Professional Documents

Culture Documents

Almost Final

Uploaded by

Butesh R E DarshanOriginal Description:

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Almost Final

Uploaded by

Butesh R E DarshanCopyright:

Available Formats

CASH MANAGEMENT IN WORKING CAPITAL

EXECUTIVE SUMMERY Introduction A basic limitation of the traditional financial statements comprising the balance sheet and the profit and loss A/c is that they do not give all the information related to the financial operations of the firm. Nevertheless, they provide some extremely useful information to the extent that the balance sheet mirrors the financial position on a particular date in terms of the structure of assets, liabilities and owners equity, and so on and the profit and loss account shows the results of operations during the certain period of time in terms of the revenues obtained and the cost incurred during the year. Thus, the financial statements provide summarized view of the financial position and operations of the firm. Therefore, much can be learnt about a firm from a careful examination of its financial statements as invaluable documents! Performance reports. The analysis of financial statement is, thus, an important aid to financial analysis.

The focus of financial analysis is on key figures in the financial statements and the significant relationship that exists between them. The analysis of financial statements is a process of evaluating the relationship between components parts of financial statements to a better understanding of the firms position and performance. The first task of the financial analyst is to select the information relevant to the decision under consideration from the total information contained in the financial statements. The second

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

step is interpretation and drawing of interference and conclusions. In brief, financial analysis is the process of selection, relation and evaluation.

Statement of the problem Financial statements can provide valuable insights into a firms performance. Analysis of financial statements is useful for the company to evaluate its own performance and also it is of interest to lenders (short term as well as long term), inventors, security analysts, managers and others. Financial statement analysis may be done for a variety of purposes, which may range from a simple analysis of the short term liquidity position of the firm to a comprehensive assessment of the strengths and weaknesses of the firm in various areas. It is helpful in assessing corporate excellence, judging creditworthiness, forecasting bond ratings, predicting bankruptcy, and assessing market risk.

To evaluate the effectiveness of operations and to determine it success an analyst has to combine quantitative results with qualitative factors. For instance a companys current profitability may be low. However, because of actions initiated by the management like technology up gradation, joint venture, joint

2

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

venture, and collaboration with a foreign partner, etc., the prospects for better performance of the company in future may be bright.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

Aims and Objectives Objectives of the study To gain corporate exposure

To get exposed to all the departments of the company

To know the financial position of the firm access

To assess the financial strengths and weakness of the firm to give valuable suggestion to attain operational excellence

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

Scope of the study This project as a reference guide or as a source of information. It gives the idea about the financial analysis of the firm. The main objective of the study was to put into practical the theoretical aspect of the study into real life work experience. The study aims to study the liquidity position of the firm. Ratio analysis has been used to analyze the financial position of a firm. It deals with analysis and interpretation of data collected through the sources of primary and secondary data. Graphs diagrams and tabulation methods are used to analyze and interpret the data collected. Methodology The data in this project is enabling in secondary in nature. Financial reports, company records, were referred for data analysis. The study has been undertaken by collecting relevant data from the balance sheets, profit and loss statements, operating statements of the company and financial tools were used in analyzing and interpretation of data. However, primary data is also collected by observation, discussing with company officials. This primary data is used to fill in the gaps while preparing this report, and to know the latest procedures adopted by the company. This helped me to draw inferences and conclusions.

METHODOLOGY OF DATA COLLECTION

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

Research methodology Research methodology is a systematic way for solving any research problem. It is a science of analyzing how research is done scientifically. It studies the various steps that are generally adopted by a researcher in studying the research problem.

Sources of Data There are two type of data Primary data Secondary data Primary data The primary data are those, which are, collected a fresh for the first time and thus happen to be original in character. The primary data collection involves the collecting of information for the first time by observation, experimentation and through questionnaire in the original form by the researching himself or his nominees. Such data are published by authorities who themselves are responsible for their collection. Secondary data The secondary data are those which have been collected by some other and which have been processed. Generally speaking secondary data are information, which have been previously collected by some organization to satisfy its own need. But the department under reference for an entirely different reason is using it.

7

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

There are two main sources for secondary data. Published data Data that is already available in books, magazines, trade journals, newspapers, reports, prepared by research scholar etc. Unpublished data This is not published, it can be found in unpublished biographies, autobiographies, some governmental aspects, and private individual organization etc.

Limitations of the study The span of study is confined to only 3 years. The

comparison of various ratios may not have the same conditions, which may result in unrelated comparisons. The other limiting factor being the confidential in nature of

certain aspects. The study was conducted to the extent of information provided. Time constraint : It is not possible to study in detail the

finance operation of the company.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

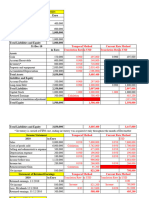

FINDINGS SHARE CAPITAL The authorized share capital of the company is Rs. 100,00,000 divided into 100000 equity shares of Rs. 100 each VEIW OF FINANCIAL POSITION Though the company is incorporated in the year of 2000 its actual commercial work stated in the year of 2003 April 1st The company had not started any business, so there is no question of profit in the year 2000 to 31st March 2003. But however as a first step towards the commencement of commercial activity the company has taken over the business of timing gear blanker on April 2003 2003-04 this year the company has started commercial activity by acquiring the building, plant & machinery from Divgi Metal ware Pvt. Ltd. , on an annual lease of Rs 9,00,000/- plus taxes Rs 51,750/-. Using these leased assets the company has carried out job work for Divgi Warner Pvt. Ltd. After expenses the company made a modest profit of Rs 3745/- before depreciation. But the depreciation was Rs 1,09,604/- ,so less in that year was Rs 1,05,858/-.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

10

CASH MANAGEMENT IN WORKING CAPITAL

With the automobile sector looking up DIPL have all confidence that in the coming years the company will turn the corner.

2004-05 in this year as made aprofit before depreciation Rs. 3, 36, 064/- so it result as follows Financial Results Year Ended Particulrs 31-3-2005 Rs. .. Profit/(Loss) Before Depreciation Less: Depreciation Profit/(Loss) for the year 3, 36, 064 1, 75, 159 .. 1, 60, 905

11

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

Brought Forward Profit/(Loss) Balance Carried to Balance Sheet

1, 12, 393 .. 48, 512 ..

