You might also like

- Graham and Doddsville Winter 2012Document52 pagesGraham and Doddsville Winter 2012waterhousebNo ratings yet

- USREITs REITs 101 - An IntroductionDocument89 pagesUSREITs REITs 101 - An Introductiong4nz0No ratings yet

- Sample Business Plan - Real Estate DevelopmentDocument78 pagesSample Business Plan - Real Estate Developmentg4nz094% (18)

- 2012-2014-Real Estate Land Bus PlanDocument55 pages2012-2014-Real Estate Land Bus Plang4nz0No ratings yet

- Graham & Doddsville - Issue 15 - Spring 2012Document64 pagesGraham & Doddsville - Issue 15 - Spring 2012bijueNo ratings yet

- Garbis - Tranquility at Fredericktown A Value Add Investment Proposition - 2009 - RosenbergDocument99 pagesGarbis - Tranquility at Fredericktown A Value Add Investment Proposition - 2009 - Rosenbergg4nz0No ratings yet

- Graham & Doddsville 20091009Document29 pagesGraham & Doddsville 20091009wrolosonNo ratings yet

- Graham & Doddsville: - Larry RobbinsDocument54 pagesGraham & Doddsville: - Larry RobbinsSaurabh DasNo ratings yet

- Graham and Doddsville - Issue 13 - Fall 2011Document34 pagesGraham and Doddsville - Issue 13 - Fall 2011g4nz0No ratings yet

- Graham and Doddsville - Issue 9 - Spring 2010Document33 pagesGraham and Doddsville - Issue 9 - Spring 2010g4nz0No ratings yet

- Graham and Doddsville Newsletter Fall 2010Document35 pagesGraham and Doddsville Newsletter Fall 2010Jean-Marie TruelleNo ratings yet

- Act 83 of 2010 Renewable Incentives Bill Oficial EnglishDocument77 pagesAct 83 of 2010 Renewable Incentives Bill Oficial Englishg4nz0No ratings yet

- Graham and Doddsville - Issue 12 - Spring 2011Document27 pagesGraham and Doddsville - Issue 12 - Spring 2011g4nz0No ratings yet

- Graham and Doddsville - Issue 8 Winter 2010Document35 pagesGraham and Doddsville - Issue 8 Winter 2010tatsrus1No ratings yet

- ModulosDocument7 pagesModulosg4nz0No ratings yet

- Graham and Doddsville - Issue 5 Winter 2009Document35 pagesGraham and Doddsville - Issue 5 Winter 2009tatsrus1No ratings yet

- Graham and Doddsville - Issue 6 - Summer 2009Document37 pagesGraham and Doddsville - Issue 6 - Summer 2009g4nz0No ratings yet

- Selected Treasury 1603 Grant MaterialsDocument133 pagesSelected Treasury 1603 Grant Materialsg4nz0No ratings yet

- Graham and Doddsville - Issue 1 - Winter 2006Document22 pagesGraham and Doddsville - Issue 1 - Winter 2006David KesslerNo ratings yet

- Graham and Doddsville - Issue 3 - Winter 2007Document23 pagesGraham and Doddsville - Issue 3 - Winter 2007g4nz0No ratings yet

- InversoresDocument2 pagesInversoresg4nz0No ratings yet

- Act 82 Energy Diversification ActDocument22 pagesAct 82 Energy Diversification Actg4nz0No ratings yet

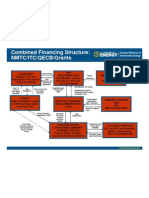

- Solar NMTC StructureDocument1 pageSolar NMTC Structureg4nz0No ratings yet

- Monish PabraiDocument22 pagesMonish PabraiDavid SobkowiczNo ratings yet

- 2010PRCC PrepaDocument32 pages2010PRCC Prepag4nz0No ratings yet

- Gold vs. Model: Date Ibbotson Real R 2% Deflatoadjusted F Inversion Leverage Model GoldDocument6 pagesGold vs. Model: Date Ibbotson Real R 2% Deflatoadjusted F Inversion Leverage Model Goldg4nz0No ratings yet

- Building Energy Efficiency Retrofit FormsDocument5 pagesBuilding Energy Efficiency Retrofit Formsg4nz0No ratings yet

- Sun Energy FormsDocument4 pagesSun Energy Formsg4nz0No ratings yet

- Wind Energy FormsDocument5 pagesWind Energy Formsg4nz0No ratings yet

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (120)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- AMX Prodigy Install ManualDocument13 pagesAMX Prodigy Install Manualsundevil2010usa4605No ratings yet

