You might also like

- Intermediate Accounting 2: a QuickStudy Digital Reference GuideFrom EverandIntermediate Accounting 2: a QuickStudy Digital Reference GuideNo ratings yet

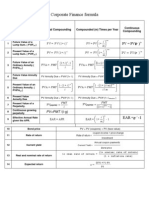

- Kelly's Finance Cheat Sheet V6Document2 pagesKelly's Finance Cheat Sheet V6Kelly Koh100% (4)

- Corporate Finance Formulas: A Simple IntroductionFrom EverandCorporate Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- BF2201 Cheat Sheet FinalsDocument2 pagesBF2201 Cheat Sheet Finalssiewhong93100% (1)

- Cheat SheetDocument3 pagesCheat SheetjakeNo ratings yet

- CorpFinance Cheat Sheet v2.2Document2 pagesCorpFinance Cheat Sheet v2.2subtle69100% (4)

- Cheat Sheet Final - FMVDocument3 pagesCheat Sheet Final - FMVhanifakih100% (2)

- Accounting and Finance Formulas: A Simple IntroductionFrom EverandAccounting and Finance Formulas: A Simple IntroductionRating: 4 out of 5 stars4/5 (8)

- Corporate Finance - FormulasDocument3 pagesCorporate Finance - FormulasAbhijit Pandit100% (1)

- CheatSheet (Finance)Document1 pageCheatSheet (Finance)Guan Yu Lim100% (3)

- CheatDocument1 pageCheatIshmo KueedNo ratings yet

- Cheat Sheet Exam 1Document1 pageCheat Sheet Exam 1Shashi Gavini Keil100% (2)

- How to Read a Financial Report: Wringing Vital Signs Out of the NumbersFrom EverandHow to Read a Financial Report: Wringing Vital Signs Out of the NumbersNo ratings yet

- Corporate Finance Formula SheetDocument4 pagesCorporate Finance Formula Sheetogsunny100% (3)

- Corporate Finance Math SheetDocument19 pagesCorporate Finance Math Sheetmweaveruga100% (3)

- ACC1002X Cheat Sheet 2Document1 pageACC1002X Cheat Sheet 2jieboNo ratings yet

- Accounting Cheat SheetsDocument4 pagesAccounting Cheat SheetsGreg BealNo ratings yet

- Financial Accounting: Tools For Business Decision-Making, Third Canadian EditionDocument6 pagesFinancial Accounting: Tools For Business Decision-Making, Third Canadian Editionapi-19743565100% (1)

- Corporate Finance FormulasDocument3 pagesCorporate Finance FormulasMustafa Yavuzcan83% (12)

- Economics Cheat SheetDocument2 pagesEconomics Cheat Sheetalysoccer449100% (2)

- Dividend Discount and Residual Income Models ExplainedDocument2 pagesDividend Discount and Residual Income Models ExplainedMohammad DaulehNo ratings yet

- Cheat Sheet Corporate - FinanceDocument2 pagesCheat Sheet Corporate - FinanceAnna BudaevaNo ratings yet

- Cheat Sheet For AccountingDocument4 pagesCheat Sheet For AccountingshihuiNo ratings yet

- Cheat Sheet For Financial AccountingDocument1 pageCheat Sheet For Financial Accountingmikewu101No ratings yet

- Cfa Level I - Us Gaap Vs IfrsDocument4 pagesCfa Level I - Us Gaap Vs IfrsSanjay RathiNo ratings yet

- Managerial Accounting Mid-Term Cheat SheetDocument6 pagesManagerial Accounting Mid-Term Cheat SheetĐạt Nguyễn100% (1)

- CFA Level 1 Corporate Finance - Our Cheat Sheet - 300hoursDocument14 pagesCFA Level 1 Corporate Finance - Our Cheat Sheet - 300hoursMichNo ratings yet

- FIN6215-Cheat Sheet BigDocument3 pagesFIN6215-Cheat Sheet BigJojo Kittiya100% (1)

- Finance Cheat SheetDocument4 pagesFinance Cheat SheetRudolf Jansen van RensburgNo ratings yet

- Bonds Exam Cheat SheetDocument2 pagesBonds Exam Cheat SheetSergi Iglesias CostaNo ratings yet

- Accounting Cheat SheetDocument7 pagesAccounting Cheat Sheetopty100% (15)

- Accounting Cheat SheetDocument2 pagesAccounting Cheat SheetvgirotraNo ratings yet

- ACCT 101 Cheat SheetDocument1 pageACCT 101 Cheat SheetAndrea NingNo ratings yet

- Fin Cheat SheetDocument3 pagesFin Cheat SheetChristina RomanoNo ratings yet

- Accounting Cheat SheetDocument2 pagesAccounting Cheat Sheetanoushes1100% (2)

- Ultimate Accounting Guide SheetDocument1 pageUltimate Accounting Guide SheetMD. Monzurul Karim Shanchay67% (6)

- CFA Formula Cheat SheetDocument9 pagesCFA Formula Cheat SheetChingWa ChanNo ratings yet

- Time value of money cheat sheetDocument3 pagesTime value of money cheat sheetTechbotix AppsNo ratings yet

- The Ultimate Financial Management Cheat SheetDocument3 pagesThe Ultimate Financial Management Cheat SheethazimNo ratings yet

- Bec Notes 17Document87 pagesBec Notes 17Pugazh enthi100% (2)

- Business Valuation Methods and Uses GuideDocument43 pagesBusiness Valuation Methods and Uses GuideAngus Sadpet100% (1)