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

12

CASH MANAGEMENT IN WORKING CAPITAL

Recommended Capabilities for Cash-Flow Tools A good cash-flow management system should be easy to use, offer flexible "what-if" and reporting options, and allow you to update projections once actual results are available. The importance of ease of use depends on how frequently you need to use your cash-flow management system. Many businesses will calculate and update their cash-flow projections monthly. A few small or cash-flush businesses may only need to look at it once a quarter. Larger companies, or ones walking a financial tightrope, may manage their cash daily. If you need to use your cash-flow tool often, you will learn its ins and outs and capabilities over time and become expert in its use. If you use the tool only occasionally, then it's very important that it be easy to use effectively, because you don't want to have to relearn a complex tool each quarter. The need for "what-if" scenarios is important for businesses that do not have easily predictable financial results due to the nature of their work. For example, cash flow may be highly dependent upon the timing of the signing of a large contract that provides an up-front payment. You would want to project cash flow scenarios both with and without the contract, to see your options. Since managing cash flow is a never-ending task, you'll usually want some way of easily updating your cash-flow

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

13

CASH MANAGEMENT IN WORKING CAPITAL

projections from the last period to include this period's actual results as a basis for moving forward. A cash-flow tool that's integrated into your business accounting system will usually have this capability. Otherwise, look for a way to easily export your actual numbers from your accounting package and then import them into your cash-flow tool.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

14

CASH MANAGEMENT IN WORKING CAPITAL

Conclusion Each company struggles in the initial stage. But it recovers slowly. It does not happen suddenly itself. It takes time. While Divgi Industries Pvt. Ltd.(DIPL) is a developing company. It has bright future, because there is a wide scope for automobiles in the whole world. So there is no chance of decrease in demand for automobiles components and innovation in the area. DIPL is working at their best level. According to me company is utilizing local facilities effectively but company is not utilizing its plant & machinery and land & building fully. The workers, staff, and management people are conscious about their work and putting their full effort to see DIPL as a developed company. WHEN A PERSON IS CONSCIOUS AND SINCERE ABOUT HIS WORK HE WILL ACHIEVE THE GOAL.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

15

CASH MANAGEMENT IN WORKING CAPITAL

Introduction In 1997, the government has published the Mechanical industry Development Plan for the period 2000-2010 composed by Industrial Strategy and Policy Research Institute of Ministry of Industry. The Development Plan also provided guide line for the development of auto industry, both assembling and producing parts and components. Ever since, many policies to promote the development of mechanical industry in general and auto industry in particular has been promulgated. Priorities which auto parts and components producers may be entitled to includes The Daimio policy initiated in 1986 has given a extra development momentum for the whole economy in general and auto industry in particular. Fourteen foreign investors have been granted investment license in car assembling and manufacturing and about twice as much investment licenses have been granted to foreign auto component and spare parts investors. However, due to various hindrances, there are only 11 auto foreign-invested manufacturers currently working and a dozen component and spare parts foreign-invested manufacturers actually back up for auto industry (several other investors just provide components and spare parts for motorbike manufacturing thought they registered to produce components and spare parts for auto manufacturing), coexisting with the previously available domestic auto spare parts producers. These companies construct the backbone of Vietnam auto industry.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

16

CASH MANAGEMENT IN WORKING CAPITAL

As for foreign invested auto component and spare parts producers, most the projects are small scaled in relation with auto industry. These projects often assemble imported materials and export most of their products for auto manufactures in the region and only a small portion is for domestic consumption.

Demand for products is derived from two sources: components and spare parts for repair and maintenance of currently running vehicles and for production of auto manufactures (domestic and abroad). However, a considerable proportion of the operational vehicles has been in use for quite along time and is in need of overhaul or even replacement. Component and spare parts demand can be inferred from this pool. Auto manufacturers employ brand-new components and spare parts for their production and after-sale services. Only those satisfy the produces technical requirements and financially reasonable producers. For the purpose of assembling brand-new auto, complete sets of auto parts and components are imported. Local finish is just assembling, welding and painting. As mentioned above, such complete sets are imported from abroad factories of the suppliers. For example, complete set of auto parts for the assemble of

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

are

employed,

especially

for

foreign-invested

17

CASH MANAGEMENT IN WORKING CAPITAL

TOYOTA are imported from other factories of TOYOTA in Japan, Indonesia, Australia, etc. The annual volume of import is based on the operation capacity of the investors and annual overall plan for import is approved by the Prime Minister. Parts and components for maintenance, repair and after sale services of such producers are also imported. These items are often distributed through authorized dealers network of the producers. Customers are mainly wealthy owners of brand-new auto who want origin parts and components of the maker to be sure that such replacements are compatible and meet the producer standards. Demand for parts and components for repair and

maintenance of currently operating vehicle is diversified. The restriction on import of secondhand auto parts and components whereas domestic production is still infant results in the fact that available separate parts and components for substitution in the market are second-hand ones which were knocked downed from other auto or smuggled.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

18

CASH MANAGEMENT IN WORKING CAPITAL

The volume of brand-new imported separate parts is inconsiderable. For most of auto currently in use in Vietnam are from CIS, South Korea and Japan, the separate auto parts and components are also originated from these countries. Whenever there is something breakdown, the owner may find second-hand substitution in open air markets or mechanical workshops, both private and State owned. Domestic auto parts and components producers are mainly State owned mechanical and chemical enterprises. These enterprises were established during the 60s and 70s with the assistance of East Europe socialist countries and China. The technology and machinery were also equipped ever since. As mentioned above, these enterprises produced some 25 type of external2 parts and components for autos made in socialist countries. No main parts of the engine or body-works were produced in large scale. Products followed socialist vehicle norms and standards therefore may mot compatible with auto made in other countries such as Japan, West Germany, USA, etc. The renovation of outdated machinery is not comprehensive and continually for lack of fund. Replaced machinery originated from difference sources and are not synchronous. This results in the inferior quality of products produced by these producers consequently. The constrain on the ability of providing qualified products for auto parts and components markets forces domestic mechanical

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

19

CASH MANAGEMENT IN WORKING CAPITAL

to diversify their products. Though this solution allows them to maintain their operation but confused orientations drift them off specialization and producing qualified auto parts and components

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

20

CASH MANAGEMENT IN WORKING CAPITAL

Company profile DIVGI INDUSTRIES PVT.LTD. is situated at the out skirts of the city SIRSI in Banavasi road. It is a medium scale engineering industry of prestigious city SIRSI. It is a place which is situated at the top of western ghats and is one of the famous city in North Canara. DIVGI INDUSTRIES PVT.LTD. (DIPL) is incorporated in the year of 2000.its actual commercial activities stared in April 2003. its registered office is in Sirsi (KARNATAK). It produces the finished and semi finished components of automobiles. It is certified with ISO/TS 16949 quality system in 2005 There is another one industry is situated in the same area DIVGI WARNERS PVT.LTD(DWPL) for which DIPL does the job work. Actually buildings and machineries are taken on lease basis from DIVGI METALWARES PVT.LTD. DIPL is produces automobile components likes companion flange, sun gear, shaft, yoke, etc Raw materials are comes from Divgi warners pvt. ltd.(Puna) to Divgi warners pvt. ltd.(Sirsi) Again these raw materials supplied DIPL from Divgi warners pvt.ltd.(Sirsi).After the job work on DIPLagain supplied to DWPL(Sirsi) after some value addition work these products are send to DWPL(Puna) for export

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

21

CASH MANAGEMENT IN WORKING CAPITAL

(USA) and other customers like Mahindra & Mahindra, Telco, Tata ,etc There are 120 employees working in DIPL. The workers have shift basis work with specified target. The company is paying them a good salary and provide good facilities and motivational programs. DIPL is a developing company and has turnover near crore . DIPL doing a job work for DWPL but this year company is fetching new customer.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

