You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1091)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Payment Schedule: Computation Sheet Bank FinancingDocument3 pagesPayment Schedule: Computation Sheet Bank FinancingJam SarimosNo ratings yet

- Myjobmag-Banking-Entry Level-CVDocument1 pageMyjobmag-Banking-Entry Level-CVkassimmakoy05No ratings yet

- Credit RatingDocument18 pagesCredit Ratingrameshmba100% (10)

- Ayukoben AyambaDocument41 pagesAyukoben AyambaLoveline Manong FombeleNo ratings yet

- Blank Quiz q2 WK 1 Written WorksDocument4 pagesBlank Quiz q2 WK 1 Written WorksDeanna Kate Balais100% (1)

- ICEA Annuity Proposal FormDocument2 pagesICEA Annuity Proposal Formkevin muchungaNo ratings yet

- Accounting ChapterDocument66 pagesAccounting ChapterBrisa MasiniNo ratings yet

- The Hydrogenics Case Is The First in A Series ofDocument2 pagesThe Hydrogenics Case Is The First in A Series ofAmit PandeyNo ratings yet

- Department of Education: Region IX, Zamboanga Peninsula Division of Zamboanga City Tolosa, Zamboanga CityDocument1 pageDepartment of Education: Region IX, Zamboanga Peninsula Division of Zamboanga City Tolosa, Zamboanga CityRay FaustinoNo ratings yet

- Account Statement: Generated On Sunday, April 16, 2023 6:05:49 AMDocument1 pageAccount Statement: Generated On Sunday, April 16, 2023 6:05:49 AMPatience AkpanNo ratings yet

- Account Statement From 1 Apr 2018 To 31 Mar 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument8 pagesAccount Statement From 1 Apr 2018 To 31 Mar 2019: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceNarendra SaiNo ratings yet

- Resume Internal Audit and Enterprise GovernanceDocument6 pagesResume Internal Audit and Enterprise GovernanceAnnisa Rahman DhitaNo ratings yet

- Final Question Bank With Answers - Treasury Management-Final ExamDocument7 pagesFinal Question Bank With Answers - Treasury Management-Final ExamHarsh MaheshwariNo ratings yet

- IES-Template For Preparing Cover LetterDocument1 pageIES-Template For Preparing Cover LetterkizztarNo ratings yet

- State Bank of India: Application Form Atm Transaction DisputeDocument6 pagesState Bank of India: Application Form Atm Transaction DisputeSandeep YadavNo ratings yet

- Test Paper CA Final TpdtaaDocument3 pagesTest Paper CA Final TpdtaayeidaindschemeNo ratings yet

- Computations For Budgeted Figures in The Master Budget-Trading ConcernDocument2 pagesComputations For Budgeted Figures in The Master Budget-Trading ConcernZackie LouisaNo ratings yet

- ICDS - 9 Borrowing CostDocument15 pagesICDS - 9 Borrowing Costkavita.m.yadavNo ratings yet

- HUF FormatsDocument2 pagesHUF FormatsVinay TotlaNo ratings yet

- Sdlkfjasd LFKDocument66 pagesSdlkfjasd LFKTerryLasutNo ratings yet

- Statement 20230202Document10 pagesStatement 20230202philip balsomNo ratings yet

- Retail BankingDocument9 pagesRetail BankingBebin RoseNo ratings yet

- Risk and InsuranceDocument63 pagesRisk and InsuranceGuruKPO100% (2)

- Advocates For Truth in Lending, Inc. vs. Bangko Sentral Monetary BoardDocument2 pagesAdvocates For Truth in Lending, Inc. vs. Bangko Sentral Monetary BoardylourahNo ratings yet

- G Dividend PolicyDocument7 pagesG Dividend PolicySweeti JaiswalNo ratings yet

- ch9 1Document33 pagesch9 1Sai Karthik BaggamNo ratings yet

- Lecture Guide 15 - KeyDocument5 pagesLecture Guide 15 - KeyFrancis VirayNo ratings yet

- IFP From ScotiaDocument11 pagesIFP From ScotiaForexliveNo ratings yet

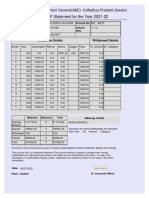

- GPF Statement For The Year 2021-22: O/o The Pr. Accountant General (A&E) - II, Madhya Pradesh, GwaliorDocument1 pageGPF Statement For The Year 2021-22: O/o The Pr. Accountant General (A&E) - II, Madhya Pradesh, GwaliorSHIVGOPAL KULHADENo ratings yet

- Balance StatementDocument4 pagesBalance StatementVitor BinghamNo ratings yet