890223086161x - Product Disclosure Sheet FinalpubalanNo ratings yet

- Choose A Forex BrokerDocument1 pageChoose A Forex BrokerMed MesNo ratings yet

- ACCT 411-Applied Financial Analysis-Arslan Shahid Butt PDFDocument7 pagesACCT 411-Applied Financial Analysis-Arslan Shahid Butt PDFAbdul Basit JavedNo ratings yet

- Unit-1 Introduction To Managerial EconomicsDocument13 pagesUnit-1 Introduction To Managerial EconomicsAsmish EthiopiaNo ratings yet

- Partnership Formation Activity 2Document4 pagesPartnership Formation Activity 2Shaira Untalan100% (1)

- CREDITFAQ31 The Debt Service Coverage Ratio 092016Document4 pagesCREDITFAQ31 The Debt Service Coverage Ratio 092016handsomepeeyushNo ratings yet

- Bullish or BearishDocument10 pagesBullish or Bearishadebayoexcel2006No ratings yet

- Chapter 10 - Bond Prices and YieldsDocument42 pagesChapter 10 - Bond Prices and YieldsA_Students100% (3)

- Starbucks Analylsis 2Document26 pagesStarbucks Analylsis 2api-321188189No ratings yet

- Buyback Letter of OfferDocument3 pagesBuyback Letter of OfferNarNo ratings yet

- FAR210 - Feb 2023 - SSDocument11 pagesFAR210 - Feb 2023 - SSfarisha aliahNo ratings yet

- Lenskart CaseDocument2 pagesLenskart CaseManas ChoudhuryNo ratings yet

- JLR Bond Valuation - Adit - P41065Document7 pagesJLR Bond Valuation - Adit - P41065Adit Shah100% (2)

- Abm 2 DiagnosticsDocument2 pagesAbm 2 DiagnosticsDindin Oromedlav LoricaNo ratings yet

- Summary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisFrom EverandSummary of The Black Swan: by Nassim Nicholas Taleb | Includes AnalysisRating: 5 out of 5 stars5/5 (6)

- 2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNFrom Everand2019 Business Credit with no Personal Guarantee: Get over 200K in Business Credit without using your SSNRating: 4.5 out of 5 stars4.5/5 (3)

- The Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursFrom EverandThe Six Secrets of Raising Capital: An Insider's Guide for EntrepreneursRating: 4.5 out of 5 stars4.5/5 (8)

- The Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingFrom EverandThe Masters of Private Equity and Venture Capital: Management Lessons from the Pioneers of Private InvestingRating: 4.5 out of 5 stars4.5/5 (17)

- Finance Basics (HBR 20-Minute Manager Series)From EverandFinance Basics (HBR 20-Minute Manager Series)Rating: 4.5 out of 5 stars4.5/5 (32)

- These are the Plunderers: How Private Equity Runs—and Wrecks—AmericaFrom EverandThese are the Plunderers: How Private Equity Runs—and Wrecks—AmericaRating: 4.5 out of 5 stars4.5/5 (14)

- The Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetFrom EverandThe Caesars Palace Coup: How a Billionaire Brawl Over the Famous Casino Exposed the Power and Greed of Wall StreetRating: 5 out of 5 stars5/5 (2)