22

CASH MANAGEMENT IN WORKING CAPITAL

VISION : To be catalytic and innovative organization in the society that supplies goods and services that are of superior value to those who use them; create jobs that provide meaning for those who do them , and offers our talents and wealth to help and reward all who invest in us their time money and trust GOALS : To become Indias prominent and perfect technology and in crate based solution provide in automotive transmission and power train application for on and off highway usage to achieve world class standard in spheres of our business activities. MISSION : Our mission is to assist our customer seek new frontiers of value for the continuously evolving needs of a globalizing market place in so doing ,we seek to bring unique distinctive and superior value to those who use our products and services .We seek to provide our customers a continuous sources of innovation by anticipating change and shaping it to our purpose.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

23

CASH MANAGEMENT IN WORKING CAPITAL

THE OBJECTIVES OF THE COMPANY: To manufacture, process, treat, buy sell import and export. Exchange after improve manipulate report prepare for market or otherwise deal in all kinds of automobile engineering components including their costing, by products joint there of and for the purpose do all the necessary process including machining champhering cutting, grinding, boaring, moving, as well as smelting, founding, melting, sintering, defining, making chaping shealing threating welding fabricating, extracting, foiling and finishing of the casting including any part derived as by product out of any of the above process in to finish component required for engineering industry in general and automobile industry in particular. To carry on the business of engineer contractors builders filters founders wire drawers galunisers enamollers electro platers. To own run manage and carry on the business of workshop or structure mechanical, ferrous, foundry, storage tanks, chimneys pressure vessels, fabricated items agriculture implements cycle parts pipes and fittings. To carry on the business as technic advisors, consultants for any other person or person inturned in or carrying or any of

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

24

CASH MANAGEMENT IN WORKING CAPITAL

the business, as similar to or connected with the objects of the company for such consideration and on such terms and condition beneficial to the company.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

25

CASH MANAGEMENT IN WORKING CAPITAL

Board of directors Balachandra Narasighrao Divgi Puna Umesh Narasighrao Divgi Sirsi Jitendra Bhasker Divgi Sirsi Meera Ramrao Divgi Sirsi

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

26

CASH MANAGEMENT IN WORKING CAPITAL

ORGANIZATION CHART

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

27

CASH MANAGEMENT IN WORKING CAPITAL

COMPANY PRODUCTS Name range/weight 1 : YOKE Yoke Reg DC 1.5000 Kg Yoke Reg SC 1.5000 Kg Yoke Export DC Kg 2 : COMANION FLANGE 13-00-031-006-M Kg 44-00-031-009-B Kg 44-00-031-029-A Kg 44-00-031-030-A Kg 3 : SHAFT Lower output shaft (Reg) Kg

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

size

1.3000

1.0300 1.4500 1.6800 1.7500

0.8500

28

CASH MANAGEMENT IN WORKING CAPITAL

Lower output shaft (Exp) Kg Upper output shaft 2.8760 Kg 4 : SUNGEAR Sun gear Kg

0.8500

0.6740

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

29

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

30

CASH MANAGEMENT IN WORKING CAPITAL

COMPANY PROFILE WITH REFERANCE TO 7S MODEL OF McKINSEY Strategy The DIPL has a very systematic action .The organization is very systematic in all its operations. The allocation of resources are

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

31

CASH MANAGEMENT IN WORKING CAPITAL

effectively done. This strategy is followed to achieve the companys aims Structure The organization structure is a very formal one. The department is structure is done in such a manner that it helps in the smooth running of the organization. The authority and responsibility relationships are formally structured. System The system may be in the production department, HR department, finance ,management representative , customer representative departments are very well organized . good control techniques are used in all the departments. Style Style refers to the way of managing labours and spends its time to achieve the organizational goals. The leading functions in DIPL is done effectively so that organizational goals are achieved. Staff The staff refer to the people in the enterprise and their socialization into the organizational culture. The staff of DIPL have perfectly adjusted with the organizational culture. Shared value This value helps the members in the organization to achieve effective goals. It helps in creating a favorable organizational

32

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

culture by taking into consideration the goals of both the superiors and subordinates. Skills Skills in the 7S model refers to the distinctive capabilities of the organization. The DIPL is very effective in the achievement of quality systems. It is also been certified by International Organizational for Standardization. The organization doing extremely well in the domestic as well as international market.

The 7S McKinsey model

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

33

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

34

CASH MANAGEMENT IN WORKING CAPITAL

General requirement Defining the process for quality management system to apply across the company. Defining the sequence and interaction of these process. Ensure both sequence and control of these process. Providing resources and information to operation and monitoring of these process. Monitor measure and analyze these process. Implement and achieve the planned results . Achieve the continual improvement of the processes. Control the outsourced processes that affect the product conformity with the requirements by identifying with the quality management. The company takes the responsibilities of conformity to all customer requirement out sourced processes. Ensure the above requirements are achieved in a accordance with ISO/TS 16949. The results shall be reviewed as necessary or determine further opportunities for improvement. Audits, customer feedback and review of the quality management system can also be considered as continual activity. The company shall be on improving the system and its ability to provide conforming product/services consistently. Reference :

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

35

CASH MANAGEMENT IN WORKING CAPITAL

1. Procedure of control of quality records 2. Minutes of management review meeting 3. Procedure for corrective action 4. Procedure for preventive action 5. Procedure for internal audit 6. Procedure for control of non-conforming products

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

36

CASH MANAGEMENT IN WORKING CAPITAL

Management commitments The top management demonstrate leadership with respect to quality though management Communicating to organization the importance of meeting customer as well as statutory and regulatory requirements. Establishing the quality policy objectives and providing resources Conducting management reviews Review product realization processes and support processes to ensure their effectiveness and efficiency The directors/CEO is not only committed to the development of system but also to the improvement and its effectiveness Customer focus The process determining customer requirements is being covered by the following procedures: Customer related process Planning of product realization Customer satisfaction

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

37

CASH MANAGEMENT IN WORKING CAPITAL

The management is activity involved and ensures that these processes are actually working and the system is effective in promoting customer satisfaction through management review.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

38

CASH MANAGEMENT IN WORKING CAPITAL

Quality objectives

1. To continually enhance CUSTOMER SATISFECTION by

monitoring the CUSTOMER SATISFECTION INDEX 2. To improve PRODUCTIVITY achieve higher PROCESS CAPABILITIES with a focus to achieve ZERO DEFECT in all out business activities.

3. To achieve OPTIMUM INVENTORY LEVELS through ON

TIME PROCUMENT of quality materials at competitive prices.

4. To

improve

the

OVERALL

INVENTORY

EFFICTIVENESS.

5. To develop a motivated committed and effective team by

providing the necessary resources, good training programs and a congenial atmosphere for overall growth of the employees.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

39

CASH MANAGEMENT IN WORKING CAPITAL

QUALITY POLICY We at Divgi Industries Pvt. Limited are committed to pursue excellence, and enhance customer satisfaction through the process of continual improvement in all the spheres of our business activity.

We endeavor to achieve these goals through the development of standardized processes, measurable obj ect i ve s , a n d t h e si n c e r e and mot i va t e d involvement of all our people.

