SOTE TWAWEZA 2012

MODULE 5 TPS FINANCIAL REPORTING

notes

- value in use (VU). NFV is the sales price of an asset in an arms length transaction less the costs of disposal. VU is the present value (PV) of future cash flows expected to arise from the asset over its remaining life and from its disposal. In other words we are looking at the financial outcome of the two choices a company has with an asset: keep it (VU), or sell it (NFV). The higher is taken as it is assumed that the company will opt for the more beneficial outcome. Example 1 A fixed asset was acquired in January 2008 for 200,000. Depreciation policy is 15% straight line with a nil estimated residual value. At 1 January 2011 the NFV of the asset is 95,000 and the value in use is estimated at 87,000.

Required: Calculate the amount of any impairment at 1 January 2011.

Solution NBV (carrying amount) of asset at 1.1.11 Cost Less: depreciation 2008-10 (200,000 x 15% x 3 years) NBV 1.1.11

200,000 90,000 110,000

Recoverable amount This is measured as the higher of NFV and VU (higher of 95,000 and 87,000) ie 95,000. As the recoverable amount is 95,000, there has been an impairment of 15,000 (carrying amount of 110,000 less 95,000).

5.4 REQUIREMENT FOR IMPAIRMENT REVIEWS

The directors of a company should assess at each balance sheet date whether there are indications of impairment. If there are, the recoverable amount should be calculated (para 9). Para 12 details some external and internal sources of information that might indicate an impairment eg falls in market values, changes in legislation, physical damage of an asset, operating losses, new competition. Para 10 has additional requirements for intangible assets and goodwill. A company should estimate the recoverable amount of the following assets at least annually even if there is no indication that the asset is impaired: (a) (b) an intangible asset with an indefinite useful life; and an intangible asset not yet available for use.

In addition, goodwill acquired in a business combination should be tested for impairment annually.

2

SOTE TWAWEZA 2012

TPS FINANCIAL REPORTING MODULE 5

The following points should be noted in calculating the carrying amount of a CGU: (i) includes only those assets that can be attributed directly, or allocated on a reasonable and consistent basis, to the CGU and that will generate the future cash flows. This will normally include tangible and intangible fixed assets and goodwill (see (iii) below); exclude liabilities unless the recoverable amount cannot be determined without considering the liability eg if a CGU has an obligation to repair goods under warranty the NFV (and hence recoverable amount) will reflect this obligation as it is unlikely the CGU would be sold without transferring the liability at the same time. The liability should be included and the cash flows should reflect estimated repair costs under warranty. This will give consistency in the way carrying amount, NFV and VU are calculated. goodwill should be allocated to individual CGUs if they benefit from synergies of the business combination. Section 5.9 deals with goodwill in more detail. corporate assets (assets such as head office buildings, central computing facilities etc which serve more than one CGU) should be allocated to CGUs if possible. Refer to 5.9 where this is not possible. Example 2 Jackson Ltd (Jackson) acquired 100% of the ordinary share capital of James Ltd (James) for 10 million on 1 January 2004. This figure included 960,000 for goodwill. Jackson is preparing group accounts for the year to 31 December 2010 and due to a decline in market conditions has decided to carry out an impairment review of the fixed assets and goodwill of James. James operates in two distinct business areas which are largely independent one is services to the oil industry and the other is the operation of a rail franchise. The following assets have been attributed to these activities as follows: Oil services 000 Fixed assets Tangible Intangible 10,000 10,000 Rail franchise 000 6,900 1,200 8,100

notes

(ii)

(iii)

(iv)

All fixed assets are held at depreciated cost.

SOTE TWAWEZA 2012

MODULE 5 TPS FINANCIAL REPORTING

notes

The following items have still to be allocated: (a) head office property with a net book value of 3,200,000. It is estimated that this can be split 60:40 between oil and rail. goodwill it is estimated that 75% of this relates to the rail franchise and the remainder to oil.

(b)

The directors estimate that the rail franchise has a NFV of 7,500,000 and oil services a NFV of 9,600,000. The intangible asset in the rail franchise relates to the NBV of the operating license associated with the franchise. The following pre-tax cash flows have been estimated for each CGU: Oil services 000 3,000 2,800 2,800 4,800* Rail franchise 000 4,200 3,400 3,400*

Year 2011 2012 2013 2014

* the rail franchise expires at the end of 2013 and the oil services division will be wound up in 2014. The pre-tax market rate of return for oil services is estimated at 15% and 20% for the rail franchise.

