You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (399)

- The UN Dispute Settlement Mechanism Reinforce The Rule of LawDocument5 pagesThe UN Dispute Settlement Mechanism Reinforce The Rule of LawQisthiDaisyNo ratings yet

- Comparative Studies Civil ProDocument8 pagesComparative Studies Civil ProQisthiDaisyNo ratings yet

- Comparative Studies Civil ProDocument8 pagesComparative Studies Civil ProQisthiDaisyNo ratings yet

- Juridical Evaluation On Aceh - FULL PAPERDocument9 pagesJuridical Evaluation On Aceh - FULL PAPERQisthiDaisyNo ratings yet

- Course Book Intl Envo LawDocument6 pagesCourse Book Intl Envo LawQisthiDaisyNo ratings yet

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (838)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (119)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (821)

- Rsbsa-8 7 2015 PDFDocument4 pagesRsbsa-8 7 2015 PDFRonalene Garbin100% (1)

- A More Expensive Cuppa: Nestle (Malaysia)Document8 pagesA More Expensive Cuppa: Nestle (Malaysia)bijueNo ratings yet

- Personal ID: MD-2071, CHISINAU STR. ALBA-IULIA 75/22b, Ap. 22Document1 pagePersonal ID: MD-2071, CHISINAU STR. ALBA-IULIA 75/22b, Ap. 22Bargan DoinițaNo ratings yet

- PDFDocument7 pagesPDFClaytonNo ratings yet

- HDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Document1 pageHDFC Bank Credit Cards GSTIN: 33AAACH2702H2Z6 HSN Code - 9971Hardik RavalNo ratings yet

- Shippers Letter of InstructionDocument2 pagesShippers Letter of InstructionWilliam LooNo ratings yet

- Standar Pemasangan Sticker Mesin ATM BCA 2021Document20 pagesStandar Pemasangan Sticker Mesin ATM BCA 2021MA FayyadhNo ratings yet

- Star Two vs. Paper CityDocument2 pagesStar Two vs. Paper CityJewel Ivy Balabag DumapiasNo ratings yet

- Abenson Summer Exclusives - Promo Mechanics PDFDocument2 pagesAbenson Summer Exclusives - Promo Mechanics PDFBon Alexis GuatatoNo ratings yet

- Bank of Namibia Act 15 of 1997Document22 pagesBank of Namibia Act 15 of 1997André Le RouxNo ratings yet

- From Import Import From Import From Import Try From Import Except PassDocument2 pagesFrom Import Import From Import From Import Try From Import Except PassriteshNo ratings yet

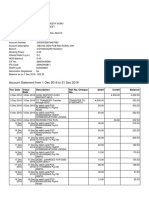

- Account Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Dec 2016 To 31 Dec 2016: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceENDLURI DEEPAK KUMARNo ratings yet

- Fms Project-Microfinance in IndiaDocument25 pagesFms Project-Microfinance in Indiaashu181186No ratings yet

- Nov Paper11 2010Document20 pagesNov Paper11 2010Aung Zaw HtweNo ratings yet

- T24 Islamic Banking User Guide: Wakala MusawamaDocument30 pagesT24 Islamic Banking User Guide: Wakala MusawamaSathya KumarNo ratings yet

- Liability Insurance.Document62 pagesLiability Insurance.pankajgupta80% (5)

- PradipchowdhuryDocument2 pagesPradipchowdhurybiswa chakrabortyNo ratings yet

- NAFSCOB-Branch OperationsDocument379 pagesNAFSCOB-Branch OperationsAshoak VarmaNo ratings yet

- Bills of ExchangeDocument16 pagesBills of ExchangeswayamNo ratings yet

- Tendering ProcessDocument36 pagesTendering ProcessChris Opuba100% (1)

- IRDA Syllabus for Insurance Broker ExamDocument8 pagesIRDA Syllabus for Insurance Broker Examreena mathurNo ratings yet

- New Microsoft PowerPoint PresentationDocument48 pagesNew Microsoft PowerPoint PresentationIryne Kim PalatanNo ratings yet

- Intermediate Accounting 3 PDFDocument86 pagesIntermediate Accounting 3 PDFChelsy SantosNo ratings yet

- Who is Sta. Lucia Land and their Sotogrande Condotel projectDocument44 pagesWho is Sta. Lucia Land and their Sotogrande Condotel projectRustle JimmiesNo ratings yet

- Case 4 - Wellfleet Bank (Patacsil)Document6 pagesCase 4 - Wellfleet Bank (Patacsil)Davy PatsNo ratings yet

- Certificate PDFDocument28 pagesCertificate PDFRecordTrac - City of OaklandNo ratings yet

- CPA Board Examinations QuestionsDocument14 pagesCPA Board Examinations QuestionsJeane BongalanNo ratings yet

- Fundamental of Banking MarathiDocument256 pagesFundamental of Banking MarathisunilNo ratings yet

- Pershing Sqaure CP ActivismDocument31 pagesPershing Sqaure CP ActivismMichael BenzingerNo ratings yet

- Investor investment patternsDocument4 pagesInvestor investment patternsSaiKumarSeelamNo ratings yet