- Simple Past Lastdinezqm7Document16 pagesSimple Past Lastdinezqm7Esin ErgeneNo ratings yet

- Lecture 5: Triangulation Adjustment Triangulation: in This Lecture We Focus On The Second MethodDocument5 pagesLecture 5: Triangulation Adjustment Triangulation: in This Lecture We Focus On The Second MethodXogr BargarayNo ratings yet

- Accounting For A Service CompanyDocument9 pagesAccounting For A Service CompanyAnnie RapanutNo ratings yet

- One God One People February 2013Document297 pagesOne God One People February 2013Stig DragholmNo ratings yet

- PD750-01 Engine Data Sheet 12-29-20Document4 pagesPD750-01 Engine Data Sheet 12-29-20Service Brags & Hayes, Inc.No ratings yet

- Market Challengers StrategiesDocument19 pagesMarket Challengers Strategiestobbob007100% (20)

- 3S Why SandhyavandanDocument49 pages3S Why SandhyavandanvivektonapiNo ratings yet

- Haldex Valve Catalog: Quality Parts For Vehicles at Any Life StageDocument108 pagesHaldex Valve Catalog: Quality Parts For Vehicles at Any Life Stagehoussem houssemNo ratings yet

- Scale Aircraft Modelling 01.2019Document100 pagesScale Aircraft Modelling 01.2019Nikko LimuaNo ratings yet

- Subsea Pipeline Job DescriptionDocument2 pagesSubsea Pipeline Job DescriptionVijay_DamamNo ratings yet

- Helical Coil FlowDocument4 pagesHelical Coil FlowAshish VermaNo ratings yet

- Easy NoFap EbookDocument37 pagesEasy NoFap Ebookசரஸ்வதி சுவாமிநாதன்No ratings yet

- The Impact of Social Networking Sites To The Academic Performance of The College Students of Lyceum of The Philippines - LagunaDocument15 pagesThe Impact of Social Networking Sites To The Academic Performance of The College Students of Lyceum of The Philippines - LagunaAasvogel Felodese Carnivora64% (14)

- Machine DesignDocument627 pagesMachine DesignlucarNo ratings yet

- A Control Method For Power-Assist Devices Using A BLDC Motor For Manual WheelchairsDocument7 pagesA Control Method For Power-Assist Devices Using A BLDC Motor For Manual WheelchairsAhmed ShoeebNo ratings yet

- GENUS Clock Gating Timing CheckDocument17 pagesGENUS Clock Gating Timing Checkwasimhassan100% (1)

- SLHT Grade 7 CSS Week 5 Without Answer KeyDocument6 pagesSLHT Grade 7 CSS Week 5 Without Answer KeyprinceyahweNo ratings yet

- The Incidence of COVID-19 Along The ThaiCambodian Border Using Geographic Information System (GIS), Sa Kaeo Province, Thailand PDFDocument5 pagesThe Incidence of COVID-19 Along The ThaiCambodian Border Using Geographic Information System (GIS), Sa Kaeo Province, Thailand PDFInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Cross System Create Supplier ProcessDocument14 pagesCross System Create Supplier ProcesssakthiroboticNo ratings yet

- Module 1Document64 pagesModule 1Jackyson RajkumarNo ratings yet

- Grammar Review A2-B1Document5 pagesGrammar Review A2-B1Lena Silva SouzaNo ratings yet

- CE Laws L8 L15Document470 pagesCE Laws L8 L15Edwin BernatNo ratings yet

- Drill Bit Classifier 2004 PDFDocument15 pagesDrill Bit Classifier 2004 PDFgustavoemir0% (2)

- 88 Year Old Man Missing in SC - Please ShareDocument1 page88 Year Old Man Missing in SC - Please ShareAmy WoodNo ratings yet

- 2 Beats Per Measure 3 Beats Per Measure 4 Beats Per MeasureDocument24 pages2 Beats Per Measure 3 Beats Per Measure 4 Beats Per MeasureArockiya StephenrajNo ratings yet

- BF254 BF255Document3 pagesBF254 BF255rrr2013No ratings yet

- Complex Poly (Lactic Acid) - Based - 1Document20 pagesComplex Poly (Lactic Acid) - Based - 1Irina PaslaruNo ratings yet

- Light Dimmer CircuitsDocument14 pagesLight Dimmer CircuitskapilasriNo ratings yet

- Job Sheet 1Document5 pagesJob Sheet 1Sue AzizNo ratings yet