We

are

committed

to

creating

high

level

consciousness to defect prevention, reduction of data variation, and wastage minimization, in our continuous efforts to give our customer a complete defect and hassle-free experience.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

40

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

41

CASH MANAGEMENT IN WORKING CAPITAL

Continual improvement Continual improvement is part of our culture and way life of DIPL. It is a comprehensive and all compassing system of method and practice based on continual leaving to achieve sustain such maximize business success. It is driven by a close understanding of the customer, disciplined use of facts, data and analysis and deli gent attention to managing improving and investing where require our business process. To follow our vision to the future, we must see that differences between traditions that no longer serve us and have a courage to act on that knowledge we must be aiming the few who anticipate change and shape into our propose.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

42

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

43

CASH MANAGEMENT IN WORKING CAPITAL

CONTINUOUS IMPROVEMENT TARGET FOR - 2006 KEY PERFORMANCE INDICATOR SI No. 1 2 KPI MATERIAL YIELD IN HOUSE REJECTION TARGET 99.20% 0.040%

3 4

MANUFACTURING EFFECTIVENESS RIGHT FIRST TIME

82.00% 99.82%

UNSCHEDULED DOWN TIME

1.40%

OVERALL EQUIPMENT EFFECTIVENESS ON TIME DELIVERY

82.00%

100.00%

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

44

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

45

CASH MANAGEMENT IN WORKING CAPITAL

SAFETY RULES AND REGULATIONS: Safety is a very important factor that has to be considered at the shop floor. The workers working at the shop floor must take precautions for the purpose of the machines, material and themselves. If precautions are not observed by employees, the chance of accident will increase and this will result in the loss of machinery and the injury to workmen who may lead to disability or even death in measure cases. Hence, it is necessary to the company to keep a close vision on safety precautions. In Divgi industries, efforts or taken by the management for sector of chargemen and other leading hands putting efforts for safety. Various posters are pasted on the walls, shop floors and near the punch card clocks showing the importance of safety, employees engaged on shop floor are provided with safety goggles, hand gloves, etc. Company has got important of returns regarding observance of safety. As a company has sufficient land, care has been taken for more space in the workshop and ample apace is left around the machine for the workers to move freely. In addition to this, the shops are properly maintained with proper ventilation, lighting etc. in the department where thers is direct contact with the electricity proper has been taken.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

46

CASH MANAGEMENT IN WORKING CAPITAL

Thus the company has got better policy maintaining safety. This policy has been made not just for the sake of provison a Factory Act 1948, but to keep its work force away form any accidents or mishaps. If in case the accident occurs sufficient medical provisions are made. In this way, almost care is being taken by DIPL for the employees safety. WORKERS PARTICIPATION IN MANAGEMENT: There is no provision of workers participation in management in DIPL but the beneficial suggestions are always welcomed by management. If the suggestion are truly beneficial to the company then the same are awarded accordingly. Communication: This is very effective, tere is very less communication gap between management and the employees. Weekly meeting are conducted for senior management level, twice a month meetings are held for supervisors and for workers notices are put on the notice board in evrery dept. in case of any problems workers can directly communicate to top management or through supervisioors. Communication system is upword aswell as downword which reduces problems and increases productivity of the company.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

47

CASH MANAGEMENT IN WORKING CAPITAL

Welfare Facilities Provided by DIPL (As per the factory act 1948) Statutory welfare facilities. Non-statutory welfare facilities 1) Provisions Regarding health and Safety: ( Cleanliness section 11 ) The company is kept clean by daily sweeping and washing the floors. The company has 3 sweepers. The effective arrengments are made to dispose off the waste and efficient According to the settlement signed by the management and employees it is agreed that all workmen will keep their machines and work area absolutely clean and maintain orderliness in the area around working place.

This company provides all sort of safety equipment and all safe working condition as required by the factory Act 1948. Employees engaged in shop are provided with safety shares and hand gloves, safety goggles, ear muffs, safety belts etc. The company has also provided fire fighting equipments.

2) Ventilation and Temperature: ( Sec. 13 )

Suitable arrangement are made to ensure ventilation and working temperature with the help of sufficient number of

48

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

windows, exhaust and cross ventilation. The temperature is kept nearly constsnt with the effective measures at the working place. 3) Dust and Fumes: ( sec 14 ) This company is immune to the dust and as a results of adoption of modern technique to over come this factors. 4) Light : ( sec 17 ) Every part of the company is provided with sufficient and suitable lighting both natural and artificial. Glazed windows and sky light are used for lighting work rooms. Effective provisions are made to prevent glare and formation of shadows to such an extent so as to avoid strain. 5) Drinking water : ( sec 18 ) The company has provided a clean drinking water facility to all employees. The water tank is kept in clean and hygienic condition. There are big clay pots fitted with tops in every section of the company.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

49

CASH MANAGEMENT IN WORKING CAPITAL

6) Latrines and Urinals : ( sec 19 ) Sufficient latrines and urinals are provided which are

conveniently situated and accessible to workers at all the times .these are cleanly maintained and are in good conditions. 7) washing Facilities:- [ Sec 42] The company has provided adequate and suitable washing facilities as per the factories Act 1948. the number of taps and basions are sufficient other things like soap towels are provided . 8) First Aid application and dispenssry:The company has proided first aid boxes in every dept.and they are checked periodically by the authorised person .Being a light engineering company accidenta rate is very low. If an accident arise the injuried person is taken to Rotary Hospital Sirsi [ there is agreement between and the hospital ]. 9) Canteen : [ Sec 46 ] Free canteen facilites are proided for employees. The canteen proides the worker with break fast ,tea,and lunch. 10) Welare Officer :- [ Se 49] As vper the reqirements the company has appointed the HRD officer in 3 shifts. Each employee works for 8 hours a day. Sunday is a weekly holiday.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

50

CASH MANAGEMENT IN WORKING CAPITAL

A break of half an hour is givan in each shift. The office staff work in a general shift of 9am to 5pm. 1.General shift 2.First shift 3. Second shift 4. Third shift 9 am to 5 pm 7.30am to 4 pm 4 pm to 12.30 am 12.30 am to 7.30 am

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

51

CASH MANAGEMENT IN WORKING CAPITAL

12.

Leave / Paid holidays :

An employ in the company enjoys different types of leave which are as follows: a) Earned leave:- 15 days for first 240 days. b) Casual leave:- 7 days per year. c) Sick leave 10 days for those who are not covered by E.S.I.C and 4 days for those covered by E.S.I.C. Paid holidays: The company has sanctioned paid holidays through out the year which are as follows:1. Republic day 26th January

2. Karnataka Rajyotsava Ist November

3. independence day 15th August

4. Vijaya Dashami 5. Anant chturdasi 6. Diwali 13) Other statutory welfare benefits:-

The company provides all other statutory benefits like gratuity bonus as per rules laid down in their following acts. Gratuity: - It is paid as per the gratuity Act 1972 and it is also linked with the life insurance corporation of India.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

52

CASH MANAGEMENT IN WORKING CAPITAL

Bonus: - Bonus is paid according to the settlement. Usually 8.33% per annum is paid.

B. Non statutory facilities:1. Pay scales and Allowances:As per settlement signed between workers and management. 2. Financial assistance to perform last rites of Death: If an employee dies while in service his/her immediate family member is given Rs 4000/- as emergency assistance to the performance of last rites.

