You might also like

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Finance of International Trade Related Treasury OperationsDocument1 pageFinance of International Trade Related Treasury OperationsMuhammad KamranNo ratings yet

- Detailed Lesson Plan in ABMDocument5 pagesDetailed Lesson Plan in ABMAnonymous QZsOxQsJNo ratings yet

- FIN036 AssignmentDocument25 pagesFIN036 AssignmentSandeep BholahNo ratings yet

- Mande Morisho What Do You Know About Depository InstitutionsDocument2 pagesMande Morisho What Do You Know About Depository InstitutionsMand'e MorishoNo ratings yet

- Objectives of AuditDocument4 pagesObjectives of AuditSana ShafiqNo ratings yet

- Sample Agreement To Deliver BitcoinsDocument2 pagesSample Agreement To Deliver BitcoinsMike Caldwell100% (1)

- Application AmexDocument8 pagesApplication AmexAkash HimuNo ratings yet

- Evaluation of BC ModelDocument46 pagesEvaluation of BC ModelPiyuksha PargalNo ratings yet

- Kfs Current AccountsDocument10 pagesKfs Current Accountsritika sainiNo ratings yet

- Industry Profile: Banking Sector in IndiaDocument15 pagesIndustry Profile: Banking Sector in Indiasri1031No ratings yet

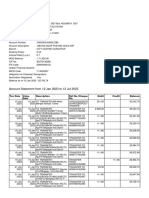

- Account Statement From 12 Jan 2023 To 12 Jul 2023Document10 pagesAccount Statement From 12 Jan 2023 To 12 Jul 2023SouravDeyNo ratings yet

- Lecture PPTs Business Communication Unit IIIDocument34 pagesLecture PPTs Business Communication Unit IIIAmit Kumar100% (1)

- General Vs BarramedaDocument11 pagesGeneral Vs BarramedaShivaNo ratings yet

- Sa 510Document14 pagesSa 510Narasimha Akash100% (1)

- Current Issues in Istisna & Tijarah (Final)Document12 pagesCurrent Issues in Istisna & Tijarah (Final)Hasan Irfan Siddiqui100% (1)

- Customer Perception Towards Internet Banking PDFDocument17 pagesCustomer Perception Towards Internet Banking PDFarpita waruleNo ratings yet

- Credit Risk - Standardised ApproachDocument78 pagesCredit Risk - Standardised Approachleyla_lit100% (2)

- Local Case: MGT - 489 Sec: 07 Submitted To S.S.M Sadrul Huda (SSH2) Associate Professor Dept. of ManagementDocument7 pagesLocal Case: MGT - 489 Sec: 07 Submitted To S.S.M Sadrul Huda (SSH2) Associate Professor Dept. of ManagementThe TopTeN CircleNo ratings yet

- MFL 16 17 Ar PDFDocument120 pagesMFL 16 17 Ar PDFSatvinder Deep SinghNo ratings yet

- Marketing Strategy of Bharti Axa Life Insurance - 191468884Document36 pagesMarketing Strategy of Bharti Axa Life Insurance - 191468884Jammu & kashmir story catcherNo ratings yet

- Abc Company Trial Balance For The Year End: December 31, 2010Document8 pagesAbc Company Trial Balance For The Year End: December 31, 2010JT GalNo ratings yet

- What Is Credit AppraisalDocument8 pagesWhat Is Credit AppraisalAshwin Sajan VargheseNo ratings yet

- RBI SBI Demand Draft Exchange RatesDocument11 pagesRBI SBI Demand Draft Exchange RatesJithin VijayanNo ratings yet

- Basic Banking TransactionDocument30 pagesBasic Banking TransactionJennifer Dela Rosa100% (1)

- AICPA - Develops Standards For Audits ofDocument3 pagesAICPA - Develops Standards For Audits ofAngela PaduaNo ratings yet

- Semester: B. Com - V Semester Name of The Subject: Financial Market & Institutions Unit-1Document61 pagesSemester: B. Com - V Semester Name of The Subject: Financial Market & Institutions Unit-1Sparsh JainNo ratings yet

- IIF ReportDocument152 pagesIIF ReportJuan Manuel Lopez LeonNo ratings yet

- Tcs Project ReportDocument52 pagesTcs Project Reportfaheem munim0% (2)

- Doctrine of TracingDocument34 pagesDoctrine of TracingAkmal SafwanNo ratings yet

- Apni Shakhsiyat Ki Tameer Kaise Ki JaeDocument99 pagesApni Shakhsiyat Ki Tameer Kaise Ki JaeMansoorNo ratings yet