- Corporate Finance Practice ExamDocument22 pagesCorporate Finance Practice ExamgNo ratings yet

- 8th and Walton Retail Math Cheat SheetDocument1 page8th and Walton Retail Math Cheat SheetSurabhi RajeyNo ratings yet

- Fin 3101Document5 pagesFin 3101Park JiyeonNo ratings yet

- Cost of Capital and Capital Budgeting FormulasDocument4 pagesCost of Capital and Capital Budgeting FormulasMaha Bianca Charisma CastroNo ratings yet

- Cost of Capital: A Concise GuideDocument23 pagesCost of Capital: A Concise GuidenawabrpNo ratings yet

- R M R M R M R M: Time Value of MoneyDocument8 pagesR M R M R M R M: Time Value of MoneyHenry JiangNo ratings yet

- Cheat SheetDocument1 pageCheat Sheetakdhkjh100% (1)

- Formula SheetDocument7 pagesFormula SheetanasfinkileNo ratings yet

- The Cost of CapitalDocument4 pagesThe Cost of CapitalCharice CortesNo ratings yet

- Session 6 – Pricing of Risk and Capital Budgeting RulesDocument4 pagesSession 6 – Pricing of Risk and Capital Budgeting RulesZaki KamardinNo ratings yet

- 12 & 13. Cost of CapitalDocument5 pages12 & 13. Cost of CapitalSatyam RahateNo ratings yet

- 1Document21 pages1DrGeorge Saad AbdallaNo ratings yet

- Lecture Slides - Course Basics, Housekeeping & IntroductionDocument18 pagesLecture Slides - Course Basics, Housekeeping & IntroductionAvishai MoscovichNo ratings yet

- Valuation of Shares & Bonds Lecture NotesDocument8 pagesValuation of Shares & Bonds Lecture NotesNiket R. ShahNo ratings yet

- Twentieth AR IIFL 20150703Document164 pagesTwentieth AR IIFL 20150703Sri ReddyNo ratings yet

- A9r68c4valuation Project WorkbookDocument144 pagesA9r68c4valuation Project WorkbookjomanousNo ratings yet

- Topic 6 Financial AssetsDocument60 pagesTopic 6 Financial AssetsRui JiaNo ratings yet

- Introduction To CooperativesDocument35 pagesIntroduction To Cooperativesxformal100% (1)

- Bank Financing Proposal for Brick Factory ExpansionDocument11 pagesBank Financing Proposal for Brick Factory ExpansionSudhakaar ShakyaNo ratings yet

- Accounting CH 9Document38 pagesAccounting CH 9Nguyen Dac ThichNo ratings yet

- Mutual Fund About SMCDocument61 pagesMutual Fund About SMCshaileshNo ratings yet

- Chapter 11Document10 pagesChapter 11HusainiBachtiarNo ratings yet

- Institute of Actuaries of India: Subject ST6 - Finance and Investment BDocument7 pagesInstitute of Actuaries of India: Subject ST6 - Finance and Investment BVignesh SrinivasanNo ratings yet

- Birla Sun Life InsuranceDocument17 pagesBirla Sun Life InsuranceKenen BhandhaviNo ratings yet

- BDA and Development Bank of Japan Form Strategic PartnershipDocument3 pagesBDA and Development Bank of Japan Form Strategic PartnershipPR.comNo ratings yet

- GG 16-18Document3 pagesGG 16-18Katlene HortilanoNo ratings yet

- List of BooksDocument4 pagesList of Booksavinash singhNo ratings yet

- 4Document24 pages4yyy yiyyao100% (1)

- Company Accounts Issue of Shares Par Premium DiscountDocument20 pagesCompany Accounts Issue of Shares Par Premium DiscountDilwar Hussain100% (1)

- Ipo Readiness 2014Document4 pagesIpo Readiness 2014Lahoty Arpit ArunkumarNo ratings yet

- Paul WilmottDocument3 pagesPaul Wilmottkylie05No ratings yet

- Tax Equity Financing and Asset RotationDocument38 pagesTax Equity Financing and Asset RotationShofiul HasanNo ratings yet

- Estimating Beta For Barclays Bank Shares Listed On The Zimbabwe Stock Exchange (ZSE) For The Year 2014Document8 pagesEstimating Beta For Barclays Bank Shares Listed On The Zimbabwe Stock Exchange (ZSE) For The Year 2014IOSRjournalNo ratings yet

- Analysis of Benefits and Risks of Mutual FundsDocument24 pagesAnalysis of Benefits and Risks of Mutual Fundspratik0909No ratings yet

- Securities Market (Basic) Module PDFDocument284 pagesSecurities Market (Basic) Module PDFAyush Pratap SinghNo ratings yet

- Investment Risk Quiz: Assess Your ToleranceDocument3 pagesInvestment Risk Quiz: Assess Your ToleranceAnkit GoelNo ratings yet

- Financial Performance Analysis of Top Ethiopian Private BanksDocument55 pagesFinancial Performance Analysis of Top Ethiopian Private BanksAnonymous ej7PpdNo ratings yet

- Review Test Submission - Lecture 6 - Online Assignment - ..Document6 pagesReview Test Submission - Lecture 6 - Online Assignment - ..RishabhNo ratings yet

- 3Document26 pages3JDNo ratings yet

- Index Models and Portfolio OptimizationDocument14 pagesIndex Models and Portfolio OptimizationdomazzzNo ratings yet

- Revised Syllabus for TY BCom Business EconomicsDocument5 pagesRevised Syllabus for TY BCom Business EconomicsDarshit V VoraNo ratings yet