3. Transport The company has 3 cars, tempo and jeeps for its purpose which is managed by the transport department of the company. 4. Lons and Advances: Advances are given by the company to its employees but it depends upon the situation and the management decision. 5. Leave Travel allowances:

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

53

CASH MANAGEMENT IN WORKING CAPITAL

The company pays Rs 830.00 per annum as leave travel allowances to its employees who fulfill attendance i.e. not less then 240 days. 6. Uniform: The company issues two pairs of dress per person per year. The company also issues one pair of safety shoes.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

54

CASH MANAGEMENT IN WORKING CAPITAL

7. Training:

Training is given to the employees inside a well as outside the factory according to the training needs. I T I/ Diploma holders are given practical training after being recruited apart from that at intervals especially when new machines are installed. 8. Promotion: Every employees has an opportunity for promotion. Usually promotion are awarded to employees according to their respective work. Which is based on qualities. Certain facts are considered .. persons are liable for promotions. a) b) c) d) Responsibility Sincerity Quality of work Attendance However seniority as well merit is considered according to the performance. There is performance appraisal. PLANT LOCATION:

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

55

CASH MANAGEMENT IN WORKING CAPITAL

Ideal plan location is important a business activity. Plant location decision being strategic long term and non repetitive require detailed analysis of long term consequences.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

56

CASH MANAGEMENT IN WORKING CAPITAL

Factors governing plant location. Regional factors Community factors Site factors Regional factors:- Decide the overall area within the country , proximity to markets, proximity to source of raw materials, availability of utilities, transport facilities, climatic condition, industrial and taxation laws. Community factors:Community factors influences

selection of the plant location within the region such factors are; availability of labour, industrial and labour attitudes,social structure, service facilities etc. Site factors:- Site factors favour specific site within the community. Such factors are, availability and cost of the land, suitability of the land etc.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

57

CASH MANAGEMENT IN WORKING CAPITAL

INFRASTRUCTURE FACILITIES: Infrastructure facilities consider availability of utilities like power water, disposal of west etc. Power:- It is one of the useful need of the industry, which helps the organization to maintain his productivity Divgi industries Pvt Ltd sanctioned power of 750 KVA AR with an independent transformer. The unit also having a generator of 250 KVA to ensure continuity of production even at the if power failure. Water:- The requirement of waters is main for human consumption and to some extend for processing. The water requirement will be more than 1500 liters per day. The location has very good water facility. Fuel:- In Divgi industries Pvt Ltd they use the diesel in the generator. They have the generator of high capacity. That is 250 KVA for which the fuel is consumed more i.e 17 liters of diesel for one hour.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

58

CASH MANAGEMENT IN WORKING CAPITAL

LEGISLATION AND TAXATION: The policies of the state government and local bodies relating to issue of licenses, building codes, labour laws etc. are the factors in selecting rejecting a particular community site.

CLASSIFICATION OF EMPLOYEES : 1. 2. 3. 4. Permanemt Probationery Casual Apprentice Permanent employee : Permanent employee is one who has been emerged on a permanent basis and includes any person also has satisfactorily completes a probationary period of not less then three months in the same an onother accupation in the establishment including breaks due to sickness, accident, leave, lockout, strike,(not seeing an illegal strike) or involuntary closure of the establishment. Probationer : Is an employee who is provisionally engaged to fill a permanent cacancy in post and has not completed three months services there in. If a permanent employee is employed as a probationer in a new post , he may at any time during the

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

59

CASH MANAGEMENT IN WORKING CAPITAL

probationary period be reverted back to his old permanent post. Absence on side leave or due to accident or any other reason shall not be included in computing probationary period. Casual worker : Is a work man whose employment is of casual nature. Apprentice : Is a learner who is paid an allowance during the period of training.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

60

CASH MANAGEMENT IN WORKING CAPITAL

JOB DESCRIPTION Chief Executive Officer: 1) To Plan operation delegate duties appropriately to his subordinates, and coordinate their work on a day to day as well as long range basis to reach his units objectives. 2) To appreciate the changing conditions and trends affecting the work of his unit and the services it should render. 3) To select appropriate personnel for specific assignments. 4) To direct the work of his immediate subordinates which require the ability to understand thoroughly their work and guide them. 5) To stimulate, motivate and lead his subordinates with a view to secure their interested and willing participation towards achieving the common goals of the unit and the enterprise. 6) To supervise, follow up, and appraise the performance of his subordinates. 7) To interview subordinates, obtain information from them and get them to express their interests and attitudes. 8) To develop his subordinates to better efforts.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

61

CASH MANAGEMENT IN WORKING CAPITAL

9) Technical skills to accomplish the mechanic of the particular job. 10) Human skills to build team spirit as a leader,

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

62

CASH MANAGEMENT IN WORKING CAPITAL

Production In charge: 1) To initiate and set up procedures to ensure that quality of the production is maintained up to the standards. 2) To discuss and finalize with concerned personnel the fortnightly production plans. 3) To Ensure that the various section maintain their production and delivery schedules. 4) To Ensure that production requirements are met with on time. 5) To decide and give overtime working when production not met with customer requirement. 6) To sort out problems encountered during regular production and solve the same with advice and help of service depts., if necessary. 7) To attend the Technical committee meeting and report the technical problems incurred during routine production. 8) To ensure production related machines & other equipments are in always good condition.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

63

CASH MANAGEMENT IN WORKING CAPITAL

9) To ensure that there is a general cleanliness and orderliness throughout the manufacturing as well as storage and other facility areas. 10) staff To ensure that there is a general discipline and as far

as possible a feeling of well-being among the production

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

64

CASH MANAGEMENT IN WORKING CAPITAL

Quality Assurance Officer: 1) To prepare the Quality Plan for the finished products. 2) To ensure that all incoming materials, in process, & finished products for production are inspected and rested in accordance with the established procedures. 3) To approve and release the finished product for dispatch to the customer. 4) To ensure that the relevant inspection records are maintained at appropriate stages of inspection. 5) To ensure calibration of monitoring and measuring devices at defined frequency. 6) To implement the Measurement System Analysis & Statistical process control techniques appropriately. 7) To hold production, in the event major deviation pertaining to quality systems is observed on the production line.

Stores Officer: 1) To ensure proper storage of inventories in the Stores. 1) To ensure that proper inventory levels are maintained. 2) To issuing the materials for production on FIFO system. 3) To maintaining & updating the stock registers. 4) To prepare DCs of finished goods, & ensure that the finished goods are delivered to the customer with proper dispatch documents.

65

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

Purchase officer: 1) To evaluate the Sub contractors for out sourced components only 2) To prepare & maintain approved suppliers list, & ensure the purchases are made from the approved suppliers. 3) To ensure that the purchased materials are in accordance with the POs. 4) To interact with, stores, production, & maintenance departments before finalizing the POs, and prepare the POs. 5) To periodically monitor the supplier through supplier rating.

