You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- BC AssignmentDocument19 pagesBC AssignmentSrinath SaravananNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Review of The Nigeria National Houisng PolicyDocument8 pagesReview of The Nigeria National Houisng PolicyLouis Vincent100% (1)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Final Project With FindingsDocument51 pagesFinal Project With FindingsDivya PatelNo ratings yet

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (895)

- 10 PDFDocument7 pages10 PDFShubh GuptaNo ratings yet

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (400)

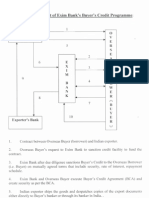

- Procedural Flow Chart of Exim BankDocument3 pagesProcedural Flow Chart of Exim BankMilan DasNo ratings yet

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Non Marketable Financial AssetsDocument3 pagesNon Marketable Financial AssetsSnehal JoshiNo ratings yet

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Cash Flows From Operating ActivitiesDocument5 pagesCash Flows From Operating ActivitiesIrfan MansoorNo ratings yet

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Ey Building A Strategic and Profitable Auto Finance Portfolio in IndiaDocument28 pagesEy Building A Strategic and Profitable Auto Finance Portfolio in IndiaDominic SavioNo ratings yet

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (588)

- Tugas 1 - Bahasa Inggris Tata NiagaDocument2 pagesTugas 1 - Bahasa Inggris Tata NiagaNabilaNo ratings yet

- Analyzing and Investing in Community Bank StocksDocument234 pagesAnalyzing and Investing in Community Bank StocksRalphVandenAbbeele100% (1)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- Docket - 6062 - Document - 1Document67 pagesDocket - 6062 - Document - 1Troy UhlmanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- 01 Intro To ServicesDocument59 pages01 Intro To ServicesOmkar ParshuramNo ratings yet

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Yield Pledge Checking: Account Opening & UsageDocument2 pagesYield Pledge Checking: Account Opening & Usageshenzo_No ratings yet

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- ONE IBC LIMITED - Bank Wire Payment Instructions USD + EUR Updated 26 Dec 2018Document4 pagesONE IBC LIMITED - Bank Wire Payment Instructions USD + EUR Updated 26 Dec 2018dothanhtungNo ratings yet

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Insight 021210 LowresDocument132 pagesInsight 021210 LowresAbu LuhayyahNo ratings yet

- Artikel Ilmiah PDFDocument15 pagesArtikel Ilmiah PDFelseNo ratings yet

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Industrial Visit (Final) PDFDocument25 pagesIndustrial Visit (Final) PDFrohit jaiswalNo ratings yet

- 6 Month Transaction BankDocument15 pages6 Month Transaction BankShravan KumarNo ratings yet

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- 02 Time Value of MoneyDocument50 pages02 Time Value of MoneyFauziah Husin HaizufNo ratings yet

- Digitizing Rural Value Chains in India Intellecap ReportDocument58 pagesDigitizing Rural Value Chains in India Intellecap ReportUmang AgarwalNo ratings yet

- ESP2 - Unit 8 Central Banking - KEYDocument7 pagesESP2 - Unit 8 Central Banking - KEYVeo Veo ChanNo ratings yet

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Mortgage DeedDocument3 pagesMortgage Deedphoebekapoor5037No ratings yet

- Final ProposalDocument6 pagesFinal ProposalSanam_Sam_273780% (10)

- A Project Report On Employee MotivationDocument72 pagesA Project Report On Employee MotivationNoor Ahmed64% (25)

- Job Analysis NIB BankDocument15 pagesJob Analysis NIB BankKiran ReshiNo ratings yet

- Working CapitalDocument72 pagesWorking CapitalSyaapeNo ratings yet

- Fiqh For Economist 2: Name: Nor Farhain Binti Sarmin MATRIC NO: 1229128Document12 pagesFiqh For Economist 2: Name: Nor Farhain Binti Sarmin MATRIC NO: 1229128Farhain SarminNo ratings yet

- Ielts Refund and Transfer Policy-2Document1 pageIelts Refund and Transfer Policy-2Reader RaiderNo ratings yet

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (121)

- People Soft Bundle Release Note 9 Bundle21Document21 pagesPeople Soft Bundle Release Note 9 Bundle21rajiv_xguysNo ratings yet

- LockBox Doc For TrainingDocument15 pagesLockBox Doc For Trainingankish77100% (1)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)