Required: (i) Calculate the total net assets for each CGU; (ii) Calculate the value in use for each CGU; (iii) Calculate the impairment (if any) for each CGU.

Note: The present value of 1 at the end of each year using a discount rate of 15% and 20% is as follows: End of year 1 2 3 4 Amount at 15% 0.870 0.756 0.658 0.572 Amount at 20% 0.833 0.694 0.579 0.482

SOTE TWAWEZA 2012

TPS FINANCIAL REPORTING MODULE 5

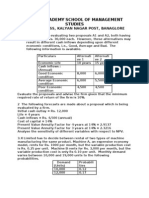

Solution (i) Total net assets Oil services 000 Rail franchise 000

notes

(ii)

Calculation of value in use This is based on discounted cash flows. These can be calculated (to nearest 000) as: Oil services 000 9,315 Rail franchise 000 7,828

Workings: Value in use Oil services Year Discount factor (15%) 0.870 0.756 0.658 0.572 Cash flow 000 3,000 2,800 2,800 4,800 PV 000 2,610 2,117 1,842 2,746 9,315 Rail franchise Discount factor (20%) 0.833 0.694 0.579 Cash flow 000 4,200 3,400 3,400 PV 000 3,499 2,360 1,969 ____ 7,828

2011 2012 2013 2014 (iii)

Calculation of impairment Oil services 000 Rail franchise 000

You will now be able to achieve the second learning objective of this module.

7

SOTE TWAWEZA 2012

MODULE 5 TPS FINANCIAL REPORTING

notes

5.7 ACCOUNTING FOR AN IMPAIRMENT LOSS

Loss for an individual asset (para 58 64) the asset should be written-down to recoverable amount if this is below the carrying amount. the loss should be an expense in profit or loss, except when the asset has been previously revalued. if the asset is carried at revalued amount the impairment loss should be treated as a revaluation loss per IAS 16 or IAS 38, hence a debit to the revaluation reserve in the first instance with any excess loss taken to profit or loss if the impaired asset has been revalued the impairment loss should be treated as a new revaluation. If the asset is at cost the impairment loss is additional depreciation. after the impairment loss has been recognised depreciation is based on the adjusted carrying amount of the asset. Loss for CGU (para 104 108) the loss should be allocated by writing-down assets in the CGU in the following order: (a) first, any goodwill allocated to the CGU; (b) then, to other assets in the CGU pro-rata on carrying amount. In carrying out (b) no individual assets in the CGU should be written-down below the highest of: (a) its NFV (if determinable); (b) its VU (if determinable); and (c) zero. Applying (a) and (b) means that no asset is written-down below a known value. In this case, the amount of loss not deducted from the carrying amount of the individual asset is spread pro rata over other assets in the unit. The other rules above relating to individual assets apply to a CGU eg loss to profit or loss/revaluation reserve. Example 3 How would the impairment of the assets of James in example 2 be recorded as at 31 December 2010? Solution There is no indication that any specific assets are impaired. The assets are held at cost therefore losses go to profit or loss. The write-down should be treated as additional depreciation. Oil services The impairment loss would first be allocated to the goodwill (240,000) and then to tangible fixed assets (remaining loss of 2,320,000). Each tangible fixed asset would be written-down by 19.46% (2,320/(10,000 + 1,920)).

SOTE TWAWEZA 2012

TPS FINANCIAL REPORTING MODULE 5

000

000

notes

Rail franchise The impairment should first be allocated to goodwill, then to the other assets. No distinction is made between intangible and tangible assets the impairment loss is allocated proportionately.

Once goodwill has been written-off, the remaining impairment loss of 1,552,000 (2,272,000 - 720,000) needs to be pro-rated between the remaining assets. NBV of remaining assets Directly attributable - tangible - intangible Head office - tangible The allocation of the loss is as follows: Working Tangible fixed assets Intangible fixed assets NBV 8,180 1,200 9,380 % 87.2 12.8 100.0 Loss allocated 1,353 199 1,552 Rail 000 6,900 1,200 1,280 9,380

Example 4 Assume in the rail franchise of James it was known that the operating licence (the intangible asset) had a net fair value (NFV) of 1,100,000. As the licence does not itself generate cash flow it is not possible to calculate its VU. What effect would this have on the write-off of the impairment loss? Solution The goodwill should still be written-off. The operating licence should not be written-down below the higher of NFV (1.1m) and VU (not available) ie by a maximum of 100,000 (1.2m - 1.1m). The remainder of the loss should be allocated to the remaining tangible fixed assets pro rata.