Officer maintenance

1) To

planned

maintenance,

breakdown

maintenance,

predictive & preventive maintenance of machines. 1) To maintain the relevant maintenance records. 2) To ensure the proper inventory of critical spare parts are maintained. 3) To ensure that while ordering spare/parts proper specifications, are clearly specified in the POs And further confirm the incoming materials ordered by his department

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

66

CASH MANAGEMENT IN WORKING CAPITAL

are in accordance with their specifications, and authorized to clear the GRRs for such materials.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

67

CASH MANAGEMENT IN WORKING CAPITAL

Officer Personnel:

1) Maintaining contacts with the Factory Inspectors, Labour

Inspectors and Act, and other govt. authorities. Representing the Company before the Conciliation Authorities 2) Counseling and assisting employees in regard to personal difficulties and problems affecting ability and contentment in work. 3) To collect the training needs from the respective departments of the company 4) To prepare annul training plan. 5) To arrange the faculties for training to meet the training to meet the training topic needs. 6) To keep training records. 7) To evaluating the training, trained employees in consultation with faculty and concerned Dept. head. 8) Ta maintain the records of each employee. 9) To recruitment of the new employee in consultation with the department heads & C.E.O./Manager. Management Representative:

1) To

ensure the management policies & control are

understood,

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

68

CASH MANAGEMENT IN WORKING CAPITAL

implemented and maintained in accordance with Quality std, requirements. 2) To issue & withdrawal of quality system documents. 3) To conduct internal quality audits & liasoning audits. 4) To conduct Management reviews. 5) To monitoring appropriate action for system nonconformities. 6) To maintain the department records. external

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

69

CASH MANAGEMENT IN WORKING CAPITAL

Customer Representative:

1) To interacting with customer on special characteristics &

communication the details of interaction in the concerned personnel of his company and collecting the customer information 2) To take concession on specification/manufacturing processes. 3) To interacting with customer for delivery schedules & on time delivery of products to the customer. 4) To take the resolving customer complaints. Operators: 1) To take instruction from Supervisors/in charge about the machine to be operated, & job to be machined. 2) To follow the work instructions & process flow diagram. 3) Monitor the process by given instruments & documents. 4) Keep separately rework/rejected jobs with proper identification. 5) End of the shift fill the production detail in necessary documents. 6) Inform Production in charge in case of machine break down. 7) Stop production in consultation with Prod. In charge / Quality inspector, if improper deviation observed in the job.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

70

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

71

CASH MANAGEMENT IN WORKING CAPITAL

JOB WORK In this system, goods are produced according to the customers orders. Continuous orders will be there from the customer and when ever orders are received, the job will be taken up for the production. This is also known as Market Order Business. As the need of each customer varies the materials and machinery will also be differ. Each job is different, distinct and support class by itself. The cost of the items produced by this method will therefore be higher than the cost of the similar items produced in mass production bases.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

72

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

73

CASH MANAGEMENT IN WORKING CAPITAL

Brief view of departments Production DIPL produces different types of components which are used in gearbox of the automobiles. like, sun gear, companion flange, yoke, shaft For different products there are many in chargers ,who carried out production through workers. When job work comes, production in chargers , operators, supervisors together make the schedule for the work. The raw materials are in the forging form. After they have to under go mainly 4 process. 1 Rough turn 2 Finish turn 3 Broaching 4 Drill tap These process are carried out separately for both the sides. Water soluble, oils are used as a coolant which increases the life of the machines. Quality assurance The quality assurance department is specially meant for final approval. It is responsible for verification of products. After the approval from this department , only the final products are supplied to customer. The company is certified with ISO/TS16949 quality system guidelines and improves its effectiveness.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

74

CASH MANAGEMENT IN WORKING CAPITAL

Functions: Monitoring the process continuously to ensure that suitable product parameters are in compliance with the established requirement.

Approving process, equipment, personnel for maintaining records of qualified and special process.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

75

CASH MANAGEMENT IN WORKING CAPITAL

Maintenance This department is essential in all production organizations which is mainly concerned with the machine work. The machinery maintenance is one of the part of day to day work. Function Look after the day to day maintenance of the machinery To purchase the parts that may require for the maintenance To keep the machineries in good condition every day To make the repairs of the machineries Stores It is responsible to ensure proper storage of inventories in the store It is responsible to ensure that proper inventory levels are maintained It is responsible and authorized for issuing the materials for production on FIFO method It is responsible for maintaining and updating the store register It is responsible to prepare DCs of finished goods and ensure that the finished goods are delivered to the customer with proper dispatch documents. Personal department

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

76

CASH MANAGEMENT IN WORKING CAPITAL

Human

resource is

our valuable

asset.

So

proper

management of this asset is very important. This department involves 2 types of functions Regulatory functions: Maintain attendance register and wages register in form no 22 Maintain adult register in form no 11 Maintain leave book of employees Collect provided fund amount i.e.12%

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

77

CASH MANAGEMENT IN WORKING CAPITAL

Administrative functions: Safety and cleaning of premises Recruitment Training and development programs for all the departments Prepare annual training report, performance appraisal Management representative It is responsible for the total quality programs and shall have authority and freedom for ensuring. The management policies and control are understood implemented and maintained in accordance with ISO/TS16949 Customer representative This department is responsible to ensure customer

representative are communicated to appropriate departments and fulfill the special characteristics, setting quality objective, conduct related training programs. Also responsible to take corrective and preventive actions, product design & development. Most important function is handling the customer related issue. Finance Finance is essential component of the business. To maintain this

78

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

effectively a specialized department is there i.e. FINANCE DEPARTMENT. This department is concerned with the day to day financial activities like purchase, sale, payments, receipts etc. It properly manages the accounts of concerned year.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

79

CASH MANAGEMENT IN WORKING CAPITAL

Functions Day to day cash /bank transactions Recovering Bills passing and payments Recording of all the transactions in books of A/Cs Preparation of cash flow statement budget Providing various types of management information reports required by the management from time to time Carry out auditing Main sources of income

Labour charges from DWPL From the sale of scrape which is available during the time of production From dividend of share Current customer for scrape

Southern Ferro India Pvt. Ltd. M.S.P.Division 173 Belur Industrial estate Dharwad First steel Traders Hubli

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

80

CASH MANAGEMENT IN WORKING CAPITAL

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

81

CASH MANAGEMENT IN WORKING CAPITAL

CASH MANAGEMENT INTRODUCTION Cash is the important current asset operations of the business. Cash is basic input needed to keep the business running on a continuous basis; it is also the ultimate output expected to be realized by selling the service or product manufactured by the firm. The firm should keeps sufficient cash, neither more nor less. Cash shortage will disrupt the firms manufacturing operation while excessive cash will simply remain idle, without contributing anything toward the firms profitability. Thus, a major function of the financial manager is to maintain a sound cash position. Cash is the money which a firm can disburse immediately without any restriction. The term cash includes coins, currency and cheques held by the firm, and balances in its bank accounts. Some times near-cash items, such as marketable securities or bank times deposits, are also included in cash. The basic characteristic of nearcash assets is that they can readily be converted in to cash. Generally, when a firm has excess cash, it in marketable securities. This kind of investment contributes some profit to the firm.