SOTE TWAWEZA 2012

TPS FINANCIAL REPORTING MODULE 5

Example 5 A CGU comprising a factory, plant and equipment etc and associated goodwill became impaired because its products became out of date and unattractive compared to those of competitors. The recoverable amount fell to 25m at 31 December 2006, resulting in an impairment loss of 15m, allocated as follows: Carrying amounts before impairment based on HC m Goodwill 10 Factory 12 Plant and machinery 18 Total 40 Carrying amounts after impairment m 10 15 25

notes

The impairment loss of 15m was recognised in profit or loss as the assets were at historic cost. By 31 December 2010 the entity had improved its product range substantially by adding new models and the recoverable amount of the CGU increased to 30m. The carrying amounts of the factory and plant and machinery at 31 December 2010 are as follows: Based on Had no impairment impairment values occurred m m Factory Plant and machinery 9.0 12.0 10.8 14.4

The recoverable amount of the plant and machinery is estimated to be 13m. The recoverable amount of the factory is estimated to be 15m. Goodwill is estimated to be worth around 2m.

Required: Explain how the reversal of the impairment loss should be accounted for.

Solution

11

You might also like

- Impairment of Assets NotesDocument23 pagesImpairment of Assets NotesGeorge Buliki100% (1)

- IAS 36 Impairment of Assets (2021)Document12 pagesIAS 36 Impairment of Assets (2021)Tawanda Tatenda HerbertNo ratings yet

- IAS 36 Impairment of AssetsDocument22 pagesIAS 36 Impairment of AssetsZeeshan Mahmood100% (1)

- Hock 2020 Part 1 Section A - External Financial Reporting Decisions AnswersDocument237 pagesHock 2020 Part 1 Section A - External Financial Reporting Decisions AnswersAhad chy100% (1)

- IAS 16 PPE Practice QuestionsDocument2 pagesIAS 16 PPE Practice QuestionsMyo Naing88% (25)

- Non Current Asset Held For Sale Final-1Document29 pagesNon Current Asset Held For Sale Final-1nati100% (4)

- Chapter 8: Ias 12 Income Taxes: QuestionsDocument7 pagesChapter 8: Ias 12 Income Taxes: Questionsmary100% (2)

- IAS 38 Question 6Document2 pagesIAS 38 Question 6tazil shahNo ratings yet

- 62230126Document20 pages62230126ROMULO CUBIDNo ratings yet

- Accounting For Biological Asset Tutorial IVDocument5 pagesAccounting For Biological Asset Tutorial IVJohn TomNo ratings yet

- Past Exam Answer Key (To Consol BS)Document53 pagesPast Exam Answer Key (To Consol BS)Huệ LêNo ratings yet

- Sums On Project AnalysisDocument26 pagesSums On Project AnalysisAlbert Thomas80% (5)

- Ch08 Property, Plant & EquipmentDocument6 pagesCh08 Property, Plant & EquipmentralphalonzoNo ratings yet

- IAS-10 and IAS-37 Solutions Practice QuestionsDocument13 pagesIAS-10 and IAS-37 Solutions Practice QuestionsAbdul SamiNo ratings yet

- PPE Accounting PrinciplesDocument6 pagesPPE Accounting Principlesmae cruzNo ratings yet

- Fair ValueDocument44 pagesFair Valuenati100% (1)

- Final Exam - FA2 (Shareholders Equity) With QuestionsDocument10 pagesFinal Exam - FA2 (Shareholders Equity) With Questionsjanus lopezNo ratings yet

- IAS-41 AGRICULTURE ACCOUNTINGDocument3 pagesIAS-41 AGRICULTURE ACCOUNTINGÃhmed AliNo ratings yet

- 7 - Property, Plant and Equipment and Related Accounts Theory of AccountsDocument15 pages7 - Property, Plant and Equipment and Related Accounts Theory of AccountsandreamrieNo ratings yet