Cash flow isn't the same as profit and loss. Believe it or not, a company can be profitable while experiencing cash flow problems that drive it to bankruptcy.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

82

CASH MANAGEMENT IN WORKING CAPITAL

Profit is an accounting term, which includes non-cash items and estimates. Cash flow is a less forgiving number with a harder edge that factors in payments and expenditures. If your sales are profitable, but you need to need to invest millions in new plant and equipment to make the products you sell, cash flow may not be a pretty sight.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

83

CASH MANAGEMENT IN WORKING CAPITAL

Another fallacy: Cash is not the balance in your business bank account. Your cash balance in your accounting books needs to cover checks you have issued which have not yet been paid by your bank. You may have customer payments in hand, checks and bank drafts, which have not yet been deposited in your bank. That's cash, too, even though you can't bank on it. Where does cash come from, asked the little boy? For most businesses, a major source of cash comes from sales to customers. It's not necessarily a direct path, though. Many businesses extend credit to customers, so the sale hangs around as an account receivable, preferably for as short a time as possible, before the customer sends payment for the purchase and the receivable converts to good old cash. Cash can also come from financing activities, such as a bank loan or an investment by the business owners. Where does cash go? Just about where you would expect: to pay suppliers and employees and investments in plant and equipment. It may also be used to repay debt or provide an investment return to owners. Cash flow can be more difficult to predict than profit and loss, particularly for smaller businesses that are dependant on a few large customers. You may be able to estimate when you will close a sale and earn the profit. But you may have little control over when your customers pay you and the cash comes in.

84

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

Typically, a business has more control over its cash payments than its cash receipts. Granted, your employees expect to receive their pay on payday. However, you may be able to stretch the time you take to pay your trade suppliers within reason, of course.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

85

CASH MANAGEMENT IN WORKING CAPITAL

"Annual income twenty pounds, annual expenditure nineteen six, result happiness. Annual income twenty pounds, annual expenditure twenty pound ought and six, result misery." - Charles Dickens (David Copperfield) Victorian author Charles Dickens deftly summarized the importance of positive cash flow 150 years ago. Today, cash flow is still the lifeblood of any business. Like it or not, cash is how business keeps score. If you don't have enough cash on hand, you can't pay your suppliers, your employees, or your financers. Without sufficient cash, you'll go out of business soon enough. Cash flow is the flow of spendable money into your business and back out again. You may have sold tons of goods and have a fistful of invoices to show for it. But you can't spend those invoices directly you can't pay your employees with them come payday, nor your suppliers when you're ready to make a new batch of widgets. It's when you are on a deadline to pay cash out, but your cash in hasn't showed up yet, that you are in cash-flow-crunch hell. Yet managing your cash flow can be a tricky business, and your business policies regarding, for example, how you extend credit to your customers, how many customers you have, and how quickly they pay, all can combine to make it too complex to track in your head. When it gets this complicated, smart business

86

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

managers turn to computerized tools to help them get a handle on the process, the risks, and the opportunities. In this All Business.com Buyer's Guide, we provide a backgrounder on cash-flow concepts, an overview of software tools for managing cash flow, and some tips about which policies you've got to keep an eye on if you expect to stay out of unanticipated trouble.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

87

CASH MANAGEMENT IN WORKING CAPITAL

FACETS OF CASH MANAGEMENT Cash management is concerned with the managing of: (i) cash flows into and out of the firm, (//) cash flows within the firm, and (Hi) cash balances held by the firm at a point of time by financing deficit or investing surplus cash. It can be represented by a cash management cycle as shown in the bellow figure. Sales generate cash which has to be disbursed out. The surplus cash has to be invested while deficit has to be borrowed. Cash management seeks to accomplish this cycle at a minimum cost. At the same time, it also seeks to achieve liquidity and control. Cash management assumes more importance than other current assets because cash is the most significant and the least productive asset that a firm holds. It is significant because it is used to pay the firm's obligations. However, cash is unproductive. Unlike fixed assets or inventories, it does not produce goods for sale. There-fore, the aim of cash management is to maintain adequate control over cash position to keep the firm sufficiently liquid and to use excess cash in some profitable way. Cash management cycle

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

88

CASH MANAGEMENT IN WORKING CAPITAL

The management of cash is also important because it is difficult to predict cash flows accurately, particularly the inflows, and there is no perfect coincidence between the inflows and outflows of cash. During some periods, cash outflows will exceed cash inflows, because payments for taxes, dividends, or seasonal inventory build up. At other times, cash inflow will be more than cash payments because there may be large cash sales and debtors may be realised in large sums promptly. Cash management is also important because cash constitutes the smallest portion of the total current assets, yet management's considerable time is devoted in managing it. In recent past, a number of innovations have been done in cash management techniques. An obvious aim of the firm now-a-days is to manage its cash affairs in such a way as to keep cash balance at a minimum level and to invest the surplus cash in profitable investment opportunities.

In order to resolve the uncertainty about cash flow prediction and lack of synchronisation between cash receipts and payments, the firm should develop appropriate strategies for cash management. The firm should evolve strategies regarding the following four facets of cash management:

Cash planning - Cash inflows and outflows should be planned

to project cash surplus or deficitfor each period of the planning period. Cash budget should be prepared for this purpose.

Managing the cash flows - The flow of cash should be

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

89

CASH MANAGEMENT IN WORKING CAPITAL

properly managed. The cash inflows should be accelerated while, as far as possible, the cash outflows should be decelerated.

Optimum cash level - The firm should decide about the

appropriate level of cash balances. The cost of excess cash and danger of cash deficiency should be matched to determine the optimum level of cash balances.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

90

CASH MANAGEMENT IN WORKING CAPITAL

Investing surplus cash - The surplus cash balances should be

properly invested to eam profits. The firm should decide about the division of such cash balance between alternative short-term investment opportunities such as bank deposits, marketable securities, lending. The ideal cash management system will depend on the firm's products, organisation structure, competition, culture and options available. The task is complex, and decisions taken can affect important areas of the firm. For example, to improve collections if the credit period is reduced, it may affect sales. However, in certain cases, even without fundamental changes, it is possible right bank and controlling the collections properly. M O T IV E S F O R H O L D IN G C A S H The firm's need to hold cash may be attributed to the following three motives, to significantly reduce cost of cash management system by choosing a or intercorporate

The transactions motive The precautionary motive The speculative motive. Transaction Motive

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

91

CASH MANAGEMENT IN WORKING CAPITAL

The transactions motive requires a firm to hold cash to conduct its business in the ordinary course. The firm needs cash primarily to, make payments for purchases, wages and salaries, other operating expenses, taxes, dividends etc. The need to hold cash would not arise if there were perfect synchronisation between cash receipts and cash payments, i.e., enough cash is received when the payment has to be made. But cash receipts and payments are not perfectly synchronised.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

92

CASH MANAGEMENT IN WORKING CAPITAL

For those periods, when cash payments exceed cash receipts, the firm should maintain some cash balance to be able tomake required payments. For transactions purpose, a firm may invest its cash in marketable securities. Usually, the firm will purchase securities whose maturity corresponds with some anticipated payments, such as dividends, or taxes in the future. Notice that the transactions motive mainly refers to holding cash to meet anticipated payments whose timing is not perfectly matched with cash receipts. Precautionary Motive The precautionary motive is the need to hold cash to meet contingencies in the future. It provides a cushion or buffer to withstand some unexpected emergency. The precautionary amount of cash depends upon the predictability of cash flows. If cash flows can be predicted with accuracy, less cash will be maintained for an emergency. The amount of precautionary cash is also influenced by the firm's ability to borrow at short notice when the need arises. Stronger the ability of the firm to borrow at short notice less the need for precautionary balance. The precautionary balance may be kept in cash and marketable securities. Marketable securities play an important role here. The amount of cash set aside for precautionary reasons is not expected to earn anything; therefore, the firm should attempt to earn some profit on it. Such funds should be

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

93

CASH MANAGEMENT IN WORKING CAPITAL

invested in high-liquid and low-risk securities and relatively less in cash. Speculative Motive

marketable securities.