- DepletionDocument6 pagesDepletionjemjem14No ratings yet

- Financial Accounting and Reporting: Small and Medium-Sized EntitiesDocument19 pagesFinancial Accounting and Reporting: Small and Medium-Sized EntitiesDan DiNo ratings yet

- ACC 577 Quiz Week 2Document11 pagesACC 577 Quiz Week 2MaryNo ratings yet

- Topic 3 Tutorial Questions PDFDocument15 pagesTopic 3 Tutorial Questions PDFKim FloresNo ratings yet

- Revaluation ModelDocument33 pagesRevaluation ModelLumongtadJoanMaeNo ratings yet

- IAS 16 Property Plant Equipment OverviewDocument7 pagesIAS 16 Property Plant Equipment OverviewAdeel Shoukat100% (3)

- Impairment of Asset: Cash Generating UnitDocument28 pagesImpairment of Asset: Cash Generating UnitLumongtadJoanMaeNo ratings yet

- Far2921investments in Debt Instruments PDF FreeDocument6 pagesFar2921investments in Debt Instruments PDF FreeMarcus MonocayNo ratings yet

- Chapter 1 Joint Arrangements & PEDocument36 pagesChapter 1 Joint Arrangements & PEMati MeseretNo ratings yet

- Financial InstrumentsDocument93 pagesFinancial InstrumentsLuisa Janelle BoquirenNo ratings yet

- Biological Assets: Multiple Choice Questions & Problem Solving QuestionsDocument19 pagesBiological Assets: Multiple Choice Questions & Problem Solving QuestionsAIKO MAGUINSAWANNo ratings yet

- Depreciation, Asset Costs, Capitalization SEODocument7 pagesDepreciation, Asset Costs, Capitalization SEOLara Lewis Achilles50% (2)

- Chapter 3: Business Combination: Based On IFRS 3Document38 pagesChapter 3: Business Combination: Based On IFRS 3ሔርሞን ይድነቃቸውNo ratings yet

- Exercise 6 - 1 Multiple Choice QuestionsDocument3 pagesExercise 6 - 1 Multiple Choice QuestionsYrica100% (1)

- ACTG 431 QUIZ Week 2 Theory of Accounts Part 2 - FINANCIAL ASSETS QUIZDocument6 pagesACTG 431 QUIZ Week 2 Theory of Accounts Part 2 - FINANCIAL ASSETS QUIZMarilou Arcillas PanisalesNo ratings yet

- Compound Financial Instruments and Note PayableDocument4 pagesCompound Financial Instruments and Note PayablePaula Rodalyn MateoNo ratings yet

- IAS 16 (CAF5 S18) : (I) (Ii) (Iii) - Rs. in MillionDocument41 pagesIAS 16 (CAF5 S18) : (I) (Ii) (Iii) - Rs. in MillionShameel IrshadNo ratings yet

- PAS 23 Borrowing Costs CapitalizationDocument34 pagesPAS 23 Borrowing Costs CapitalizationRigine Pobe Morgadez100% (1)

- Ias 2 Questions and AnswersDocument3 pagesIas 2 Questions and AnswersShameel Irshad75% (8)

- DWC Legazpi Practical Accounting One LiabilitiesDocument14 pagesDWC Legazpi Practical Accounting One Liabilitiesyukiro rineva0% (2)

- Module 4 - ImpairmentDocument5 pagesModule 4 - ImpairmentLuiNo ratings yet

- Understanding the Requirements for Reclassification of Financial AssetsDocument9 pagesUnderstanding the Requirements for Reclassification of Financial AssetsTurksNo ratings yet

- Property Plant and Equipment QuizDocument2 pagesProperty Plant and Equipment Quizabdulmut100% (1)

- Mas Handout 1Document13 pagesMas Handout 1Rue Scarlet100% (2)

- Initial Cash FlowDocument3 pagesInitial Cash FlowNouman Mujahid50% (2)

- Plant and equipment accountingDocument3 pagesPlant and equipment accountingVivek Pange0% (1)

- Intermediate Accounting Exam 11Document2 pagesIntermediate Accounting Exam 11BLACKPINKLisaRoseJisooJennieNo ratings yet

- IAS 23 Borrowing Costs CapitalizationDocument10 pagesIAS 23 Borrowing Costs CapitalizationMaria100% (1)