Precautionary balance should, thus, be held more in marketable

The speculative motive relates to the holding of cash for investing in profit-making opportunities as and when they arise. The opportunity to make profit may arise when the security prices change.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

94

CASH MANAGEMENT IN WORKING CAPITAL

The firm will hold cash, when it is expected that interest rates will rise and security prices will fall. Securities can be purchased when the interest rate is expected to fall; the firm will benefit by the subsequent fall in interest rates and increase in security prices. The firm may also speculate on materials' prices. If it is expected that materials' prices will fall, the firm can postpone materials' purchasing and make purchases in future when price actually falls. Some firms may hold cash for speculative purposes. By and large, business firms do not engage in speculations. Thus, the primary motives to hold cash and marketable securities are: the transactions and the precautionary motives. CASH PLANNING Cash flows are inseparable parts of the business operations of firms. A firm needs cash to invest in inventory, receivable and fixed assets and to make payment for operating expenses in order to maintain growth in sales and earnings. It is possible that firm may be making adequate profits, but may suffer from the shortage of cash as its growing needs may be consuming cash very fast. The cash poor' position of the firm can be corrected if its cash needs are planned in advance. At times, a firm can have excess cash with it if its cash inflows exceed cash outflows. Such excess cash may remain idle. Again, such excess cash flows can be anticipated and properly invested if cash planning is resorted to. Thus, cash planning can help to anticipate the future cash flows and needs of

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

95

CASH MANAGEMENT IN WORKING CAPITAL

the firm and reduces the possibility of idle cash balances (which lowers firm's profitability) and cash deficits (which can cause the firm's failure).

Cash planning is a technique to plan and control the use of cash. It protects the financial condition of the firm by developing a projected cash statement from a forecast of expected cash inflows and outflows for a given period.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

96

CASH MANAGEMENT IN WORKING CAPITAL

The forecasts may be based on the present operations or the anticipated future operations. Cash plans are very crucial in developing the overall operating plans of the firm. Cash planning may be done on daily, weekly or monthly basis. The period and frequency of cash planning generally depends upon the size of the firm and philosophy of management. Large firms prepare daily and weekly forecasts. Medium-size firms usually prepare weekly and monthly forecasts. Small firms may not prepare formal cash forecasts because of the non-availability of information and small scale operations. But, if the small firms prepaid cash projections, it is done on monthly basis. As a firm grows and business operations become complex, cash planning becomes inevitable for its continuing success. Cash Forecasting and Budgeting

Cash budget is the most significant device to plan for and control cash receipts and payments. A cash budget is a summary statement of the firm's expected cash inflows and outflows over a projected time period. It gives information on the timing and magnitude of expected cash flows and cash balances over the projected period. This information helps the financial manager to determine the future cash needs of the firm,

97

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

plan for the financing of these needs and exercise control over the cash and liquidity of the firm.' The time horizon of a cash budget may differ from firm to firm. Monthly cash budgets may be prepared by a firm whose business is affected by seasonal variations. Daily or weekly cash budgets should be prepared for determining cash requirements if cash flows show extreme fluctuations. Cash budgets for a longer intervals may be prepared if cash flows are relatively stable.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

98

CASH MANAGEMENT IN WORKING CAPITAL

Cash forecasts are needed to prepare cash budgets. Cash forecasting may be done on short or long-term basis. Generally, forecasts covering periods of one year or less are considered short-term; those extending beyond one year are considered long-term. Short term forecasts It is comparatively easy to make short-term forecasts. The important functions of carefully developed short-term cash forecasts are: To determine operating cash requirements To anticipate short-term financing To manage investment of surplus cash. The short-term forecast helps in determining the cash requirements for a predetermined period to run a business. If the cash requirements are not determined, it would not be possible for the management to know how much cash balance is to be kept in hand, to what extent bank financing be depended upon and whether surplus funds would be available to invest in marketable securities. To know the operating cash requirements, cash flow projections have to be made by a firm. As stated earlier, there is hardly a perfect matching between cash inflows and outflows. With the short-term cash forecasts, however, the financial manager is

99

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

CASH MANAGEMENT IN WORKING CAPITAL

enabled of the firm.

to

adjust

these

differences

in

favour

It is well known that, for their temporary financing needs, most companies depend upon banks.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

100

CASH MANAGEMENT IN WORKING CAPITAL

One of the significant roles of the short-term forecasts is to pinpoint when the money will be needed and when it can be repaid. With such forecasts in hand, it will not be difficult for the financial manager to negotiate short-term financing arrangements with banks. This in fact convinces bankers about the ability of the management to run its business. The third function of the short-term cash forecasts is to help in managing the investment of surplus cash in marketable securities. A carefully and skillfully designed cash forecast helps a firm to: (0 select securities with appropriate maturities and reasonable risk, (//) avoid over and underinvesting and (Hi) maximise profits by investing idle money. Short-run cash forecasts serve many other purposes. For example, multi-divisional firms use them as a tool to coordinate the flow of funds between their various divisions as well as to make financing arrangements for these operations: These forecasts may also be useful in determining the margins or minimum balances to be maintained with banks. Still other uses of these forecasts are, Planning reductions of short and long-term debt Scheduling payments in connection with capital expenditures programmes Planning forward purchases of inventories Checking accuracy of long-range cash forecasts

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

101

CASH MANAGEMENT IN WORKING CAPITAL

Taking advantage of cash discounts offered by suppliers Guiding credit policies.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

102

CASH MANAGEMENT IN WORKING CAPITAL

Short-term Forecasting Methods Two most commonly used methods of short-term cash forecasting are: The receipt and disbursements method The adjusted net income method. The receipts and disbursements method is generally employed to forecast for limited periods, such as a week or a month. The adjusted net income method, on the other hand, is preferred for longer durations ranging between a few months to a year. Both methods have their pros and cons. The cash flows can be compared with budgeted income and expense items if the receipts and disbursements approach is followed. On the other hand, the adjusted income approach is appropriate in showing a company's working capital and future financing needs.

Receipts and disbursements method - Cash flows in and out in most companies on a continuous basis. The prime aim of receipts and disbursements forecasts is to summarise these flows during a predetermined period. In case of those companies where each item of income and expense involves flow of cash, this method is favoured to keep a close control over cash.

INSTITUTE OF BUSINESS MANAGEMENT & RESEARCH - HUBLI

103

CASH MANAGEMENT IN WORKING CAPITAL

Three broad sources of cash inflows can be identified: (i) operating, (//) non-operating, and (Hi) financial. Cash sales and collections from customers form the most important part of the operating cash inflows. Developing a sales forecast is the first step in preparing a cash forecast. All precautions should be taken to forecast sales as accurately as possible. In case of cash sales, cash is received at the time of sale. On the other hand, cash is realised after sometime if sale is on credit. The time in realising cash on credit sales depends upon the firm's credit policy reflected in the average collection period.