- Quiz FinalDocument6 pagesQuiz FinalChriztel Joy Manansala100% (1)

- Module 12 - Investment PropertyDocument15 pagesModule 12 - Investment PropertyJehPoyNo ratings yet

- MODULE 30 Non-Current Assets Held For SaleDocument8 pagesMODULE 30 Non-Current Assets Held For SaleAngelica Sanchez de VeraNo ratings yet

- Long-Term Liabilities AnswersDocument15 pagesLong-Term Liabilities AnswersNicoleNo ratings yet

- ReviewerDocument5 pagesReviewermaricielaNo ratings yet

- Define Business Combination, Identify Its ElementsDocument4 pagesDefine Business Combination, Identify Its ElementsAljenika Moncada GupiteoNo ratings yet

- Exercise - IAS 23 Borrowing CostsDocument6 pagesExercise - IAS 23 Borrowing CostsMazni Hanisah100% (1)

- Quiz Biological AssetsDocument3 pagesQuiz Biological AssetsRocel DomingoNo ratings yet

- Midterm SheDocument5 pagesMidterm SheKaye Delos SantosNo ratings yet

- Chapter 14 - Retail Inventory Method PDFDocument9 pagesChapter 14 - Retail Inventory Method PDFTurksNo ratings yet

- Impairment of Assets Solutions PDF FreeDocument7 pagesImpairment of Assets Solutions PDF FreeJohn Miguel GordoveNo ratings yet

- SM CHDocument53 pagesSM CHInderjeet JeedNo ratings yet

- Ias 12,7 Ifrs 9Document10 pagesIas 12,7 Ifrs 9AssignemntNo ratings yet

- Using Technology To Enhance Internal Audit IA ProcessDocument28 pagesUsing Technology To Enhance Internal Audit IA ProcessGeorge BulikiNo ratings yet

- Tanzania Land PolicyDocument10 pagesTanzania Land PolicyGeorge BulikiNo ratings yet

- CV Writing TipsDocument1 pageCV Writing TipsGeorge BulikiNo ratings yet

- Advanced Variance 5.9Document2 pagesAdvanced Variance 5.9George Buliki100% (1)

- Products Materials: Solution To QN 5.10Document4 pagesProducts Materials: Solution To QN 5.10George BulikiNo ratings yet

- CV SampleDocument2 pagesCV SampleGeorge BulikiNo ratings yet

- Solution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesDocument10 pagesSolution To QN 6 (PG 135) : Calculation of Overhead Absorption RatesGeorge BulikiNo ratings yet

- Variance 5.13Document3 pagesVariance 5.13George BulikiNo ratings yet

- Liquidation Qn3Document6 pagesLiquidation Qn3George BulikiNo ratings yet

- Variance Analysis 5.16Document3 pagesVariance Analysis 5.16George BulikiNo ratings yet

- Budgeting 2.25Document3 pagesBudgeting 2.25George BulikiNo ratings yet

- Variance Analysis 5.15Document7 pagesVariance Analysis 5.15George BulikiNo ratings yet

- Soln To 8.9Document1 pageSoln To 8.9George BulikiNo ratings yet

- Performance 6.10Document3 pagesPerformance 6.10George BulikiNo ratings yet

- Advanced Variance 5.8Document4 pagesAdvanced Variance 5.8George BulikiNo ratings yet

- Solution To QN 7.10Document1 pageSolution To QN 7.10George BulikiNo ratings yet

- Advanced Variance 5.7Document4 pagesAdvanced Variance 5.7George BulikiNo ratings yet

- Performance 6.10Document2 pagesPerformance 6.10George BulikiNo ratings yet

- Solution To QN 7.10Document2 pagesSolution To QN 7.10George BulikiNo ratings yet

- Transfer Pricing 8.12 BDocument2 pagesTransfer Pricing 8.12 BGeorge BulikiNo ratings yet

- Transfer Pricing 8.7 BDocument2 pagesTransfer Pricing 8.7 BGeorge BulikiNo ratings yet

- Pricing 7.13Document1 pagePricing 7.13George BulikiNo ratings yet

- Variance Analysis 5.11Document2 pagesVariance Analysis 5.11George Buliki100% (2)

- Solution To QN 7.10Document2 pagesSolution To QN 7.10George BulikiNo ratings yet

- Perfomance6 15Document2 pagesPerfomance6 15George BulikiNo ratings yet

- Harden Company Case StudyDocument2 pagesHarden Company Case StudyGeorge Buliki100% (1)

- NBAA SyllabusDocument100 pagesNBAA SyllabusHamis ShekibulaNo ratings yet

- Limitations of Conceptual Framework PDFDocument20 pagesLimitations of Conceptual Framework PDFGeorge Buliki100% (25)

- Awash Bank OverviewDocument7 pagesAwash Bank OverviewAndrew Hoth Kang75% (8)

- Return Risk and SMLDocument3 pagesReturn Risk and SMLspectrum_48No ratings yet

- Chapter - 8Document14 pagesChapter - 8Huzaifa Malik100% (1)

- MAFC Research Papers: Hedge Funds: A Walk Through The GraveyardDocument30 pagesMAFC Research Papers: Hedge Funds: A Walk Through The GraveyardPooja JainNo ratings yet

- R Money Sip Presentation by Ravish Roshandelhi 1223401016149009 9Document19 pagesR Money Sip Presentation by Ravish Roshandelhi 1223401016149009 9Yukti KhoslaNo ratings yet

- Audit Report of Axis BankDocument51 pagesAudit Report of Axis BanksangeethaNo ratings yet

- Retail Financial Strategy: ROA AnalysisDocument19 pagesRetail Financial Strategy: ROA AnalysisSanjini GautamNo ratings yet

- Financial analysis insightsDocument13 pagesFinancial analysis insightsRahul KamathNo ratings yet

- Glover Lawrence Full Resume For HBRDocument3 pagesGlover Lawrence Full Resume For HBRat3mail100% (1)

- Simple Interest CalculationDocument7 pagesSimple Interest CalculationBeybi EstebanNo ratings yet

- MEFTEC 2012 Exhibitor Brochure - DubaiDocument6 pagesMEFTEC 2012 Exhibitor Brochure - DubaisaudghayasNo ratings yet

- Bab 9 MIPDocument24 pagesBab 9 MIPAprilia MarshyaNo ratings yet

- Financial Payout Request Form - Updated - tcm47-63340Document16 pagesFinancial Payout Request Form - Updated - tcm47-63340Jane Tallar Rodrigueza100% (1)

- Value Creation PDFDocument30 pagesValue Creation PDFAntoanela MihăilăNo ratings yet

- Introduction To Banking, International Banking and FinanceDocument3 pagesIntroduction To Banking, International Banking and Financepayal sachdevNo ratings yet

- Money MarketDocument17 pagesMoney MarketAbid faisal AhmedNo ratings yet

- LexDocument9 pagesLexKaustav DeyNo ratings yet

- Presentation On Auction Theory by Simon HerrmannDocument16 pagesPresentation On Auction Theory by Simon Herrmannsimon.herrmann4368No ratings yet

- Ott AppformDocument2 pagesOtt Appformsujay13780No ratings yet

- ISOM 5510 Data Analysis Group Project 14 - 3Document7 pagesISOM 5510 Data Analysis Group Project 14 - 3Ameya PanditNo ratings yet

- Factors Affecting The Fluctuations in Exchange Rate of The Indian Rupee Group 9 C2Document13 pagesFactors Affecting The Fluctuations in Exchange Rate of The Indian Rupee Group 9 C2muralib4u5No ratings yet

- FD Course OutlineDocument8 pagesFD Course OutlineSudip ThakurNo ratings yet

- FinanceDocument6 pagesFinanceIssac KNo ratings yet

- Trai Phieu 14Document6 pagesTrai Phieu 14NguyenNo ratings yet

- The Efficient Market HypothesisDocument31 pagesThe Efficient Market HypothesisKoon Sing ChanNo ratings yet

- The Bank AccountDocument15 pagesThe Bank AccountJerima PilleNo ratings yet

- Types of Mutual Funds Based on Asset Class, Structure, Goals and RiskDocument5 pagesTypes of Mutual Funds Based on Asset Class, Structure, Goals and RiskVishal DudejaNo ratings yet

- Marilog High School of Agriculture General Mathematics Final ExamDocument2 pagesMarilog High School of Agriculture General Mathematics Final ExamJeffren P. Miguel100% (3)

- 2 - Drobetz (2001)Document18 pages2 - Drobetz (2001)jjkkkkjkNo ratings yet